Meta Pops and Microsoft Drops: A Closer Look

The 2025 Q4 earnings season continues to roll along, with a decent chunk of the S&P 500 delivering their results so far. While both earnings and sales growth has remained rock-solid so far, beats percentages are lower relative to other periods, with not all seeing favorable post-earnings reactions either.

And concerning post-earnings reactions, Meta Platforms META shares popped following its release, whereas Microsoft MSFT faced one of its worst days in years. Interestingly enough, MSFT shares now lag the S&P 500 on a five-year basis, whereas META shares have crushed.

Image Source: Zacks Investment Research

Were MSFT Earnings That Bad?

Concerning headline expectations, Microsoft posted a double-beat relative to our consensus expectations, continuing its stellar earnings streak. Adjusted EPS of $4.14 grew by 24% year-over-year, whereas sales of $81.3 billion grew 17% from the year-ago period.

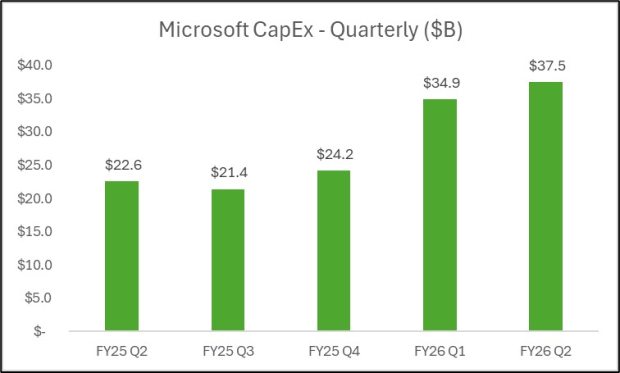

While the headline growth rates were undoubtedly impressive, investors largely took issue with the big capital expenditures geared toward its cloud and AI offerings and a slowdown in Azure growth. CapEx for the period totaled $37.5 billion, of which $29.9 billion was for property and equipment, such as GPUs and CPUs to support Azure demand.

Below is a chart illustrating MSFT’s CapEx on a quarterly basis.

Image Source: Zacks Investment Research

Many have grown skeptical of the immense capital being thrown around in the broader AI frenzy, which helps explain the poor post-earnings reaction. Investors are beginning to demand results from the investments for understandable reasons, driven by the lofty forecasts we’ve seen over the past several years.

Its Intelligent Cloud segment, which includes Azure, saw sales grow 28% year-over-year to $32.9 billion, though the segment’s gross margin took a hit due to continued AI investments.

Concerning Azure and cloud services revenue specifically, sales grew 31% year-over-year, reflecting a deceleration relative to recent growth rates of 35% and 39% across its previous two periods, respectively. For years, investors have placed a strong emphasis on accelerating cloud revenue, which has often dictated post-earnings reactions across the space, including with Amazon’s AMZN AWS.

Meta Earnings

Meta Platforms similarly posted a double-beat relative to our consensus expectations, with adjusted EPS of $8.88 climbing 11% year-over-year alongside a 24% sales increase. Up 11% year-to-date, the stock has now outperformed nicely relative to the S&P 500.

Importantly, the company continued to attract more consumers to its family of apps, with average Family Daily Active People (DAP) for December 2025 up 7% year-over-year to roughly 3.6 billion. Ad impressions, a key metric for the tech titan, grew 18% from the year-ago period, while average price per ad rose 6% from the same period last year.

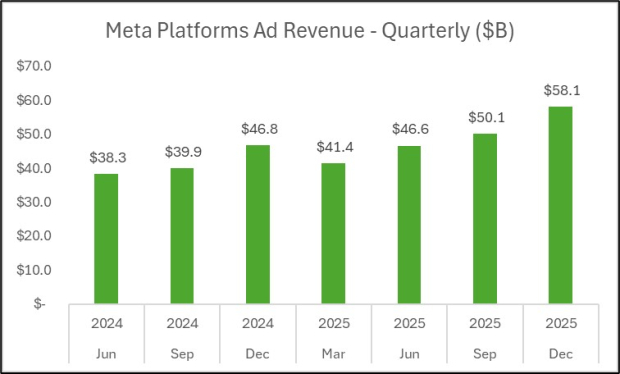

Below is a chart illustrating META’s ad revenue on a quarterly basis.

Image Source: Zacks Investment Research

Like MSFT, the company is also investing heavily in AI, as reflected in guidance for its full-year 2026. META forecasts total FY26 expenses in a band of $162 - $169 billion, of which the majority is allocated to infrastructure costs. Higher compensation for key talent to support the buildout is the second-biggest contributor to its FY26 expenses, underscoring how high a priority it remains for the company.

Putting Everything Together

Meta Platforms META and Microsoft MSFT had contrasting share reactions post-earnings, with META shares seeing positivity and MSFT shares facing a rough day on the back of steep CapEx and a deceleration in Azure.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Meta Platforms, Inc. (META): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Source Zacks-com

{kind=link}

{kind=link}

{kind=link}