The Stock Market Is Starting To Exhibit Some Healthier Signs Of Broadening Out

For weekend reading, Bryan Perry, Senior Director with Navellier Private Client Group, offers the following commentary:

Having been led by the “Magnificent Seven” mega-cap tech stocks, the stock market is starting to exhibit some healthier signs of broadening out. The S 500 posted a 6.5% gain for June, boosted by a number of bullish economic reports. The third revision of first-quarter GDP came in at +2.0% versus a previous 1.3%, while consumer confidence for June registered 109.7 versus an upwardly revised 102.5 for May, and we also saw the lowest weekly jobless claims in a month – all positive news for the economy.

So much for the Fed’s wish for widespread layoffs. Working Americans are spending with confidence once again. The S is now ahead by nearly 16% at the midpoint of 2023. Wall Street’s most vocal bears – like Mike Wilson of Morgan Stanley and Michael Hartnett of Bank of America – are still calling for a big sell -sometime over the next few months, but their thesis of a major collapse in S earnings just doesn’t seem to be materializing, as many of key or lagging sectors are getting their footing back.

In yet another catalyst for the bulls, the Federal Reserve reported that 23 of the country’s largest banks passed their annual stress test of lender strength in the face of a hypothetical economic recession.

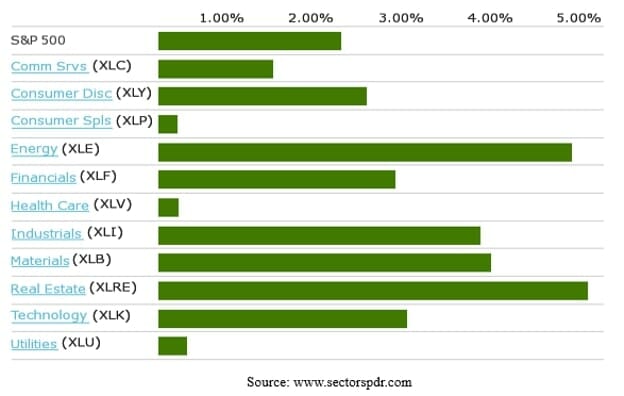

For the first time that I can remember in this calendar year, all the S 500’s sectors rose last week. Even the real estate and utility sectors gained in the face of Powell (and the bond market) seeming to be pretty convinced that another quarter point rate hike at the July 26 FOMC meeting is in the offing.

Real Estate and energy stocks actually led all 11 market S sectors last week, up 5% each.

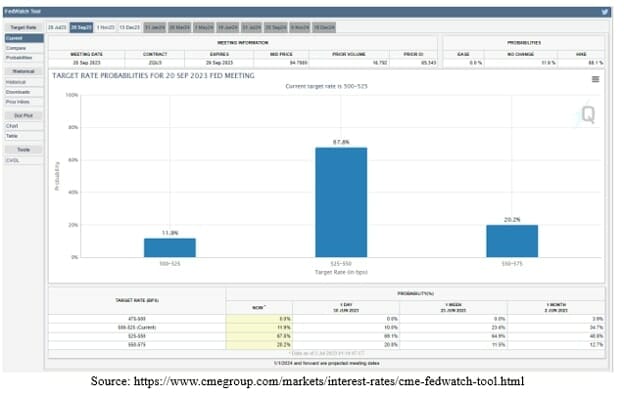

This week, investors received some key economic data points, including June manufacturing, June ADP private-sector employment, weekly jobless claims and the June employment report. Given the robust data of late, the bond futures market is pricing in a quarter point rate hike in Fed Funds to 5.25%-5.50%.

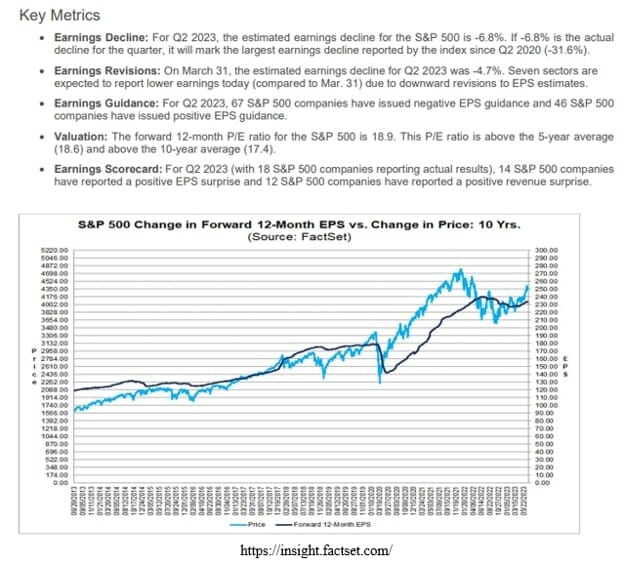

Come next week, second-quarter earnings season gets into full swing, with estimates wide-ranging. Below is the June 30 table of key metrics from FactSet Earnings Insight that show the current consensus estimate of 2023 S 500 earnings to be around $221, a far cry from the $185 level that the bearish Mike Wilson is predicting. It would take an earnings apocalypse in the second and third quarters to see this big a miss.

To put it simply, for the bears to prove their case, there is a lot riding on this earnings season.

Where the bears can run into trouble is if the FOMO (Fear of Missing Out) psychology starts to take hold on the notion – fear that a once certain recession is not in the cards. There is a mountain of cash in money markets and short-term Treasuries that could start to find its way into equities if 5% yields don’t satisfy.

As of last week, the Investment Company Institute reported that total money market fund assets decreased by $2.89 billion to $5.43 trillion for the week ending Wednesday, June 28. Among taxable money market funds, government funds decreased by $2.77 billion and prime funds decreased by $1.16 billion. Tax-exempt money market funds increased by $1.04 billion. ( Source: ici.org/research/stats/mmf)

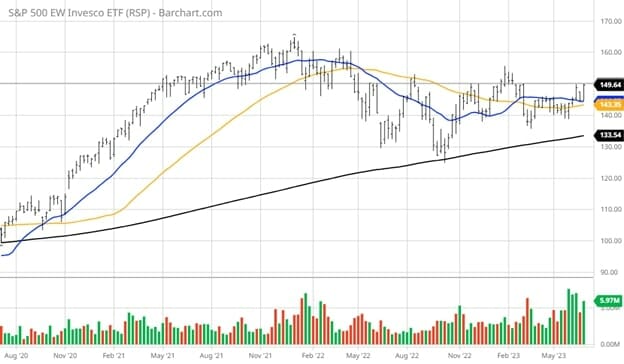

The Invesco S 500 Equal Weight ETF (RSP) outperformed the SPDR S 500 ETF (SPY) last week as the advance/decline line improved with more sectors getting a bullish lift. A break above $150 might well usher in a dash from cash into stocks. Hard to say for sure, but this rally has caught millions of nervous investors flat-footed, thanks to the most telegraphed recession that has not yet materialized.

Sure, there are big pockets of weakness – like corporate office properties – but heading into earnings season, there just hasn’t been some huge swath of companies issuing dramatically lower guidance that would materially alter the $221 estimate being put out by FactSet.

For one of the most hated rallies of the past several years, the pressure to get into stocks can sometimes exceed the pressure to stay out. I would think that the phones at bearish equity desks at firms like Morgan Stanley and Bank of America were burning up last week, especially on Friday, as the quarter ended on a powerfully bullish note. The thing about bearish predictions is that they always come true, at some point, but the timing of forecasting a meltdown can be many weeks, months or even years down the road.

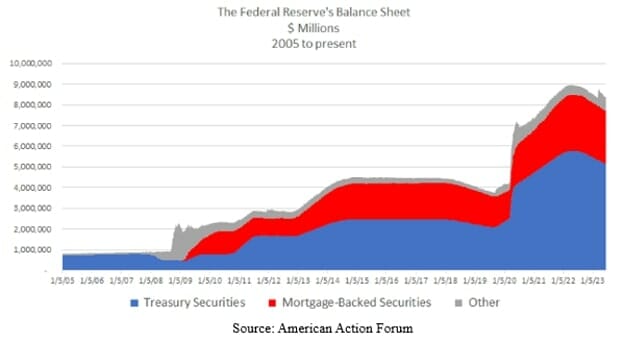

There is still a great deal of cash sloshing around the globe. As of June 14, the Fed’s assets stand at $8.4 trillion. And then there is the rest of the G-8 central banks and their bloated balance sheets. Money goes where it is best served, and with so little action in the IPO space to soak up excess liquidity, there looks to be room for the market to continue its advance and lift most boats, especially well-managed companies.

Source valuewalk

Invesco Ltd. Stock

Currently there is a rather positive sentiment for Invesco Ltd. with 5 Buy predictions and 1 Sell predictions.

As a result the target price of 18 € shows a positive potential of 33.63% compared to the current price of 13.47 € for Invesco Ltd..

{kind=link}

{kind=link}

{kind=link}