Updated on November 29th, 2019 by Josh Arnold

Consumer goods stocks are some of the most reliable dividend payers in the stock market. The Dividend Aristocrats are a group of 57 companies in the S&P 500 Index, with 25+ consecutive years of dividend increases.

There are currently 57 Dividend Aristocrats. You can download an Excel spreadsheet of all 57 (with metrics that matter) by clicking the link below:

In addition to the downloadable spreadsheet, you can see a preview of the Dividend Aristocrats list in the table below:

| 3M Co. | 170.61 | 3.3 | 98,109 | 19.9 | 66.4 | 1.08 |

| A. O. Smith Corp. | 48.74 | 1.8 | 6,680 | 20.1 | 36.3 | 0.91 |

| Abbott Laboratories | 85.42 | 1.5 | 150,971 | 46.0 | 68.9 | 1.04 |

| AbbVie, Inc. | 88.33 | 4.8 | 130,624 | 40.5 | 196.3 | 0.89 |

| Aflac, Inc. | 54.82 | 2.0 | 40,238 | 13.5 | 26.3 | 0.72 |

| Air Products & Chemicals, Inc. | 236.04 | 1.9 | 52,012 | 29.6 | 57.4 | 0.81 |

| Archer-Daniels-Midland Co. | 42.94 | 3.2 | 23,904 | 20.3 | 65.5 | 0.83 |

| AT&T, Inc. | 37.66 | 5.4 | 275,106 | 16.8 | 91.0 | 0.61 |

| Automatic Data Processing, Inc. | 171.48 | 1.8 | 74,199 | 31.4 | 57.8 | 1.01 |

| Becton, Dickinson & Co. | 260.40 | 1.2 | 70,296 | 65.8 | 77.8 | 1.00 |

| Brown-Forman Corp. | 68.72 | 1.0 | 32,816 | 40.0 | 38.2 | 0.71 |

| Cardinal Health, Inc. | 55.22 | 3.5 | 16,151 | -3.9 | -13.6 | 0.93 |

| Caterpillar, Inc. | 145.69 | 2.5 | 80,516 | 13.7 | 34.0 | 1.37 |

| Chubb Ltd. | 152.08 | 1.9 | 68,922 | 19.1 | 37.2 | 0.62 |

| Chevron Corp. | 118.07 | 4.0 | 223,255 | 16.8 | 66.8 | 0.84 |

| Cincinnati Financial Corp. | 107.40 | 2.1 | 17,546 | 19.1 | 39.3 | 0.71 |

| Cintas Corp. | 260.32 | 1.0 | 26,943 | 29.9 | 29.3 | 1.01 |

| The Clorox Co. | 148.95 | 2.7 | 18,693 | 23.3 | 63.2 | 0.46 |

| The Coca-Cola Co. | 53.95 | 2.9 | 231,148 | 29.8 | 87.9 | 0.44 |

| Colgate-Palmolive Co. | 67.68 | 2.5 | 58,004 | 25.1 | 62.9 | 0.56 |

| Consolidated Edison, Inc. | 86.73 | 3.4 | 28,831 | 20.4 | 69.0 | 0.24 |

| Dover Corp. | 112.10 | 1.7 | 16,284 | 25.0 | 43.1 | 1.11 |

| Ecolab, Inc. | 186.95 | 1.0 | 53,887 | 35.3 | 34.8 | 0.80 |

| Emerson Electric Co. | 74.44 | 2.6 | 45,345 | 19.9 | 52.3 | 1.18 |

| Exxon Mobil Corp. | 68.70 | 4.9 | 290,677 | 20.0 | 98.5 | 0.91 |

| Federal Realty Investment Trust | 132.40 | 3.1 | 10,082 | 39.3 | 122.1 | 0.53 |

| Franklin Resources, Inc. | 27.88 | 3.7 | 13,886 | 11.8 | 44.1 | 1.13 |

| General Dynamics Corp. | 182.35 | 2.2 | 52,754 | 15.6 | 34.2 | 0.91 |

| Genuine Parts Co. | 105.21 | 2.9 | 15,286 | 19.2 | 55.0 | 0.77 |

| Hormel Foods Corp. | 44.88 | 1.9 | 23,964 | 24.5 | 45.9 | 0.51 |

| Illinois Tool Works, Inc. | 175.11 | 2.3 | 56,281 | 23.0 | 53.3 | 1.22 |

| Johnson & Johnson | 137.75 | 2.7 | 362,540 | 26.0 | 69.7 | 0.60 |

| Kimberly-Clark Corp. | 136.26 | 3.0 | 46,710 | 23.2 | 69.7 | 0.48 |

| Leggett & Platt, Inc. | 52.62 | 3.0 | 6,924 | 23.6 | 70.0 | 1.09 |

| Linde Plc | 206.00 | 1.7 | 110,658 | 21.1 | 35.3 | 0.78 |

| Lowe's Cos., Inc. | 118.46 | 1.7 | 90,977 | 31.3 | 54.4 | 1.04 |

| McCormick & Co., Inc. | 169.43 | 1.3 | 22,519 | 31.9 | 41.9 | 0.40 |

| McDonald's Corp. | 196.30 | 2.4 | 147,832 | 25.5 | 60.3 | 0.42 |

| Medtronic Plc | 112.47 | 1.8 | 150,752 | 32.3 | 59.7 | 0.66 |

| Nucor Corp. | 56.40 | 2.8 | 17,101 | 9.6 | 27.3 | 1.17 |

| People's United Financial, Inc. | 16.47 | 4.3 | 7,314 | 12.5 | 53.6 | 0.96 |

| Pentair Plc | 44.34 | 1.6 | 7,453 | 21.5 | 34.7 | 1.21 |

| PepsiCo, Inc. | 135.91 | 2.8 | 189,516 | 15.4 | 42.7 | 0.53 |

| PPG Industries, Inc. | 129.19 | 1.5 | 30,548 | 25.4 | 38.3 | 0.92 |

| Procter & Gamble Co. | 121.76 | 2.4 | 303,646 | 75.6 | 181.8 | 0.55 |

| Roper Technologies, Inc. | 362.80 | 0.5 | 37,752 | 32.6 | 16.6 | 1.04 |

| S&P Global, Inc. | 265.50 | 0.8 | 64,888 | 31.3 | 26.0 | 0.98 |

| The Sherwin-Williams Co. | 584.86 | 0.7 | 53,987 | 38.6 | 28.0 | 0.88 |

| Stanley Black & Decker, Inc. | 158.80 | 1.7 | 24,139 | 34.1 | 57.3 | 1.55 |

| Sysco Corp. | 81.06 | 1.9 | 41,359 | 24.5 | 47.2 | 0.51 |

| T. Rowe Price Group, Inc. | 123.71 | 2.4 | 28,908 | 15.5 | 37.3 | 1.22 |

| Target Corp. | 125.90 | 2.1 | 63,790 | 20.0 | 41.2 | 0.85 |

| United Technologies Corp. | 148.82 | 2.0 | 128,446 | 24.9 | 49.2 | 1.13 |

| VF Corp. | 89.05 | 2.2 | 35,564 | 27.4 | 60.3 | 1.16 |

| W.W. Grainger, Inc. | 319.24 | 1.8 | 17,196 | 18.5 | 32.5 | 1.06 |

| Walmart, Inc. | 118.76 | 1.8 | 337,786 | 23.6 | 41.9 | 0.61 |

| Walgreens Boots Alliance, Inc. | 60.11 | 3.0 | 53,650 | 13.9 | 41.2 | 1.04 |

| Name | Price | Dividend Yield | Market Cap ($M) | Forward P/E Ratio | Payout Ratio | Beta |

Each year, we review all 57 Dividend Aristocrats. The next stock in the series is consumer products manufacturer The Clorox Company (CLX).

Clorox has one of the longest streaks of dividend increases in the market as the company has raised its dividend for 42 years in a row.

This article will provide an in-depth review of Clorox’s business model, and future outlook.

Business Overview

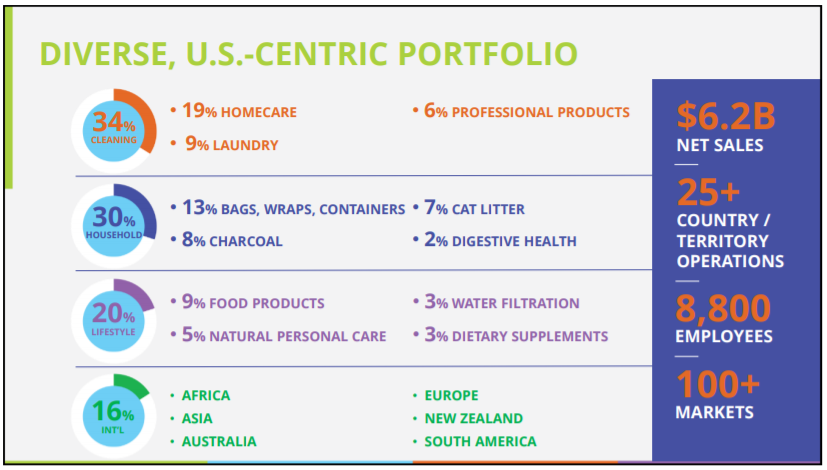

Clorox started out over 100 years ago, with the debut of its namesake liquid bleach in 1913. Today, it is a global manufacturer of consumer and professional products than collectively span a wide variety of uses and customers. The company produces annual revenue in excess of $6 billion and it sells its products in more than 100 markets.

Source: Investor presentation, page 6

The company has a highly diverse set of businesses with myriad brands and products within each, providing Clorox with huge global scale. The company’s largest segment is homecare, which is part of the core Cleaning segment. However, Clorox is much more than a cleaner company as it produces food, pet products, charcoal, and a wide variety of other brands.

The Household segment includes the Glad, Kingsford, Fresh Step, and Renew Life brands. Cleaning products include Clorox, Pine-Sol, and the Clorox Commercial Solutions businesses. Lifestyle brands include Hidden Valley, Burt’s Bees, and Brita. Lastly, the International segment sells Clorox’s brands around the world.

The strength of Clorox’s business model lies in its industry-leading brands. Consider the market share held by the following brands:

Source: Investor presentation, page 8

Many of Clorox’s brands hold the #1 or #2 market share in their respective product categories. In fact, more than 80% of its total revenue comes from products that fit this description. This results in pricing power, and high profit margins. The company states that two-thirds of its portfolio of brands have stable or growing household penetration, so organic growth should be easier to come by in the coming years.

Despite this, for several years, Clorox had a tough time growing the top line. In fact, from 2009 to 2016, Clorox managed just 0.8% compounded revenue growth annually as it struggled with volume. Decent top line growth in fiscal 2017 and 2018, respectively, gave way to a fractional increase of just 1.4% in fiscal 2019, which concluded in the summer of calendar 2019.

In the most recent quarter, Clorox reported a total revenue decline of 4% year-over-year as organic sales fell 2%, while forex translation produced a 2% headwind of its own. Clorox said higher trade promotion spending and unfavorable mix caused the lower top line, but was somewhat offset by higher prices. Still, it is clear that Clorox, after a couple of years of decent growth, is back to struggling with top line production.

Clorox has always had a fanatical obsession with improving margins, and that hasn’t changed. Gross margins were up 60 basis points in Q1 despite the weak sales figures, due to the ongoing benefits of cost saving programs and higher pricing. The higher promotional spending and higher operating costs did offset some of that gain, however.

Earnings were $203 million in Q1, good for $1.59 per share. These were both declines against last year’s Q1 at $210 million and $1.62, respectively, however. As a result, Clorox cut its guidance for this year to $6.05 to $6.25 in earnings-per-share, and our estimate is now for $6.15.

Growth Prospects

Looking ahead, Clorox has some levers it can pull to continue its recent growth. The company is continuously innovating with product extensions on its current lineup, such as flavors and cross-branding. It has done those things for a long time and will continue to do so in order to stay competitive. However, it is also focusing its mergers and acquisitions on companies that are growing, focused in the US, and are margin-accretive. Clearly, the company wants to boost domestic growth and margins through acquisitions.

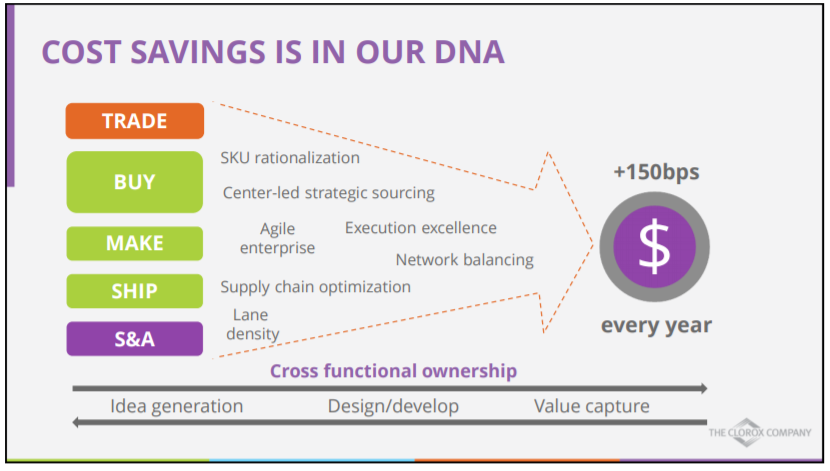

Clorox is taking a prudent approach by buying companies with a better margin profile than its existing portfolio, which boosts revenue and margins simultaneously. This is congruent with the company’s constant focus on driving every basis point of margin from each product, which has served it well during the recent top line weakness.

Source: Investor presentation, page 60

Clorox is boosting margins via productivity and waste improvements each year as well, continuing to increase operating margins for many years. The company’s focus on cost savings, combined with its accretive M&A strategy, should continue to drive earnings growth for years to come. In fact, the company recently boosted its already-ambitious target of 150 bps of annual operating margin gains to 175 bps annually. Clorox thinks it has the runway through a variety of initiatives – seen above – to move the needle in a big way on operating profits. This should help offset any revenue weakness we see in the coming years.

Longer-term, management sees revenue growth at 3% to 5% annually and small yearly improvements in operating margins. We forecast just 3% earnings-per-share gains in the coming years as we are cautious on the top line, but share repurchases combined with small margin improvements should help keep earnings-per-share moving in the right direction.

Competitive Advantages & Recession Performance

Clorox has multiple competitive advantages. First, it holds a tremendously strong brand portfolio. As previously mentioned, Clorox products enjoy very high market share across the portfolio.

Clorox retains its high industry position in part through advertising and it spends very heavily to maintain that position. Product marketing is a necessity for consumer products manufacturers and Clorox spends 10% of its revenue on this each year.

Another advantage of Clorox’s business model is that its products are used by millions of people each day, in good economies and bad. According to the company, Clorox-branded products are in about two-thirds of U.S. households.

There will always be a certain level of demand for household cleaning products and food, even if the economy enters a downturn. This allows the company to remain profitable during recessions. Indeed, Clorox is a strong example of a defensive stock. Its earnings-per-share through the Great Recession are shown below:

- 2007 earnings-per-share of $3.23

- 2008 earnings-per-share of $3.24 (0.3% increase)

- 2009 earnings-per-share of $3.81 (18% increase)

- 2010 earnings-per-share of $4.24 (11% increase)

As you can see, Clorox increased earnings-per-share each year throughout the recession, including double-digit earnings growth in 2009 and 2010. This demonstrates the company has a very recession-resistant business model and a high level of safety.

Valuation & Expected Returns

Clorox trades for a price-to-earnings ratio of 23.6, which is well in excess of our estimate of fair value of 19 times earnings. As the stock is trading at 124% of fair value, we see it as overvalued. We believe the valuation will drift lower over time as current growth rates simply do not support a valuation of 23+ times earnings.

In our view, this introduces the distinct risk of a lower valuation in the years to come, which would have significantly negative impacts on shareholder returns. Indeed, should the stock return to 19 times earnings from the current valuation of 23.6, it would produce a ~4% annual headwind to total returns.

We see total shareholder returns at just ~2% thanks in part to this, combined with the 3% forecast earnings growth and the 2.9% current yield. As a result, we see the stock as a sell at current prices despite the improvements the company has made in recent years.

The slate of growth in front of Clorox doesn’t support the current valuation, and we think that is enough to avoid the stock altogether at current prices. While we view the increase in the margin growth target as a positive, it is very clear Clorox is continuing to struggle to generate sustainable top line growth.

Final Thoughts

Clorox is a reliable dividend stock. The company has a leadership position across its product markets, with potential for some measure of growth. Right now does not appear to be a good buying opportunity, as Clorox stock trades significantly above its 10-year average and at ~124% of our fair value estimate.

The company should be able to continue its four-decade long streak of annual dividend raises regardless of the overall economic climate. However, the valuation is enough for us to rate the stock a sell and to recommend those interested in owning it to wait for a much lower valuation.

{kind=link}

{kind=link}

{kind=link}