Updated on February 25th, 2020 by Josh Arnold

In the stock market, reaching for high yields often backfires. To be sure, stocks with extremely high dividend yields look great on the surface. However, stocks with high yields are often the ones with the greatest level of risk in their distribution.

For example, Capitala Finance Corp. (CPTA) has a staggering 11% dividend yield. Capitala is one of hundreds of stocks with a 5%+ dividend yield.

Not only that, but Capitala (like many Business Development Companies, or BDCs) pays its dividend each month. This allows investors to compound their wealth even more quickly than a stock that pays a quarterly or semi-annual dividend.

There are fewer than 60 companies that pay monthly dividends. We’ve compiled a list of monthly dividend stocks with important financial metrics like dividend yields and P/E ratios that you can access below:

At first, such a high dividend yield looks like a no-brainer. After all, income levels from all kinds of assets have fallen in recent years, and Capitala sports an 11% yield today.

But looking closer, there are potential pitfalls when it comes to these extreme high-yielding stocks.

This article will discuss why Capitala’s dividend yield—while certainly very enticing—is better left for only the most risk-tolerant investors.

Business Overview

Capitala is a Business Development Company, or BDC. The company has $3.0 billion in assets under management and it uses that capital to provide lower and middle market businesses with debt or equity financing.

The company’s strategy focuses on investing in debt securities and minority equity co-investments, typically for companies with enterprise values lower than $250 million. Additional criteria used in evaluating investment opportunities include annual revenue of $10 to $200 million, and TTM EBITDA of $4.5 to $30 million.

The company has invested in over 150 different companies since its inception in 1998 and seeks to partner with strong management teams to create value and achieve optimal outcomes for shareholders.

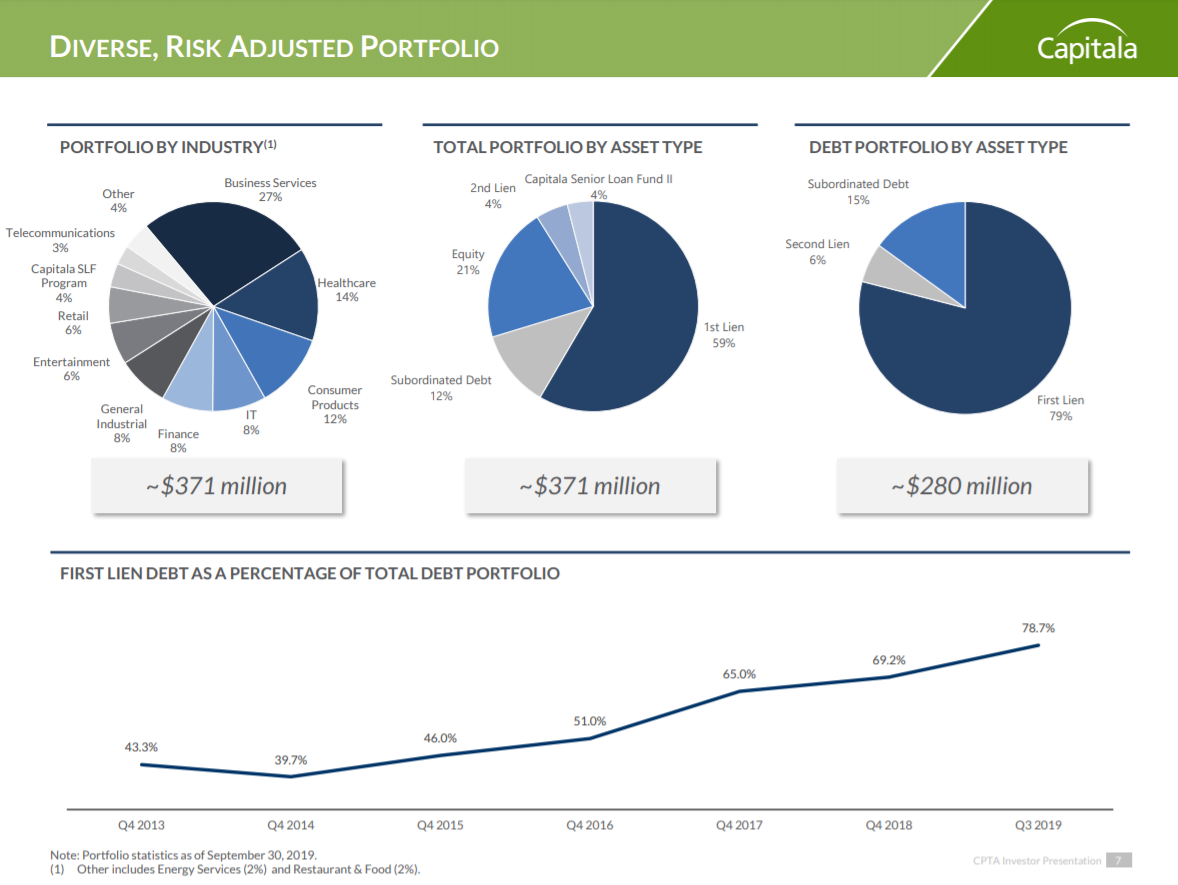

The investment portfolio is highly diversified, across many industry groups and asset classes. About 80% of the total investment portfolio is comprised of first-lien debt, as of the third quarter of 2019, a huge increase over the prior year period.

Source: Investor Presentation, page 7

Approximately 79% of the portfolio consists of debt investments, with the remaining 21% in equity investments, which hasn’t changed year-over-year.

The company’s most recent earnings showed another relatively weak performance. Total investment income during the quarter was $10.1 million, down from $11.5 million in the year-ago period. Interest and fee income was down $2.2 million, which was partially offset by a rise in dividend income totaling $1.1 million.

Total expenses fell from $7.7 million to $7.1 million year-over-year, but net investment income still declined from $0.24 per share to $0.18, a 25% year-over-year decline. This was also below the quarterly dividend rate of $0.25 per share.

Third-quarter weighted average yield on debt investments was 10.6%, while $33.2 million in repayments more than offset $13.9 million in new deployments. The company did say it expects the coming quarters to be supportive of net investment income growth following a few quarters of net repayments. Net asset value also declined from $11.88 to $9.40 from December 2018 to September 2019.

The company continues to pay its monthly distribution of $0.083, totaling an annualized distribution of $1.00. Capitala has never paid a return-of-capital distribution; all payouts come from investment income.

Growth Prospects

Capitala has two key catalysts for future investment income growth. The first is to invest more money, which will generate higher income.

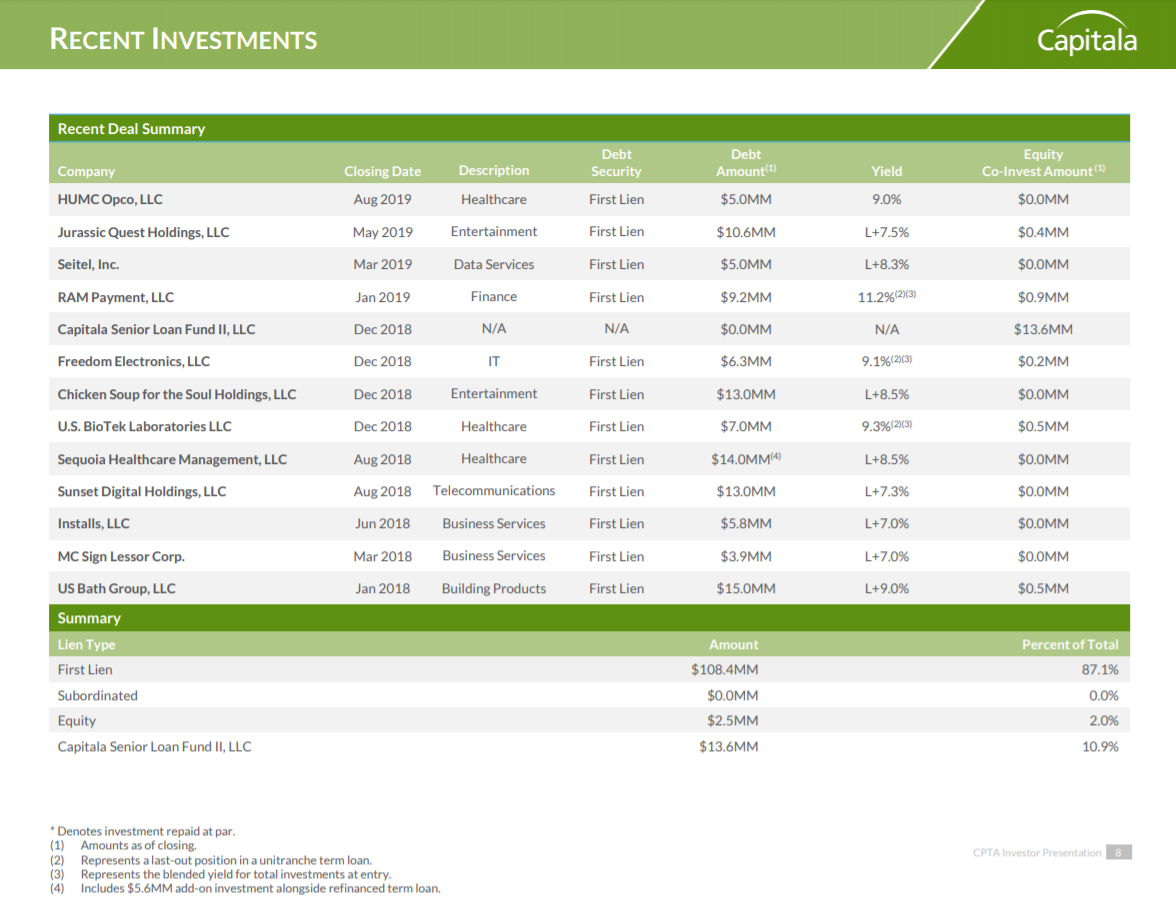

The company regularly puts new money to work and in the first three quarters of 2019, it invested $124.5 million, 87% of which was first lien debt.

Source: Investor Presentation, page 8

This is consistent with Capitala’s push to boost returns and reduce risk by investing in more senior debt, and is helping to boost its overall portfolio’s percentage of first lien debt. We expect Capitala will continue to raise and invest more capital, primarily in senior loan instruments, for many years to come. This is the primary way in which Capitala will grow in the coming years.

The second catalyst is to earn more on its existing investments, although the company already earns a very high portfolio yield. The company’s weighted average debt yield is 11.5% as of the end of Q3 2019, which is down from prior values in excess of 13%.

Still, this is a very high level of returns in a low-rate environment and Capitala has achieved this with a well-diversified base and with companies that have strong rates of cash flow.

The 111% payout ratio should be a concern for investors going forward. There is no wiggle room for the dividend, which calls into question the sustainability of Capitala’s hefty dividend payout if business conditions continue to deteriorate.

However, Capital has operated this way for years as its distribution is generally at or near 100% of its investment income. We see net investment income at $0.90 for 2019, meaning the dividend of $1.00 isn’t covered.

Dividend Analysis

Capitala has a current dividend monthly payout of $0.083 per share. On an annualized basis, the dividend payout is $1.00 per share. Based on its current stock price, Capitala has a dividend yield of 11.2%. The dividend was covered with net investment income in 2018, but the dividend fell below NII-per-share in the third quarter, and we do not expect the dividend to be fully covered by NII-per-share for 2019.

As mentioned, coverage of the dividend has been very tight for years at this point, and it has resulted in several distribution cuts since the IPO. If net investment income declines from current levels, the dividend will be at risk. With the payout ratio being in excess of 100%, Capitala’s dividend is at high risk of being cut.

Capitala has only $19 million of debt maturities in 2020. This provides the company a meaningful respite from the cash crunch that would befall it with large debt maturities. However, the long-term is less certain. Maturities will spike to $187 million in 2021. This will be a challenge, as this represents several years of net investment income.

As a result, Capitala may not be a good stock for investors interested in long-term dividend growth. To be fair, Capitala has a flexible capital structure and has refinanced its way out of large maturities before. Still, it is certainly something for investors to keep an eye on. This is particularly true because of the lack of coverage of the dividend in recent quarters.

Final Thoughts

Stocks with 10%+ dividend yields look great on paper. But with such high yields often comes high risks. With a payout ratio likely to exceed 100% of NII-per-share for 2019, Capitala has essentially no margin for error.

Investors looking for steady, more reliable income would be wise to steer clear of high-yield BDCs. Instead, keep focus on the tried-and-true dividend stocks, such as the Dividend Aristocrats. You won’t find any Dividend Aristocrats with 10% yields, but in return, the Dividend Aristocrats offer sustainable payouts and long track records of annual dividend increases.

Capitala has a much shorter dividend history, and a very high payout ratio. It may be able to sustain its dividend going forward, but the level of risk may not be appropriate for all investors. We think Capitala will struggle to produce enough net investment income in the coming years to cover its payout fully, and thus, we see the stock as too risky for income investors.

{kind=link}

{kind=link}

{kind=link}