Growth Funds Dominate First Half Performance But Lead In Outflows

Lipper assigns funds both capitalization and size based on our quantitative Holdings-Based Classification (HBC) model. We’ve written about this in the past. The results of this model help build peer groups based on specific metrics of the underlying holdings, thus creating our 12 domestic HBC classifications. These 12 classifications are the combinations of four size buckets (large, multi, mid, and small) paired with three style assignments (growth, core, and value).

2022 was a tough year for the majority of asset classes, but growth stocks suffered greatly. Lipper’s Large-Cap Growth Funds (-31.51%), Multi-Cap Growth Funds (-32.92%), Mid-Cap Growth Funds (-29.47%), and Small-Cap Growth Funds (-26.66%) were among some of the lowest-performing equity classifications.

The Q4 2022 rally was not strong enough to stop the massive outflows from these domestic HBC funds, only Multi-Cap Core Funds (+$7.3 billion), Small-Cap Core Funds (+$2.9 billion), and Small-Cap Value Funds (+$1.5 billion) registered inflows during the last three months of the year. In total, the net outflows from the 12 domestic HBC classifications were $71.2 billion.

Growth Funds Recoup Their Losses

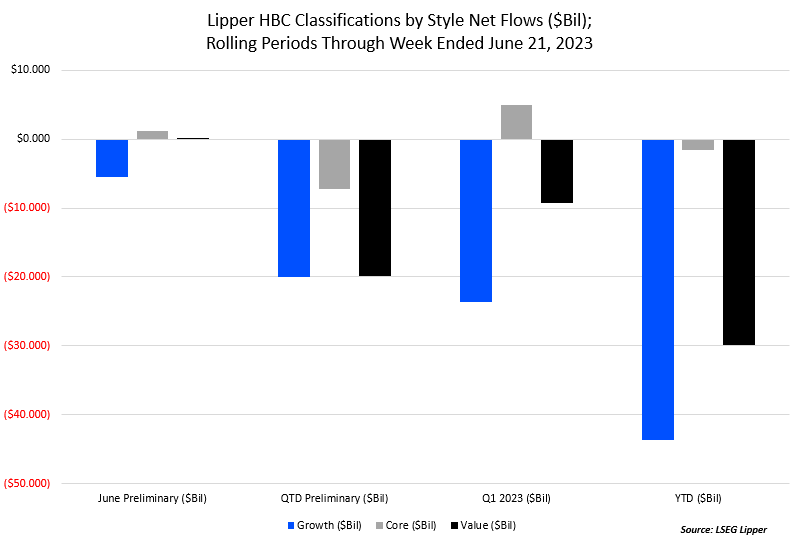

Now fast forward six months, growth funds have begun to recoup some of their 2022 losses. Year to date through June 22, 2023, Large-Cap Growth (+25.99%), Multi-Cap Growth (+$20.76), Mid-Cap Growth (+11.33%), and Small-Cap Growth (+8.99%) have realized strong gains. These growth classifications have all outperformed their Core and Value counterparts.

Despite the strong performance since the start of the year, these growth classifications have roughly $43.7 billion in outflows, with a preliminary net outflow of $20.0 billion coming over Q2 2023. Preliminary numbers for June have inflows for both core ($1.2 billion) and value (+$100 million), but heavy outflows for growth (-$5.5 billion).

The skew with performance is very top-heavy, with large gains coming from the now-called “Magnificent Seven” – NVIDIA (NASDAQ:NVDA), Tesla (NASDAQ:TSLA), Meta (NASDAQ:META), Apple (NASDAQ:AAPL), Amazon (NASDAQ:AMZN), Microsoft (NASDAQ:MSFT), and Alphabet (NASDAQ:GOOGL). Does this mean the flows are skewing towards large caps as well?

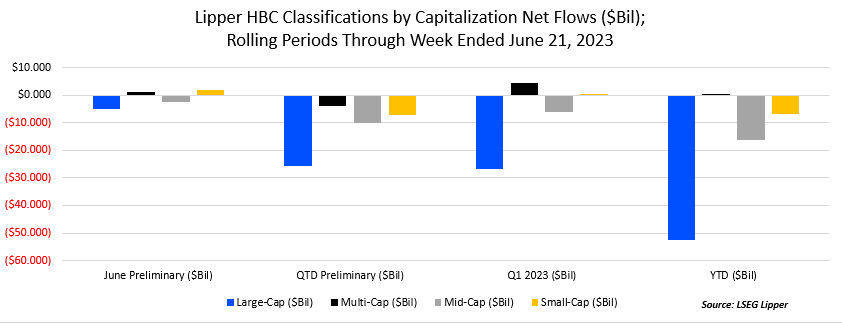

The short answer is no. Year to date multi-cap funds (+$547 million) have been the only size bucket to attract new capital, while large-(-$52.6 billion), mid-(-$16.3 billion), and small-cap (-$6.7 billion) have suffered outflows. So far this month, preliminary estimates have multi-(+$1.2 billion) and small-cap funds (+1.8 billion) as the only classification groups to see inflows.

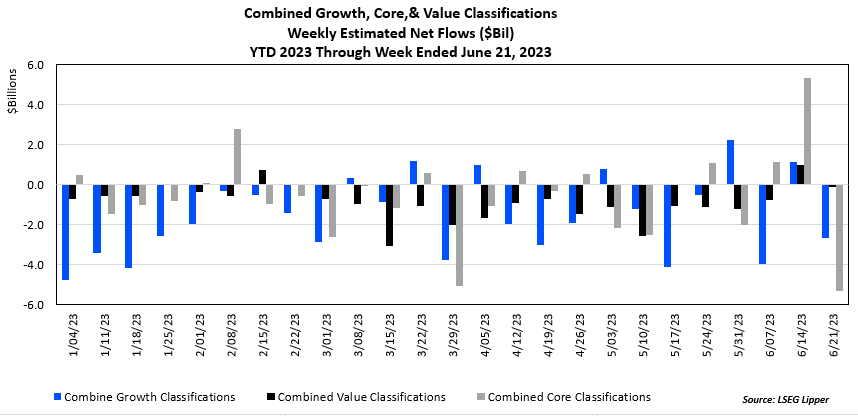

Below you can see the weekly flow totals since the start of the year for the combined classifications of growth, core, and value.

With interest rates forecasted to rise possibly another two times this year, the growth funds may not be out of the woods yet. Always a good reminder that diversification is a cornerstone of investing and performance-chasing is a hard strategy at which to consistently win.

Sources:

- Data/Charts – “LSEG Lipper”

- Commentary – “Jack Fischer, Senior Research Analyst, LSEG Lipper”

Source valuewalk

{kind=link}

{kind=link}

{kind=link}