Updated on March 14th, 2020 by Nate Parsh

Monthly dividend stocks are highly appealing to individuals such as retirees, because they make it significantly easier to budget dividend income against living expenses. We’ve compiled a list of all 58 monthly dividend stocks.

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yield and payout ratio) by clicking on the link below:

Superior Plus Corporation (SUUIF) is one such company whose management team has decided to pay a monthly dividend to shareholders. And, the company has an exceptionally high dividend yield.

As of today, Superior Plus yields 9.9% – more than four times the average dividend yield in the S&P 500. This makes Superior Plus one of our high-yield stocks, which we define as having a dividend yield above 5%. You can see the full list of all 5%+ yield stocks here.

Superior Plus’ high dividend yield and monthly dividend payments are two reasons why investors might take interest in this stock. However, the volatile nature of Superior’s business model and a poor track record of dividends are red flags.

This article will analyze Superior Plus’ investment prospects in detail to determine whether the company merits consideration for the portfolios of dividend growth investors.

Business Overview

Superior Plus is an energy company headquartered in Toronto, Canada. The company operates in two main segments:

- Energy Distribution

- Specialty Chemicals

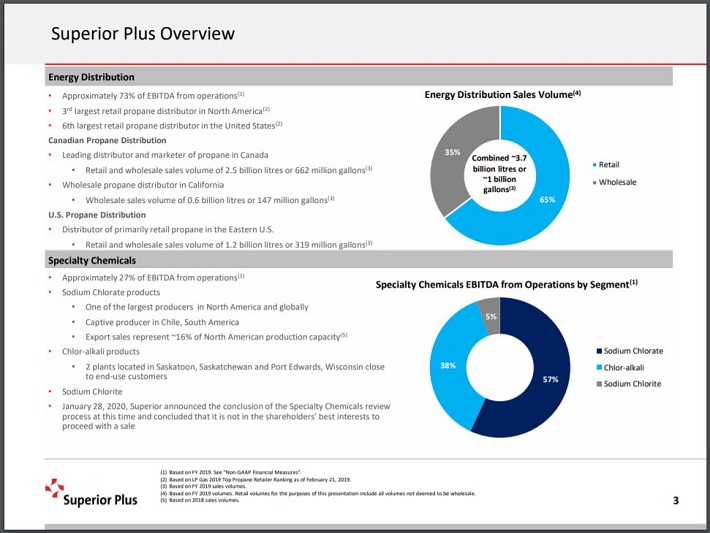

Details about each of Superior Plus’ operating segments can be seen below:

Source: JP Morgan High Yield Conference Presentation, slide 3

Superior Plus’ Energy Distribution segment is involved in the distribution and retail marketing of propane products, liquid fuels (including heating oil and propane gas), and wholesale liquids marketing services. This segment operates primarily in Canada but has been expanding into the United States through a series of acquisitions that began in 2009. The Energy Distribution segment is operated under the trade names ‘Superior Propane’ or ‘Superior Gas Liquids’.

Superior Plus’ Specialty Chemicals segment is focused on the production and supply of sodium chlorate and chlor-alkali products. Superior Plus is in the process of considering divesting its chemicals business, but the company hasn’t placed a timetable on doing so. ERCO Worldwide is the second largest producer of sodium chlorate in the world and serves customer segments such as pulp and paper, food, energy, and agriculture.

It should be noted that Superior Plus is an international stock – the company trades on the Toronto Stock Exchange under the ticker SPB and reports financials in Canadian dollars. Buying stocks based outside the U.S. presents a number of unique risks, such as currency risk.

Growth Prospects

Investors can get a sense of a company’s future growth potential by examining its historical growth rates. In the case of Superior Plus, the results are not reassuring.

From 1997 to 2017, Superior Plus saw revenues increase nearly 14% per year. However, from 2008 through 2018, revenue grew at a compound rate of less than 1%. Financial results have been drastically different in the most recent decade.

That said, when accounting for the low oil price environment of 2014 to 2016, Superior Plus appears to be performing much better. The company’s revenues grew nearly 18% from to 2016 to 2017. In 2018, revenues were higher by almost 14%.

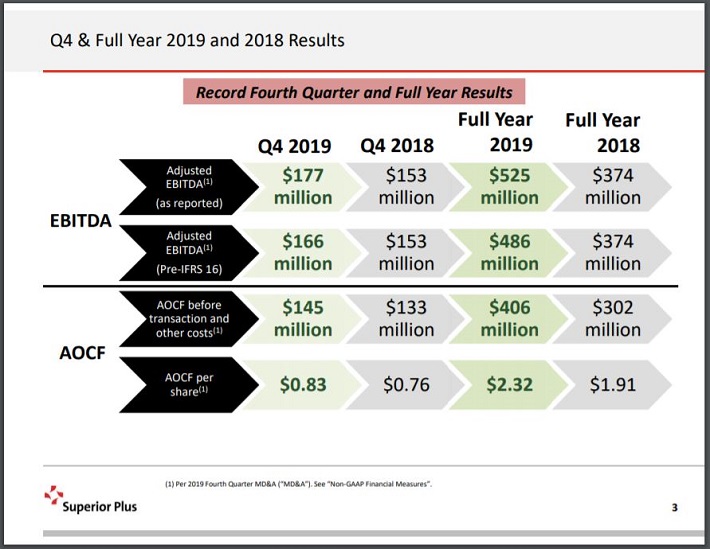

Source: Fourth Quarter Earnings Results, slide 3.

Looking at revenue growth in recent years portrays Superior Plus in a much better light. Revenue improved 4% in 2019. Still, this has not translated into a rising share price. The company’s share price has consistently held below $10, not much higher than where it was during the 2014-2016 oil downturn. Presumably, investors fear what the future holds with oil and gas prices plunging once again.

Moreover, the share price is near where it was during much of the 2007-2009 financial crisis – a consistent under-performance during one of the longest bull markets on record. There are two reasons why rising revenues have not translated to a rising share price. The first is because of the company’s weak spending controls.

Superior Plus has been unable to grow its net income at a pace anywhere close to its rate of revenue growth. This implies that the company’s expenses have been rising faster than revenues, which is a worrisome sign.

Capital expenditures were up 154% in 2017 before increasing 90% in 2018. While acquisitions declined significantly during 2019, efficiency, process improvement, growth-related and maintenance expenses grew 33%. This is partly due to the company’s capital-intensive business model (which generates significant depreciation and amortization charges).

The company’s inability to translate rising revenue to rising per-share net income is one reason it has failed to grow shareholder value over time. The second reason is that the company’s share count has meaningfully increased over time.

When a company issues shares, it is effectively performing the opposite of a share repurchase. Each continuing shareholder’s portion of the underlying business becomes less valuable. In this case, dilution has definitely harmed the company’s shareholders. Superior Plus has nearly doubled its share count since 2008. The share count grew nearly 11% alone in 2019.

Competitive Advantages & Recession Performance

As an operator in the energy distribution industry, Superior Plus has competitive advantages, benefiting from regulatory barriers to entry, and significant upfront capital outlays to enter the market. Unfortunately, Superior Plus has not shown the ability to endure through all economic environments. Earnings-per-share were cut in half during the last recession and a new high was not achieved until 2019.

A company showing such outsized earnings-per-share declines can be expected to also cut its dividend when it reports losses. Indeed, Superior Plus cut its dividend by 26% in March of 2011 and again by 50% in November of 2011.

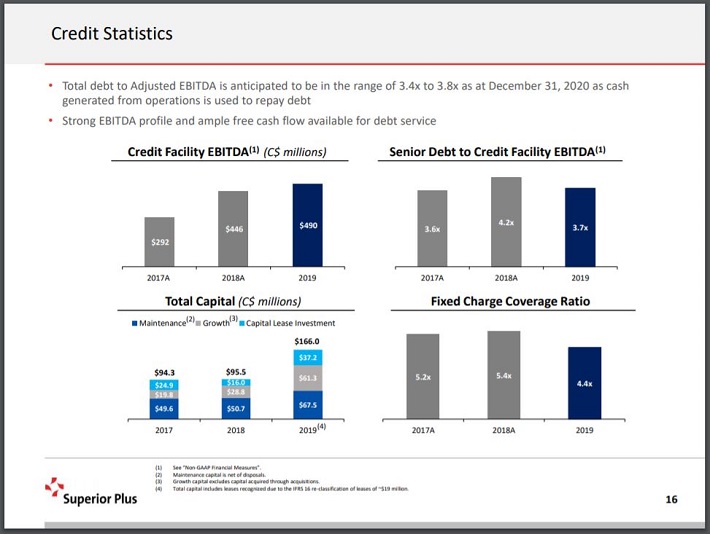

Superior Plus has responded by noticeably reducing its leverage. In fiscal 2012 (the first full year after the dividend cut), the company reported a leverage ratio (total debt to adjusted EBITDA) of 4.6x. The leverage ratio for 2019 declined to 3.7x from more than 4x in the previous year.

Source: JP Morgan High Yield Conference Presentation, slide 16

The company is in decent shape in terms of its debt load, with no material maturities until 2023. The company has a target leverage ratio of 3.4x to 3.8x.

Dividend Analysis

The dividend yield will likely make up most of the Superior Plus’ returns going forward given the lack of share price growth over the last decade. Superior Plus currently distributes a monthly dividend of $0.06 per share, or $0.72 per share annualized in Canadian dollars. At present exchange rates, this works out to approximately $0.52 per share in U.S. dollars.

The company has distributed the same dividend for a long period of time. U.S. investors need to keep in mind that the company pays its dividend in Canadian currency, which will have an impact on actual capital received. Based on an annualized dividend payout of $0.52 per share, Superior stock has a current dividend yield of 9.9%

Superior Plus is expected to earn $1.54 this year, giving the company a payout ratio of 35%. For now, the dividend appears to be safe due to the low payout ratio. That said, Superior Plus has not increased its dividend and is not expected to in the near future. The company also cut its dividend twice in 2011, which shows how quickly conditions can deteriorate given the volatility of Superior’s business model.

As such, we feel that Superior Plus is a risky stock for income investors to hold, particularly during a downturn in commodities or a global recession.

Final Thoughts

Superior Plus’ high dividend yield and monthly dividend payments help this stock to stand out relative to other dividend investments, particularly for income-oriented investors like retirees.

Some due diligence reveals that this particular security has an underwhelming track record. Moreover, its recent dividend cut suggests that another dividend cut could occur during the next recession.

Although its name suggests otherwise, we believe that Superior Plus is unlikely to deliver superior total returns moving forward. We recommend avoiding this stock and instead investing in companies with more tangible characteristics of business quality.

{kind=link}

{kind=link}

{kind=link}