Published by Bob Ciura on July 26th, 2017

Investors looking for stable dividends should first look at blue-chip stocks.

When we use the term ‘blue chip’, we are referring to stocks with 100+ years of dividend payments to shareholders, and at least a 3% current dividend yield.

Stocks that have both of these qualities have an ideal mix of dividend history, and high yield.

We have compiled a list of stocks that satisfy these two requirements. You can see the full list of blue chip stocks here.

Phillips 66 (PSX) is on the list, and is arguably the strongest blue-chip stock in the refining industry.

Through its predecessor companies, Phillips 66 dates all the way back to 1875.

The company has raised its dividend every year since its 2012, when it was spun-off from ConocoPhillips (COP).

With four more years of dividend hikes, it will become a Dividend Achiever, a group of stocks with dividend increases for 10+ consecutive years. You can see all 265 Dividend Achievers here.

And, Phillips 66 has an attractive current dividend yield of 3.3%.

This article will discuss what makes Phillips 66 a blue-chip dividend stock.

Business Overview

Phillips 66 is a diversified downstream company. Its core business is refining, which processes crude oil and other feedstocks into petroleum products, such as gasoline, diesel, and aviation fuel.

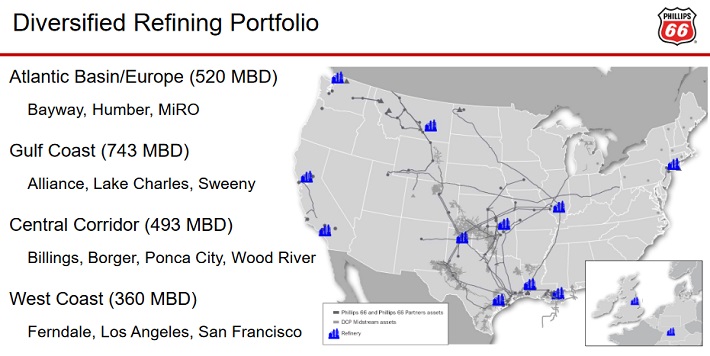

The company operates 13 refineries, 11 of which are located in the U.S., with a total crude oil processing capacity of 2.2 million barrels per day.

Phillips 66’s assets stretch across the U.S., and have access to some of the premier refining areas of the country.

Source: May 2017 Investor Presentation, page 14

Phillips 66 has four business segments:

- Midstream (9% of operating earnings)

- Chemical (34% of operating earnings)

- Refining (14% of operating earnings)

- Marketing & Specialties (43% of operating earnings)

As a downstream company, refining, marketing, and chemicals make up the vast majority of its earnings.

Last year was a difficult one for Phillips 66. Adjusted earnings, which exclude non-recurring items, declined by 64% in 2016, to $1.5 billion.

Fortunately, Phillips 66 has posted better results to start 2017.

For the first quarter, earnings-per-share fell 16% from the same quarter last year. However, adjusted earnings-per-share of $0.56 came in well above analyst expectations, which called for just $0.03 per share.

Revenue of $23.7 billion for the quarter also beat analyst estimates, by $1.4 billion. Phillips 66 generated growth across its Midstream, Chemicals, and Refining businesses.

Phillips 66’s improving performance in 2017 could set the stage for a return to growth this year and beyond.

Growth Prospects

The company is performing ahead of expectations so far this year, in large part because it has completed several major turnarounds ahead of schedule.

Refining margins are starting to improve, which is a significant catalyst for future growth. Last quarter, refining margin expanded 32%, from $6.47 per barrel to $8.55 per barrel.

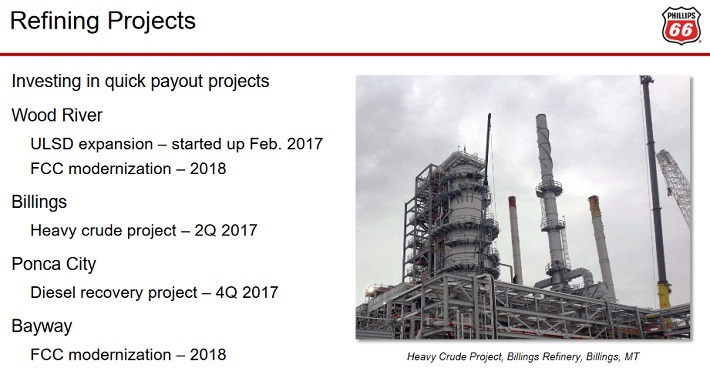

Continued new project ramp-ups should provide additional growth.

Source: May 2017 Investor Presentation, page 16

Phillips 66 has a track record of making accretive investments.

The company is a strong allocator of capital. From 2009-2016, it generated a return on capital employed of 11% per year.

Going forward, the company has several projects in the pipeline. Phillips 66 aims to invest in quick-payout projects, which have shorter completion times and higher projected rates of return.

Exports are a separate catalyst for Phillips 66.

Last quarter was the first full quarter of operation for the Freeport LPG Export Terminal.

Source: March 2017 Investor Update Presentation, page 7

The Freeport LPG Export Terminal took four years to develop, and will take supply from Phillips 66’s Sweeny fractionator and Clemens storage facility.

Capacity of the Freeport LPG Export Terminal is projected at 150,000 barrels per day.

Phillips 66 is also investing in its marketing business, with a focus on stable, highly profitable segments. For example, the company is expanding its European retail sites by 25-30 sites per year.

Competitive Advantages & Recession Performance

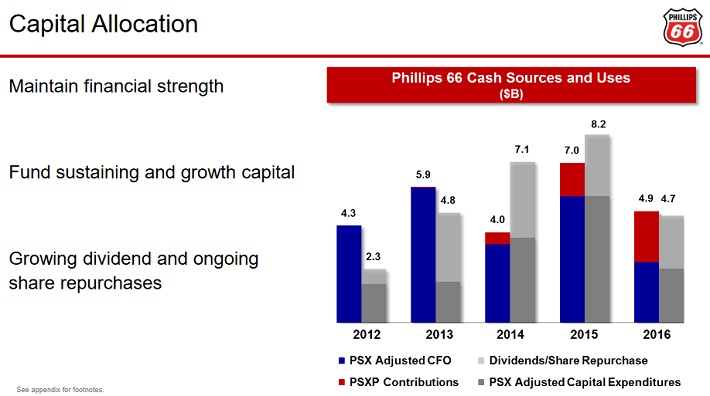

Phillips 66’s competitive advantages stem from its high-quality asset network. For example, Phillips 66 saw record refining capacity utilization last year, at 96%.

Its strong assets generate high levels of free cash flow for the company, which allows Philips 66 to invest significant resources in its growth projects.

Source: May 2017 Investor Presentation, page 20

The company expects $2.3 billion in capital expenditures for 2017, $1.3 billion of which will be utilized for growth capex.

This spending will help bring future projects online, which will generate future cash flow.

Phillips 66 was not a publicly-traded stock during the Great Recession, so its earnings from 2007-2009 are unknown.

However, it stands to reason the company would hold up relatively well during a recession. Since oil prices typically decline during recessionary periods, and Philips 66 tends to benefit from sharp declines in the price of oil.

Valuation & Expected Total Returns

Based on 2016 results, Phillips 66 trades for a price-to-earnings ratio of 28. However, last year was an anomaly, with depressed earnings.

For 2017, analysts expect Phillips 66 will generate earnings-per-share of $4.70. Therefore, the stock trades for a price-to-earnings ratio of approximately 17, based on 2017 forecasts.

Earnings-per-share are expected to continue growing in 2018. Because of this anticipated growth, Phillips 66 does not appear to be overvalued.

A reasonable breakdown of long-term total returns is as follows:

- 6%-8% operating earnings growth

- 1% share repurchases

- 3% dividend yield

Under this scenario, total annual returns would reach 10%-12%.

The dividend will be a significant piece of the puzzle. Phillips 66 is a strong dividend growth company. On May 3rd, Phillips 66 increased its dividend by 11%.

Source: May 2017 Investor Presentation, page 21

According to the company, since the first dividend after its IPO, Phillips 66 in 2012 has increased the dividend seven times, at a compound annual growth rate of 30%.

Despite the volatility of Phillips 66’s earnings in recent periods, the company should be able to continue raising its dividend each year.

The company has a strong balance sheet, with an investment-grade credit rating of BBB+ from Standard & Poor’s.

And, including its midstream segment Phillips 66 Partners (PSXP), the consolidated debt-to-capital ratio is a manageable 30%.

Final Thoughts

There is no official definition of a blue-chip stock, but Phillips 66 seems to fit the bill. It has a highly profitable business model, strong assets, and a leadership position in its industry.

The company has had a long history of rewarding shareholders with dividends, and currently offers a 3%+ dividend yield.

As a result, Phillips 66 stands out as one of the strongest blue-chip dividend stocks in the oil and gas industry.

{kind=link}

{kind=link}

{kind=link}