ImmunityBio Valuation: Paying 33x Sales for Anktiva

ImmunityBio’s IBRX stock has re-rated sharply as Anktiva transitions from a newly launched therapy to a product with accelerating prescriptions, expanding geographies, and active label-extension work. That momentum is real, but today’s valuation assumes a lot goes right.

At current multiples, investors are effectively underwriting fast commercialization and clean execution across reimbursement, manufacturing, and regulatory follow-through. The setup leaves limited room for missteps.

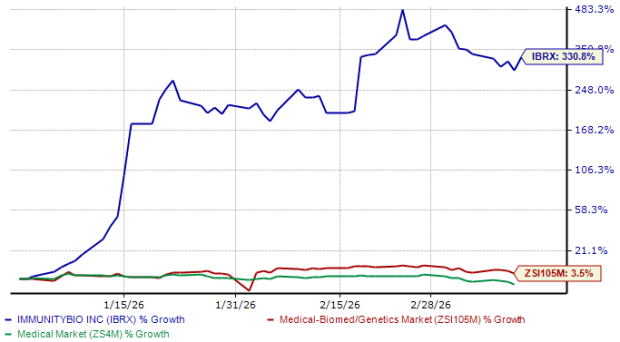

IBRX’s Run-Up and What the Market Has Priced In

ImmunityBio shares are up 330.8% year to date and 197.3% over the trailing 12 months (as of 03/12/2026). That performance stands out even more against the broader backdrop. The Zacks sub-industry is up 3.6% year to date while the sector is down 3.6%. Over the past year, the sub-industry is up 13.1% and the sector is down 1.8%.

Image Source: Zacks Investment Research

The contrast signals how much optimism has moved into IBRX specifically. In effect, the market is pricing in that Anktiva’s U.S. momentum sustains while ex-U.S. launches and ongoing expansion efforts begin to add incremental demand.

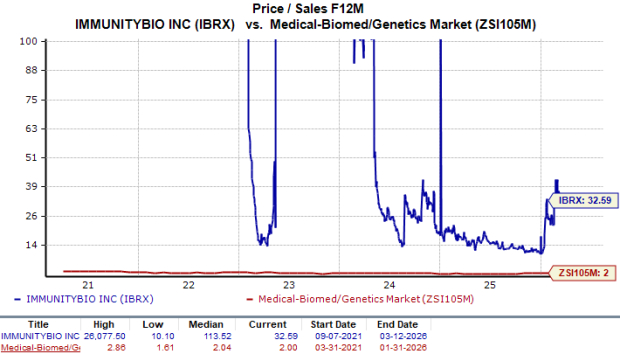

ImmunityBio’s Multiple Versus Peers Sets a High Bar

The valuation math is straightforward. IBRX trades at 32.59x forward twelve-month sales, versus 2.00x for the Zacks sub-industry, 2.28x for the Zacks sector, and 4.96x for the S&P 500. On an enterprise basis, the stock is at 33.63x forward enterprise value to sales.

Image Source: Zacks Investment Research

A sales-multiple framework matters here because management has not provided forward margin or earnings-per-share guidance. With profitability metrics not framed for investors, the multiple becomes a shorthand for how quickly Anktiva can scale revenue relative to the spending required to build the franchise.

That context also explains why competition matters, even if ImmunityBio’s growth is the main driver. Merck’s MRK Keytruda already carries an indication in BCG-unresponsive, high-risk non-muscle invasive bladder cancer (NMIBC) with carcinoma in situ (CIS), a reminder that large-cap oncology franchises are active in adjacent segments. Bristol Myers Squibb’s BMY Opdivo is approved in urothelial carcinoma settings, underscoring the intensity of the broader bladder cancer landscape.

IBRX’s Neutral Stance and What Would Change It

The current stance is Neutral, with an $8.25 price target that reflects 34.38x trailing twelve-month book value. In practical terms, that positioning implies the stock is expected to perform roughly in line with the market from here.

For investors, the “what would change it” checklist is execution-driven. First is sustained adoption in the core U.S. setting, supported by repeat prescribing and continued sequential demand signals. Second is clean commercialization work in new geographies, where access and launch details matter as much as the headline approvals.

Third is progress toward label expansion milestones already in motion. The company has an active supplemental filing seeking to broaden Anktiva plus BCG into BCG-unresponsive non-muscle invasive bladder cancer with papillary disease, following multiple interactions with the FDA. Those steps help frame what investors should monitor without stretching beyond what is already underway.

ImmunityBio’s 2025 Operating Picture Shows Mixed Leverage

The operating picture shows improving revenue traction with continued investment intensity. In the fourth quarter of 2025, total revenue was $38.3 million, up 407% year over year, and net loss per share improved to $0.06 from $0.08 a year ago.

Expenses were mixed. Research and development expense rose 81% year over year to $63.9 million, while selling, general and administrative expense declined 7% to $38.7 million. The push-and-pull fits the company’s posture: keep investing in clinical programs, manufacturing, and commercialization, while expecting net loss to narrow directionally as revenue grows.

That balance matters because the valuation assumes revenue keeps compounding even as the company builds the infrastructure needed for a broader footprint.

IBRX’s Balance Sheet and Funding Overhang

ImmunityBio ended 2025 with $242.8 million in cash, cash equivalents, and marketable securities. The balance sheet also includes significant liabilities, including related-party convertible notes and a revenue interest liability.

Those obligations matter because the near-term plan is capital-intensive by design. The company is preparing ex-U.S. launches while continuing clinical work across bladder cancer settings and other oncology indications. Europe’s model adds another layer of complexity, with country-by-country reimbursement and staged rollout priorities.

If international ramps are slower, capital intensity can stay elevated longer. In that scenario, external financing risk rises, even with management’s expectation that losses narrow as revenue scales.

ImmunityBio’s Practical “Watch List” for Buyers and Holders

In the U.S., focus on whether sequential product sales strength continues and whether repeat prescribing remains a consistent signal of real-world adoption. Net product sales rose 20% quarter over quarter in the fourth quarter, and the company emphasized repeat prescribing behavior.

In Europe, look for proof that reimbursement work is moving from planning to execution. The access strategy is country-by-country, with the Big 5 prioritized and Germany expected to be among the first launches in 2026.

On the regulatory front, monitor progress on the resubmitted supplemental application for papillary disease and any added clarity that emerges through the FDA process tied to non-muscle invasive bladder cancer expansion efforts.

What could temper upside is also clear: delayed ex-U.S. ramps, higher burn from sustained investment, or regulatory uncertainty that stretches timelines.

IBRX’s Zacks Rank

ImmunityBio currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Just Released: Zacks Top 10 Stocks for 2026

Hurry – you can still get in early on our 10 top tickers for 2026. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful.

From inception in 2012 through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2026. You can still be among the first to see these just-released stocks with enormous potential.

See New Top 10 Stocks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bristol Myers Squibb Company (BMY): Free Stock Analysis Report

Merck & Co., Inc. (MRK): Free Stock Analysis Report

ImmunityBio, Inc. (IBRX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Source Zacks-com

{kind=link}

{kind=link}

{kind=link}