Updated on August 25th, 2021 by Bob Ciura

Technology stocks (or “tech stocks” for short) tend to see more volatility during the business cycle than other sectors, like consumer staples, for instance. With that said, the tech sector has tremendous upside.

Volatility can be put to good use by investors that are interested in owning big tech securities by buying at trough valuations and avoiding those trading in excess of fair value.

In addition, the largest stocks of the group often pay very respectable dividends, which help to smooth out total returns rough periods. Payout ratios tend to be lower for tech stocks as well so the dividends offer a lot of safety during downturns, increasing their appeal.

You can download the complete list of all 330+ dividend paying tech stocks available on the big US market exchanges by clicking on the link below:

The rankings in this article are derived from our expected total return estimates from Sure Analysis Research Database. The 10 largest dividend paying tech sector stocks by market cap are ranked in this article, with #10 having the lowest expected total returns and #1 having the highest.

Rankings are compiled based upon the combination of current dividend yield, expected change in valuation as well as forecast earnings-per-share growth to determine which stocks offer the best total return potential for shareholders.

Table of Contents

The top 10 stocks on this list are all dividend-paying tech stocks with yields above the S&P 500 Index average (currently 1.3%). Additionally, all 10 stocks have Dividend Risk Scores of C or better in the Sure Analysis Research Database.

You can instantly jump to any individual section of the article by clicking on the links below:

- Best Big Tech Dividend Stock #10: Computer Services, Inc. (CSVI)

- Best Big Tech Dividend Stock #9: Cisco Systems (CSCO)

- Best Big Tech Dividend Stock #8: International Business Machines (IBM)

- Best Big Tech Dividend Stock #7: Qualcomm Incorporated (QCOM)

- Best Big Tech Dividend Stock #6: Texas Instruments Incorporated (TXN)

- Best Big Tech Dividend Stock #5: Intel Corporation (INTC)

- Best Big Tech Dividend Stock #4: SAP SE (SAP)

- Best Big Tech Dividend Stock #3: HP Inc. (HPQ)

- Best Big Tech Dividend Stock #2: Hewlett Packard Enterprise Company (HPE)

- Best Big Tech Dividend Stock #1: Micro Focus International plc (MFGP)

Best Big Tech Dividend Stock #10: Computer Services, Inc. (CSVI)

Computer Services provides regional banks with a wide range of services, such as core processing, digital banking,

payments processing, and regulatory compliance solutions. It has a market cap of $1.7 billion.

In early July, Computer Services reported (7/7/2021) financial results for the first quarter of fiscal 2022. The company grew its revenue by 8% and its earnings–per–share by 2% over the prior year, to new all–time high levels. The tepid earnings growth resulted from much higher termination fees received in last year’s quarter but Computer Services maintained its strong business momentum.

Digital banking solutions enjoyed high growth thanks to the efforts of banks to support their customers online while revenues from regulatory compliance and payments processing remained strong. It is also important to note that 90% of the total revenues are generated from long–term contracts. Management expects momentum to accelerate in the second half of this year thanks to new customers coming online.

Computer Services recently increased its dividend by 8%, marking its 50th consecutive year of dividend increases. In the past 10 years the company has grown its dividend by 15.9% per year. It has also increased its revenue and net income for 21 and 24 consecutive years, respectively.

Computer Services’ impressive growth is a testament to the strength of its business model and the existence of a significant competitive advantage. The company signs multi–year contracts with its customers and offers them a wide range of services. It is thus very costly and inefficient for these customers to stop working with the company, particularly given that they pay appreciable early termination fees. As a result, Computer Services enjoys high renewal rates.

We expect 8% annual earnings-per-share growth over the next five years. The stock also has a 1.8% dividend yield. However, we view the stock as overvalued. Shares trade for a 2021 P/E ratio of 27.9, while we have a target P/E ratio of 17.4 which is equal to the 10-year average. Therefore, expected returns are just 0.4% per year due to the overvaluation of the stock.

Best Big Tech Dividend Stock #9: Cisco Systems (CSCO)

Cisco Systems is the global leader in high performance computer networking systems. The company’s routers and

switches allow networks around the world to connect to each other through the internet. Cisco also offers data center, cloud, and security products. Cisco generates about $53 billion in annual revenues.

Cisco reported earnings results for the fourth quarter and fiscal year 2021 on 8/18/2021. Quarterly revenue grew 8.1% to $13.1 billion, beating estimates by $90 million. Adjusted earnings–per–share of $0.84 increased 5% compared with the same quarter last year. For the year, revenue grew 1% to $49.8 billion while adjusted earnings–per–share was essentially flat.

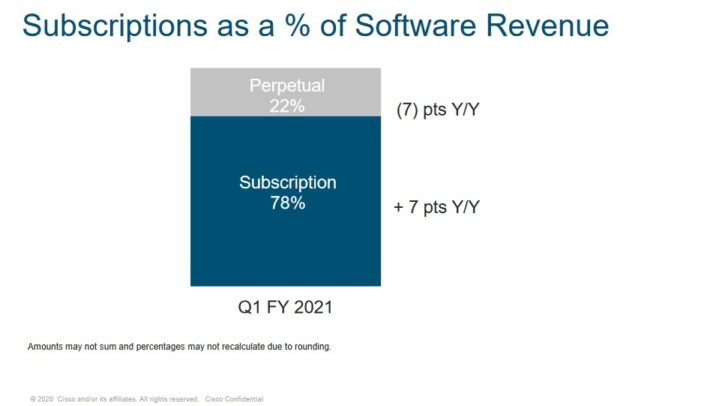

In the fiscal fourth quarter, Infrastructure Platforms and Security revenues were up 13% and 1%, respectively, while Applications fell 1%. Software subscriptions increased 9% year–over–year to $4 billion.

Source: Investor Presentation

By region, the Americas improved 8%, EMEA was higher by 6% and Asia–Pacific/Japan/China was up 13%.

We expect 6% annual EPS growth over the next five years. Share repurchases will help boost EPS growth. Cisco has $7.9 billion, or ~3% of its current market cap, remaining on its share repurchase authorization. Cisco expects first quarter of fiscal year 2022 adjusted earnings–per–share of $0.79 to $0.81.

For the fiscal year, revenue is expected to grow 7.5% to 9.5% and adjusted earnings–per–share is projected in a range of $3.38 to $3.45.

At the midpoint of guidance, Cisco shares trade for a 2021 P/E of 17.4. Our fair value estimate is a P/E of 15, which means the stock is slightly overvalued. Cisco stock has a current dividend yield of 2.5%. Overall, 5-year annual returns are expected to reach 5.4% through 2026.

Best Big Tech Dividend Stock #8: International Business Machines (IBM)

IBM is a global information technology company that provides integrated enterprise solutions for software, hardware, and services. IBM’s focus is running mission critical systems for large, multi–national customers and governments. IBM typically provides end–to–end solutions.

IBM is a dividend growth company. It has increased its dividend for 26 consecutive years, placing it on the exclusive Dividend Aristocrats list.

In the services business, IBM is the world’s largest IT provider with ~5.5% market share. In software, IBM’s software business is mostly middleware, which is the software layer that connects applications and devices to each other. In hardware, IBM sells the z15 mainframes, storage, and the Power–based servers.

The company has five business segments: Cloud & Cognitive Software, Global Business Services, Global Technology Services, Systems, and Global Financing. IBM generated annual revenue of ~$73.6B in 2020.

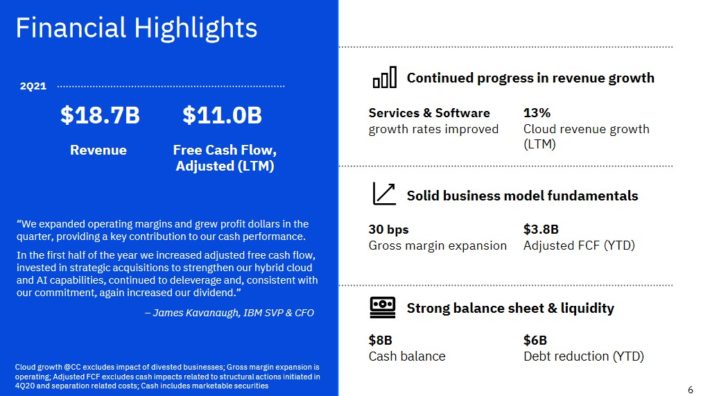

IBM reported better than expected results for Q2 2021 on July 19th, 2021.

Source: Investor Presentation

Company-wide revenue increased 3% to $18,745M from $18,123M while diluted adjusted earnings per share rose 7% to $2.33 from $2.18 on a year–over–year basis. Diluted GAAP earnings per share fell (–3%) to $1.47 in the quarter from $1.52 in the prior year.

Revenue for Cloud & Cognitive Software increased 6.1% to $6,098M from $5,748M in comparable quarters due to 12% growth in Cloud & Data, 12% growth in Cognitive but offset by a (–7%) decline in Transaction Processing. Global Business Revenue increased 11.6% to $4,341M from $3,890M due to 16% growth in Consulting, 28% growth in Global Process Services, and 5% growth in Application Management. IBM ended Q2 2021 with a backlog of $103.7B.

We expect 4% annual EPS growth for IBM, in addition to the 4.7% dividend yield. Based on expected EPS of $11.03 for 2021, shares trade for a P/E ratio of 12.7; our fair value estimate is 11. The combination of EPS growth, dividends, and a declining P/E multiple result in total expected returns of 5.7% per year.

Best Big Tech Dividend Stock #7: Qualcomm Incorporated (QCOM)

Qualcomm develops and sells integrated circuits for use in voice and data communications. The chip maker receives royalty payments for its patents used in devices that are on 3G and 4G networks. Qualcomm should generate sales of more than $33 billion this year.

Qualcomm released earnings results for the third quarter of fiscal 2021 on 7/28/2021 (the company’s fiscal year ends September 30th). Revenue grew 64.5% to $8.1 billion, beating estimates by $500 million. Adjusted earnings–per–share of $1.92 compared favorably to adjusted earnings–per–share of $0.86 in the prior year and was $0.24 better than expected.

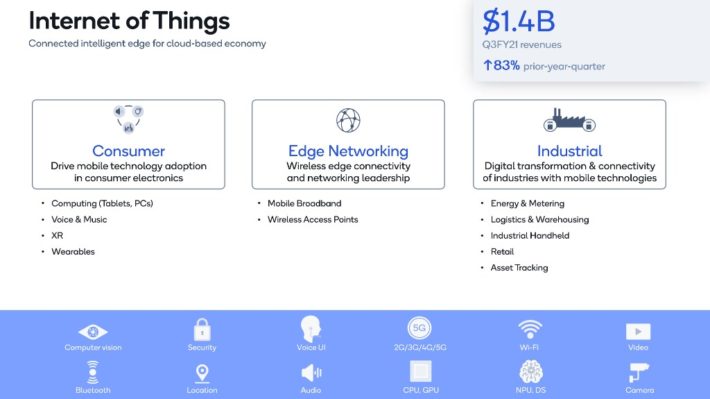

Revenues for Qualcomm CDMA Technologies, or QCT, surged 70% to $6.5 billion due to continued strength across handsets, 5G, automotive and Internet of Things businesses.

Qualcomm’s Internet of Things business will be a future growth catalyst.

Source: Investor Presentation

Separately, Qualcomm Technology Licensing, or QTL, grew 43% to $1.5 billion last quarter. The company reaffirmed its expectations that handset shipments will grow at a high single–digit rate to a range of 450 million to 550 million for calendar year 2021.

The company has grown earnings–per–share at a rate of 6.6% per year over the last decade. An agreement with Apple and Huawei, a lower share count and leadership in 5G should allow the company to grow in the coming years. We also believe that demand for 3G/4G/5G headsets will increase following a recovery from the COVID–19 pandemic. We expect 7% annual EPS growth.

Shares appear overvalued, with a 2021 P/E of 17.4 compared with our fair value estimate of 15.7. Qualcomm shares currently yield 1.9%. Overall, total returns are expected to reach 6.6% per year.

Best Big Tech Dividend Stock #6: Texas Instruments (TXN)

Texas Instruments is a semiconductor company that operates two business units: Analog and Embedded Processing. Its products include semiconductors that measure sound, temperature and other physical data and convert them to digital signals, as well as semiconductors that are designed to handle specific tasks and applications.

Texas Instruments reported its second quarter earnings results on July 21. During the quarter Texas Instruments generated revenues of $4.6 billion, which represents an increase of 41% versus the previous year’s quarter. This was the result of a revenue increase of 42% in the Analog business, while revenues in the Processing segment grew by an equally attractive 43% year–over–year.

Texas Instruments generated earnings–per–share of $1.99 during the second quarter, which was better than the analyst consensus estimate, coming in $0.14 ahead of the analyst community’s forecast.

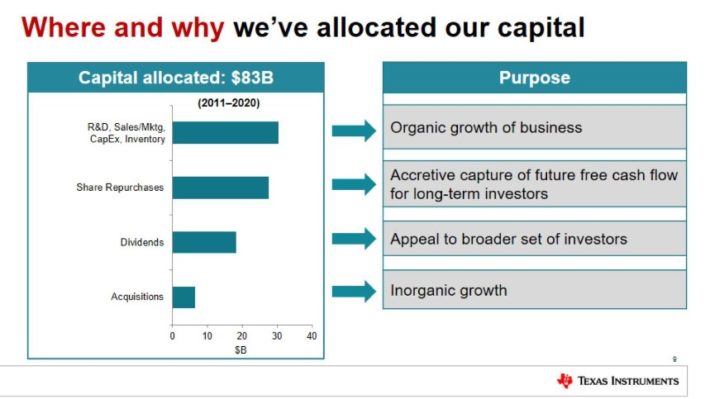

Texas Instruments has effectively allocated capital, with over $80 billion in the past 10 years spread across internal investments and acquisitions designed to generate future growth, while rewarding shareholders with buybacks and dividends.

Source: Investor Presentation

Texas Instruments’ policy of returning all free cash flows to the company’s shareholders in the form of

dividends and share repurchases affects its earnings–per–share growth, as a declining share count increases each

remaining share’s portion of all profits. Texas Instruments has bought back nearly 50% of all shares since 2004.

Through a combination of organic growth, acquisitions, and share buybacks, we expect 8% annual EPS growth for Texas Instruments through 2026.

Shares trade for a 2021 P/E of 23.5, compared with our fair value estimate of 20. This means the stock is slightly overvalued, and a declining P/E could reduce returns over the next five years. Shares also have a 2.2% dividend yield. Overall, total returns are expected to reach 6.9% per year for Texas Instruments.

Best Big Tech Dividend Stock #5: Intel Corporation (INTC)

Intel is the largest manufacturer of microprocessors for personal computers, shipping about 85% of the world’s microprocessors. Intel also manufactures products like servers and storage devices that are used in cloud computing. Intel generates about $73 billion in annual sales.

Intel reported second quarter earnings results on 7/22/2021. Revenue grew 2% to $18.5 billion, which was $700 million above expectations. Adjusted earnings–per–share of $1.28 was a $0.05, or 4.1%, improvement from the prior year and beat estimates by $0.21.

The PC–Centric business remains very strong as revenue grew 6% to $10.1 billion. PC volumes grew 33% year–over–year, which were partially offset by declines in average selling prices.

The other businesses remain mixed. Data Center Group fell 9% to $6.5 billion, primarily due to weaker results in the cloud business. Internet of Things Group grew 47% to $984 million as this segment benefited from a recovery from COVID–19.

Intel again offered revised guidance for 2021. The company expects earnings–per–share of $4.80 for the year, up from $4.60 previously.

Intel’s key competitive advantage is that it is the largest and most dominant company in its sector. This gives the

company size and scale that competitors can’t match.

We see total returns at 8.8% annually for Intel going forward. This will consist of the current 2.6% dividend yield, 5% expected EPS growth and a small boost from a rising valuation multiple.

Best Big Tech Dividend Stock #4: SAP SE (SAP)

SAP SE develops, sells, and maintains a variety of enterprise software products that are used by corporations, governments, and educational agencies. The company has more than 400,000 customers in 180 countries. SAP is headquartered in Germany and reports financial results in Euros. American investors can initiate an ownership stake in SAP through American Depository Receipts.

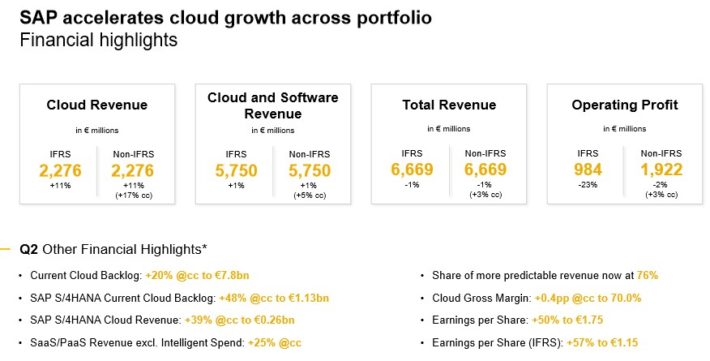

SAP reported its second quarter earnings results on July 21. The company recorded revenues of €6.7 billion during the quarter, which is equal to $7.9 billion. SAP’s revenues during the quarter were down 1% year over year, which missed the analyst consensus estimate slightly.

Source: Investor Presentation

SAP’s cloud revenue growth accelerated during the quarter, which is why SAP is now forecasting cloud revenue growth of 15% to 18% for the year. Cloud revenue growth was not high enough to offset declining software revenues, however. SAP’s operating profit started to climb again during the quarter.

SAP’s earnings–per–share totaled €1.75, or $2.07 on an adjusted basis during the second quarter. This represents a 50% increase year–over–year on an adjusted basis, and profits were way higher than what analysts had forecasted.

SAP’s strongest competitive advantage is its recurring revenue business model. During fiscal 2020, more than two–thirds of the company’s revenue was recurring in nature, or what management calls predictable revenue. This ratio of predictable revenue has risen consistently in the last couple of years.

Recurring revenue allows the company to optimize customer retention rates and to use the resulting cash flows to aggressively invest in growth opportunities, such as its cloud business.

We expect total returns of 10.1% for SAP per year, consisting of 8% annual EPS growth, the 1.5% dividend yield and a small boost from an expanding P/E multiple.

Best Big Tech Dividend Stock #3: HP Inc. (HPQ)

Hewlett–Packard’s story goes back to 1935 with two men in a one–car garage making a huge impact on electronic test equipment, computing, data storage, networking, software and services that has lasted for more than eight decades.

On November 1st, 2015, Hewlett–Packard spun off Hewlett Packard Enterprise Company (HPE) – which was its enterprise technology infrastructure, software and services business – and changed its name to HP Inc. (HPQ).

Today HP Inc. has centered its business activities around two main segments: its product portfolio of printers, and its range of so–called personal systems, which includes computers and mobile devices.

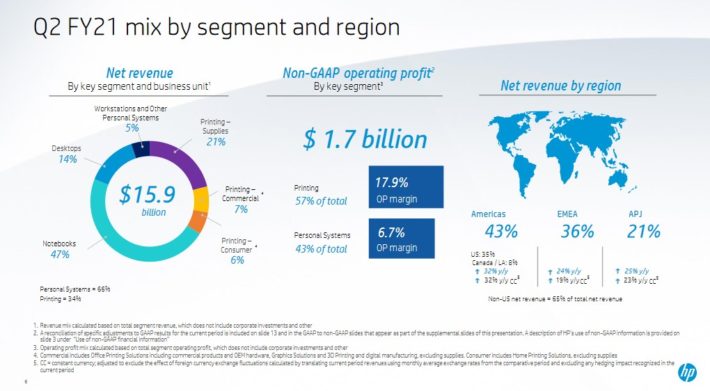

HP reported its second quarter (fiscal 2021) results on May 27. The company reported revenue of $15.9 billion for the quarter, which was up 27% from the previous year’s quarter.

Source: Investor Presentation

Non–GAAP earnings–per–share totaled $0.93 per share during the quarter, which beat the analyst consensus estimate easily. Earnings–per–share were up by a massive 82% versus the prior year’s quarter.

The company currently forecasts earnings–per–share in a range of $0.81 to $0.85 for the third quarter, which would result in another sizeable year–over–year growth versus the same quarter during fiscal 2020. HP’s consumer business has remained strong in recent quarters, and corporate customers are increasing their spending again.

HP enjoys competitive advantages as a leader in its two legacy businesses. The long–term viability of these markets is unknown to some extent, but for now HP owns a $3+ billion annual underlying profit machine. HP could be a major beneficiary of consolidation in the industry, and thanks to its strong balance sheet and ample cash flows, it could easily become an acquirer of competing businesses.

It is forecasted that earnings–per–share will hit a new record level this year, with management’s earnings–per–share guidance range being $3.40 to $3.50.

Based on the midpoint, shares currently trade for a 2021 P/E of 8.5. This is below our fair value P/E of 10. In addition to an expanding valuation multiple, shares currently yield 2.7% while we expect 4% annual EPS growth. Total returns are expected to reach 10.3% per year.

Best Big Tech Dividend Stock #2: Hewlett Packard Enterprises (HPE)

The Hewlett Packard Enterprise Company (commonly referred to as HPE) is a multinational enterprise information technology company based in San Jose, California. The company is a business–focused organization with two divisions: Enterprise Group, which works in servers, storage, networking, consulting and support, and Financial Services.

The newly created Enterprise firm focuses on new technologies in the digital infrastructure.

Source: Investor Presentation

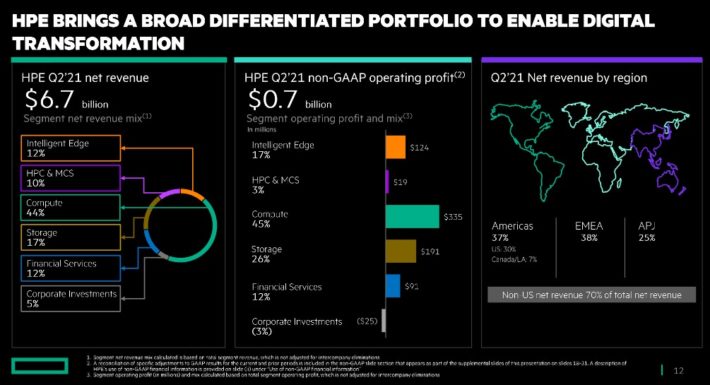

On June 1st, 2021, HPE reported its Q2–2021 results for the period ended April 30th, 2021. For the quarter, revenues rose by 11% to $6.83 billion, showing better than normal sequential seasonality driven by strong demand. HPE’s annualized revenue run–rate (ARR) reached $678 million, up 30% from the prior–year period.

The company’s “Compute” revenues of $3 billion were 12% higher year-over-year, while the “Storage” segment enjoyed 5% revenue growth to $1.1 billion. Consequently, non–GAAP EPS grew to $0.46, 70% higher YoY, due to compressed results in the comparable period last year as a result of the pandemic outbreak.

Management hiked its FY2021 outlook once again, pointing towards FY2021 non–GAAP diluted EPS in a range of $1.82 to $1.94 (previously $1.70–$1.88) and free cash flow of $1.2 to $1.5 billion (previously $1.1 to $1.4 billion).

The company’s net income had been under pressure over the past few years, but EPS remained relatively stable amid massive buybacks. Management has seen share buybacks as a more efficient way to return capital to shareholders.

Since 2015, HPE has repurchased around 29% of its stock. As the company grows in Intelligence Cloud’s ARRs, profitability and EPS growth should gradually rely less on its legacy segments and buybacks to grow.

With the latest quarter reaffirming the Cloud segment’s strong growth prospects while displaying promising results in its legacy segment, we are raising our EPS growth estimates to 6%. EPS growth should be powered by cost–cutting efficiencies, stock buybacks, and gross margins expanding.

HPE has a 2021 P/E of 8, slightly below our fair value estimate of 8.5. Future returns will be driven mostly by the 3% dividend yield and 6% expected EPS growth, for total returns of 10.4% per year over the next five years.

Best Big Tech Dividend Stock #1: Micro Focus International plc (MFGP)

Micro Focus International PLC is an enterprise software corporation that primarily services corporate customers within the Forbes Global 2000. The company’s products include IT infrastructure and enterprise applications.

Micro Focus International’s operating segments include Security, IT Operations Management, Application Delivery Management, Information Management & Governance, and Application Modernization & Connectivity.

Micro Focus International is headquartered in the U.K., but U.S. investors can initiate an ownership stake through American Depository Receipts.

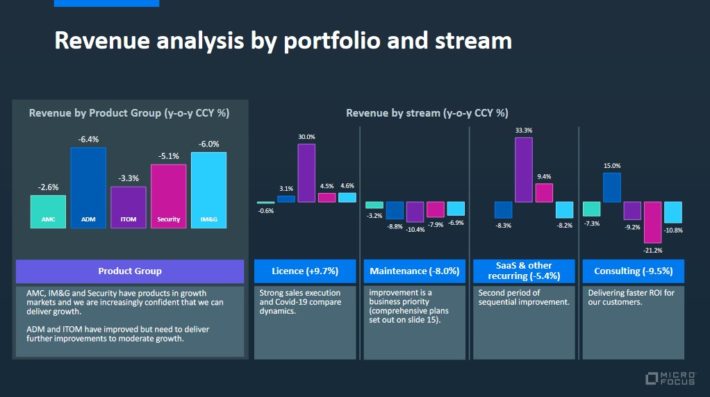

Micro Focus reported its interim results for the fiscal year 2021 (a period that ended April 30) on July 1. Adjusted earnings–per–share decreased 8.3% to $0.66. Revenue fell 4.6% to $1.4 billion, which continues a pattern of a deaccelerated decline from the second half of last fiscal year.

Source: Investor Presentation

The company still faced headwinds related to the COVID–19 pandemic, but did see some agreements closing quicker than anticipated in the quarter. Licensing revenues were up almost 10% for the first half, though this was offset by mid–single–digit to high single–digit declines in other areas.

Adjusted EBITDA declined 7.7% to $519 million while adjusted EBITDA margin was down 130 basis points to 37.7%. Both declines were less than what the company saw in fiscal year 2020. Adjusted free cash flow totaled $247 million.

Going forward, we believe that Micro Focus is more likely to generate a low–single–digit earnings–per–share growth rate, through marginal revenue growth and some margin upside.

Micro Focus International’s most compelling competitive advantage is the deep and technical relationships it has with its enterprise customers. Micro Focus’ management notes that 70% of the company’s revenue is recurring, which provides it with substantial business stability and recurring cash flows.

Shares trade for a P/E of 4.5, below our fair value estimate of 7. Expansion of the P/E ratio could boost annual returns by 9.2% per year. In addition, we expect 4% annual EPS growth, while the stock has a ~3% dividend yield.

Overall, total returns are expected to exceed 16% per year. This makes MFGP the most attractive dividend-paying tech stock with a market-beating yield and a satisfactory Dividend Risk score.

Final Thoughts

Tech stocks have not traditionally been associated with dividends, but there are plenty of quality dividend payers in tech sector to choose from.

The 10 tech stocks in this article all pay dividend yields above the current S&P 500 Index average. They also have strong Dividend Risk scores, and positive total expected returns for the next five years.

{kind=link}

{kind=link}

{kind=link}