Published on July 8th, 2022 by Quinn Mohammed

Berkshire Hathaway (BRK.B) has an equity investment portfolio worth over $360 billion, as of the end of the 2022 first quarter.

Berkshire Hathaway’s portfolio is filled with quality stocks. You can follow Warren Buffett stocks to find picks for your portfolio. That’s because Buffett (and other institutional investors) are required to periodically show their holdings in a 13F Filing.

You can see all Warren Buffett stocks (along with relevant financial metrics like dividend yields and price-to-earnings ratios) by clicking on the link below:

Free Excel Download: Get a free Excel Spreadsheet of all Warren Buffett stocks, complete with metrics that matter – including P/E ratio and dividend yield. Click here to download Buffett’s holdings now.

Note: 13F filing performance is different than fund performance. See how we calculate 13F filing performance here.

As of March 31st, 2022, Buffett’s Berkshire Hathaway owned more than 126 million shares of U.S. Bancorp (USB) for a market value of $6.7 billion. U.S. Bancorp represents about 1.9% of Berkshire Hathaway’s investment portfolio. This marks it as the 9th largest position in the portfolio, out of 49 stocks.

This article will analyze the financial services company in greater detail.

Business Overview

U.S. Bancorp traces its lineage back to 1863 when the First National Bank of Cincinnati opened for business. It has since grown to 70,000 employees, and about $25 billion in annual revenue.

The bank has expanded from a regional player to a national powerhouse in recent years, becoming the fifth–largest bank by assets in the U.S. It competes mostly in traditional banking activities, but also offers wealth management, payment, and investment services.

On April 14th, 2022, U.S. Bancorp reported first quarter earnings and diluted earnings-per-share came to $0.99, which was down significantly compared to $1.45 in the prior year period. Net revenue was $5.6 billion, up 2.4% year-over-year. The company’s results were positively impacted by loan growth, as well as net interest income and lower noninterest expenses.

Net interest income was $3.2 billion, up from $3.1 billion a year ago. Net interest margin was 2.44%, down from 2.50% in the first quarter of last year.

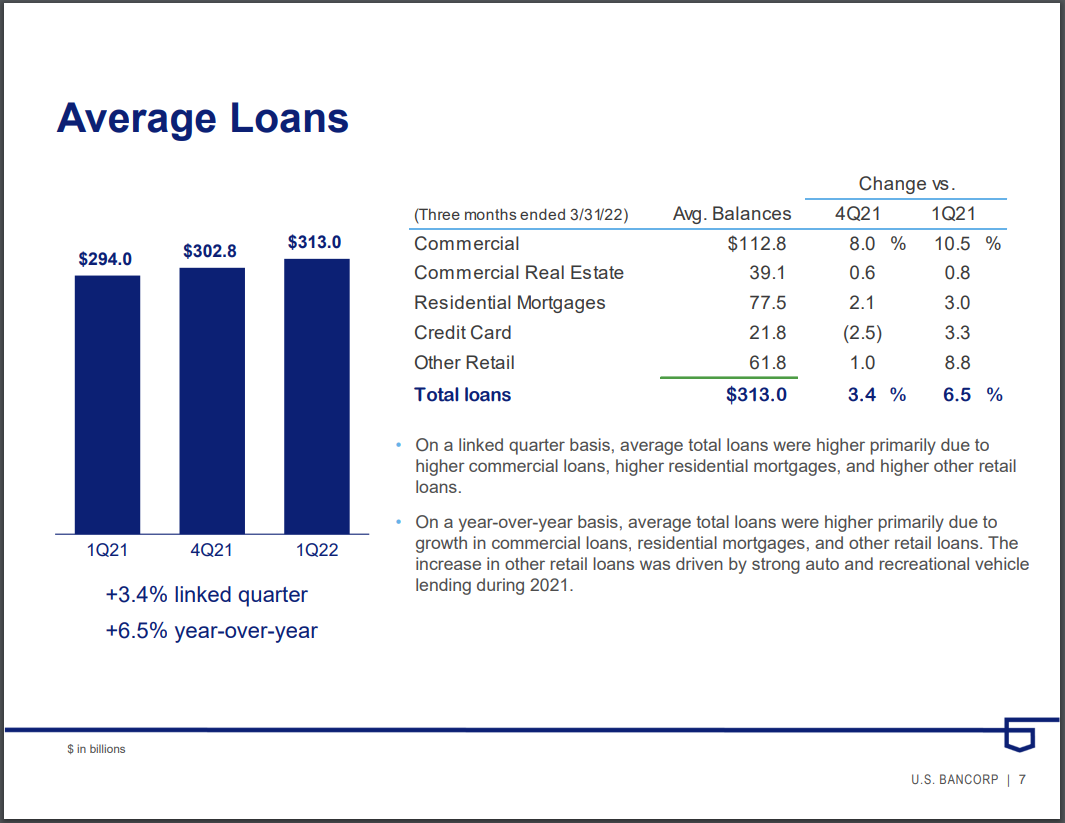

Average total loans were $313 billion, up from $303 billion in the prior quarter. Average total deposits were $454 billion, up from $450 billion in the prior quarter.

Source: Investor Presentation

Noninterest expense was $3.50 billion in the first quarter, up from $3.38 billion a year ago. Provisions for credit losses were $112 million, a huge decline from the benefit of $827 million a year ago. These provisions directly impact earnings, which clarifies a large portion of the decline in year-over-year earnings.

We estimate that U.S. Bancorp can generate $4.30 in earnings-per-share for the fiscal 2022 year.

Growth Prospects

Impressively, U.S. Bancorp has grown its earnings per share every year since 2009 until 2020, starting from the great financial crisis and ending as a result of the COVID-19 pandemic. Very few banks can claim such a record.

Rising lending rates are a growth driver for the company’s earnings, and this is set to continue in the near term. However, current low net interest margin, and moderate loan growth may weigh on the company’s growth rate.

U.S. Bancorp is also in the process of acquiring MUFG Union Bank’s core regional banking franchise from Mitsubishi UFJ Financial Group (MUFG). The purchase price is $8 billion, which includes $5.5 billion in cash and roughly 44 million shares of USB. This will provide MUFG with a 2.9% stake in U.S. Bancorp.

U.S. Bank will gain over 1 million consumer customers and roughly 190,000 small business customers on the West Coast, as a result of the acquisition. And the company anticipates adding $58 billion in loans and $90 billion in deposits based on MUFG Union Bank’s June 30th, 2021, balance sheet.

The combined entity will be a leader in serving customers in California, Washington, and Oregon. The acquisition is anticipated to be 6% accretive to earnings per share in 2023 and 8% after it is fully integrated.

U.S. Bancorp has been consistent in its share repurchases, by repurchasing 2.5% on average over the last nine and five years. Continued share repurchases should also fuel per-share results going forward.

We project that the company can continue to grow earnings by 6% annually through 2027.

Competitive Advantages & Recession Performance

U.S. Bancorp’s competitive advantage lies in its impressive operating history and first-rate management team. The company operates as a regional bank, but at tremendous scale, and for that reason, it has been more resilient through recessions than its larger peers.

While many banks struggled to remain in business during 2009 amidst the great financial crisis, U.S. Bancorp’s earnings were not even cut by half. In fact, following the recession, U.S. Bancorp was in better shape when compared to its competitors than before.

U.S. Bancorp has raised its dividend for ten consecutive years so far. We see the payout remaining below 50% of earnings in the coming years. U.S. Bancorp’s dividend appears safe, and we see no risk of a cut at this point. U.S. Bancorp last raised the dividend 9.5% to an annualized payout to $1.84. We estimate the company can continue growing the dividend at a rate of roughly 6% per annum.

Valuation & Expected Returns

Shares of U.S. Bancorp have traded for a 5- and 10-year average price-to-earnings multiple of 13.0 and 12.9, respectively. Shares are now trading below both of these averages, which indicates that shares could be undervalued at the current 10.9 times earnings. As a result, we believe there is a potential for a valuation tailwind in the intermediate term.

Our fair value estimate for USB stock is 11.5 times earnings. If this proves correct, the stock will benefit from a 3.1% annualized gain in its returns through 2027.

Shares of U.S. Bancorp currently yield 3.9%, which is above its 5- and 10-year average yields of 3.0% and 2.7%% as well. On a dividend yield basis, USB shares seem to be trading below fair value.

Putting it all together, the combination of valuation changes, EPS growth, and dividends produces total expected returns of 10.5% per year over the next five years. This makes U.S. Bancorp a buy.

Final Thoughts

U.S. Bancorp is in the midst of a massive acquisition, which will see it become a top leader in West Coast regional banking.

The company has generated an impressive track record, but took a pause during the pandemic, and then hit a new record in 2021. Following normalized results from 2022 and onward, we expect the bank to perform well.

Other Dividend Lists

Value investing is a valuable process to combine with dividend investing. The following lists contain many more high-quality dividend stocks:

- The Dividend Aristocrats List is comprised of 65 stocks in the S&P 500 Index with 25+ years of consecutive dividend increases.

- The High Yield Dividend Aristocrats List is comprised of the 20 Dividend Aristocrats with the highest current yields.

- The Dividend Achievers List is comprised of ~350 stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 44 stocks with 50+ years of consecutive dividend increases.

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The Blue Chip Stocks List: stocks that qualify as Dividend Achievers, Dividend Aristocrats, and/or Dividend Kings

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

{kind=link}

{kind=link}

{kind=link}