Published by Bob Ciura on July 26th, 2017

Blue chip stocks are generally associated with quality.

They may not be the most exciting stocks to buy, but their strong business models and consistent dividends make them very rewarding to own over the long-term.

For these purposes, the term ‘blue chip’ refers to stocks that have paid a dividend for at least 100 years, and also have at least a 3% dividend yield.

You can see the full list of blue chip stocks here.

International Business Machines (IBM) is on the list.

While IBM is struggling through a difficult and prolonged turnaround, it continues to enjoy a strong reputation in its industry, and a highly profitable business model.

If the company’s turnaround is successful, it could generate strong returns. The stock is cheap, and offers a 4% dividend yield.

Plus, IBM has increased its dividend for 22 years in a row. It is a Dividend Achiever, which have raised their dividends for 10+ consecutive years. You can see all 265 Dividend Achievers here.

This article will discuss why IBM is still a blue-chip stock.

Business Overview

IBM’s stock price has under-performed for an extended period. The share price is lower today than it was five years ago.

The reason for this is because IBM’s revenue has declined for 21 quarters in a row.

On July 18th, IBM reported fiscal second-quarter results. Revenue fell 4.7% year over year. Earnings-per-share declined 5% year over year.

However, IBM’s operating earnings-per-share, which excludes non-recurring costs such as restructuring expenses, increased 1% to $2.97.

Conditions are tough for IBM, for a number of reasons. First, the company is undergoing a huge business transformation.

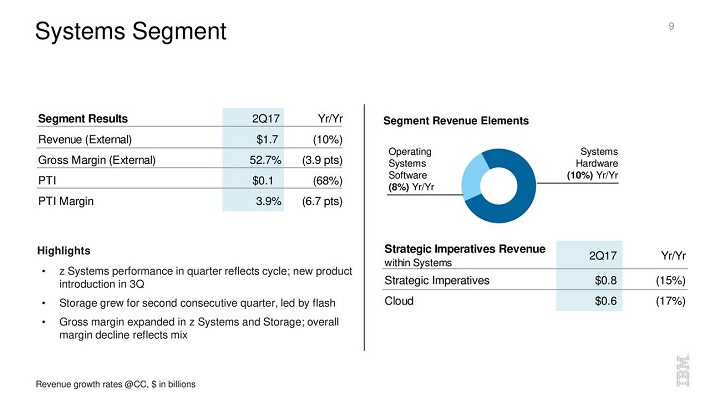

IBM is still weighed down by older, slowing legacy businesses. An example of this is the Systems segment, which is still heavily reliant on hardware.

Source: Q2 Earnings Presentation, page 9

This is one of IBM’s worst-performing segments. Revenue declined 10% last quarter, as hardware revenue fell 10% year over year.

In response, IBM has made divestments across its legacy portfolio over the past several years.

Some of IBM’s divestitures include System X, its customer care business, and its semiconductor manufacturing segment.

IBM is also suffering from the strong U.S. dollar. With a huge presence in the international markets, IBM is exposed to currency risk.

Last quarter, currency exchange reduced revenue by 1.4%.

A weaker dollar going forward would be a tailwind for IBM’s revenue.

However, underneath the revenue declines, IBM’s turnaround is gaining momentum.

Growth Prospects

IBM’s restructuring is making the company leaner, and more efficient.

The company noted in last year’s annual report that its divestments have trimmed $8 billion off the top line, but nothing off the bottom line.

In other words, IBM is shedding commoditized businesses, that were barely profitable. In exchange, it is investing aggressively in its “strategic imperatives”. IBM uses the term to describe its growth businesses, which include the cloud, data, and security.

This is the foundation of IBM’s turnaround strategy.

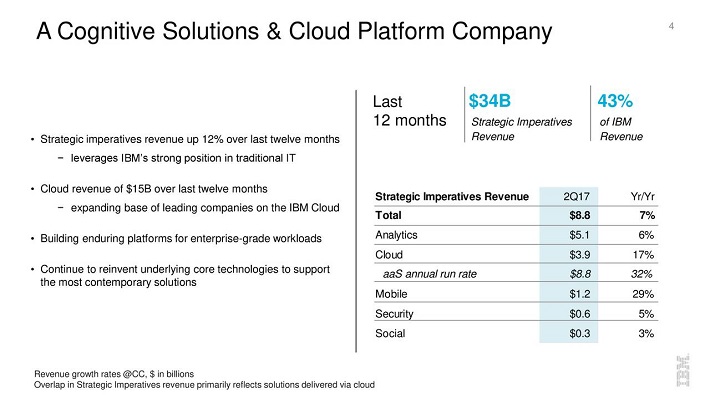

Source: Q2 Earnings Presentation, page 4

As IBM sheds its low-margin commoditized business segments, the strategic imperatives are gradually becoming a bigger piece of the overall company.

In the past four reported quarters, IBM has generated $34 billion of strategic imperative revenue, which now represents 43% of total revenue. Strategic imperative revenue is up 12% in the past year.

The benefit of this strategy over the long-term, is that IBM can focus on profitable growth. While the various divestments have caused overall revenue to decline, earnings and free cash flow are improving.

For example, IBM’s free cash flow increased 13% last quarter, to $2.6 billion.

Its divestments have freed up cash flow that would have been used on its commoditized businesses. Instead, IBM can reallocate growth investment toward its strategic imperatives.

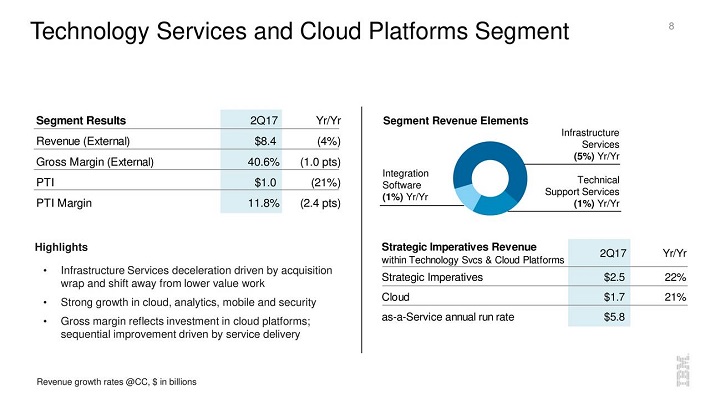

IBM’s Technology Services business is an example of this. Segment strategic imperative growth was 22% last quarter, including 21% cloud growth.

Source: Q2 Earnings Presentation, page 8

This allows IBM to continue investing in future growth, both organically and with M&A. The company spent nearly $6 billion last year, on 15 separate acquisitions.

It can do this because of its considerable financial resources, and strong balance sheet. IBM ended last quarter with $12.3 billion of cash and equivalents, up 16% from the same point last year.

Its acquisitions are focused on three specific growth areas: cognitive, cloud, and security services. This will help accelerate future growth.

For 2017, IBM expects operating earnings-per-share to increase 1.5%. If the portfolio transformation continues, earnings growth could accelerate in 2018.

Competitive Advantages & Recession Performance

Many companies have to transform their business models over time, particularly in the technology industry. Some turnarounds are successful, some are not.

In this case, it helps that IBM has a strong competitive advantage in its industry, which is its strong brand.

In the 2017 Forbes list of the world’s most valuable brands, IBM places 13th. IBM’s brand is reportedly worth $33.3 billion.

The second competitive advantage for IBM is its intellectual property.

IBM has a massive patent portfolio. IBM has led the U.S. in patents earned for 24 years in a row, exceeding 8,000 awarded patents last year alone.

Its patent portfolio is the result of significant investments in research and development. IBM typically invests 6%-7% of annual revenue on R&D.

Last year, R&D investments nearly reached $6 billion.

This provides for innovation, which has helped IBM build a durable business model.

Its financial performance during the Great Recession is as follows:

- 2007 earnings-per-share of $7.18

- 2008 earnings-per-share of $8.93

- 2009 earnings-per-share of $10.01

- 2010 earnings-per-share of $11.52

Thanks to its competitive advantages, IBM remains highly profitable, even during recession.

And, the fact that IBM actually grew earnings-per-share in each year of the recession, is even more impressive.

Valuation & Expected Total Returns

At its current share price, IBM trades for a price-to-earnings ratio of 10.7, based on 2016 operating earnings-per-share.

This is a significant discount to the S&P 500 Index, which has an average price-to-earnings ratio of 25.

IBM holds a low valuation because of its declining revenue over the past several years.

However, as previously mentioned, IBM’s turnaround strategy revolves around focusing on profitable growth. IBM is seeing most of its cloud growth hit the bottom line.

If earnings-per-share continue to grow, IBM could see its valuation multiple expand.

In addition to a rising price-to-earnings ratio, IBM’s future returns will be generated by earnings growth and dividends.

A potential breakdown of future returns is as follows:

- 1%-2% revenue growth

- 1% margin expansion

- 2%-3% share repurchases

- 4% dividend yield

Even with very weak revenue growth assumptions, IBM could generate total returns of 8%-10% per year.

IBM’s cash returns will meaningfully contribute to its total shareholder return.

IBM has a current dividend yield of 4.1%. This is a high yield, particularly for a blue chip with IBM’s brand strength.

IBM has paid a dividend since 1913. The company has demonstrated an ability to keep paying dividends, through every economic cycle.

Final Thoughts

IBM’s continued revenue declines are getting all of the attention. But underneath the surface, the shift toward profitable growth continues.

The strategic imperatives are nearing 50% of IBM’s total revenue. If the turnaround remains on track, IBM could see a return to revenue growth in 2018.

In the meantime, the company continues to grow earnings and free cash flow, which means it will be able to keep raising its dividend.

With a low valuation, 4% dividend yield, and a strong brand, IBM remains a blue-chip stock.

{kind=link}

{kind=link}

{kind=link}