Growth Prospects

Broadmark has managed to grow its loan portfolio in the past couple of years, driving interest income and fee generation higher. Since the trust has no funding costs, its lending margins are exceptional. That means that when Broadmark grows its lending portfolio, the additional operating income that is derived from the revenue gains is significant.

We see this trait continuing as the trust had more than $250 million of cash on its balance sheet at the end of the first quarter, so it has plenty of capital to continue to boost its lending activity. On the other hand, Broadmark is seeing significant weakness from its lending portfolio thanks to impacts from COVID-19. As of the end of the first quarter, a staggering 14.2% of its portfolio was in default.

The trust’s focus on construction loans means that it is dependent upon its customers completing their projects on time, and subsequently paying Broadmark for the loan. With construction activity slowing or stopping altogether in many parts of the country, Broadmark’s portfolio is suffering.

Broadmark has several ways to resolve defaults, including loan modification to taking possession of the property, but this is a costly activity for the trust to undertake, and will crimp FFO generation.

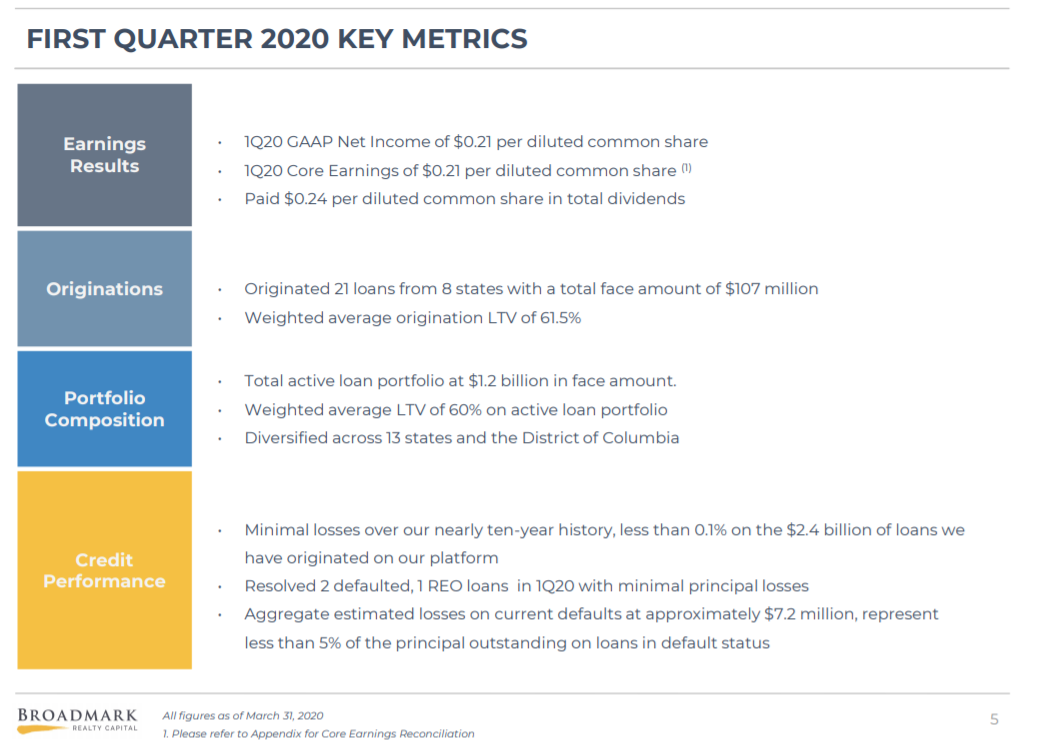

Source: Investor presentation, page 5

First quarter core earnings came to $0.21 per share, which compares somewhat unfavorably to the $0.24 per share the trust paid in dividends. Broadmark originated 21 new loans in a total of eight states in Q1, with a face value of $107 million, so it continues to boost its portfolio aggressively. The originations had a weighted average LTV of 61.5%, slightly higher than the rest of the portfolio, but still quite strong from Broadmark’s perspective.

Broadmark maintains a positive growth outlook, given its pristine balance sheet. Indeed, it has essentially no limitations on how much it can continue to grow its lending portfolio, particularly if it decides to take on debt to expand the portfolio.

However, we are still wary of its reliance upon two relatively narrow geographical areas, as well as its reliance upon residential construction loans. We believe Broadmark can grow FFO in the mid-single-digits in the coming years, but caution investors that a high number of defaults were present at the end of Q1, and that there is very little history on Broadmark since it has been public for less than a year. This means risks are somewhat higher for Broadmark than some other REITs.

Dividend Analysis

Broadmark’s dividend payment stood at $0.12 per share in December 2019. However, the dividend for January was reduced to $0.08 per share. The April, May, and June distributions were in the amount of $0.06 per share. This demonstrates a concerning trend of multiple dividend reductions in the recent past.

Still, at an annualized payout of $0.72 per share, Broadmark stock has a current yield of 7.6%, which is nearly four times that of the broader market, as measured by the S&P 500. With a high dividend yield, along with monthly payments, Broadmark stock is attractive from an income perspective.

We expect Broadmark to produce between $0.75 and $0.80 in FFO-per-share this year, or “core earnings” as the trust referred to it as in the Q1 release, which means that its dividend coverage is relatively poor. We expect Broadmark to pay out essentially all of its FFO this year, which means that if the downturn in the lending market worsens, the distribution may be at risk of yet another cut.

Broadmark can likely afford the current payout of $0.72 annually due to the high level of cash on its balance sheet, which it can use to fund any deficits between FFO and declared dividends. Of course, this is not sustainable over the long-term. The decline in the share price over the past several weeks is likely an indication that even the current monthly payout of $0.06 per share may not be safe.

This also means that the prospect of dividend growth isn’t particularly strong with Broadmark, as we see the weakness in the trust’s portfolio that was evident in Q1 as being a longer-term problem. Broadmark’s narrow focus means very little diversification. Sustainable dividend growth will likely be an issue for a long time to come.

Final Thoughts

While Broadmark’s high dividend yield and monthly payment schedule are appealing, investors should be cautious. The extreme level of defaults seen in Q1 likely hasn’t abated yet given the high concentration in terms of geographic and loan type. The dividend payout is at risk due to this.

In addition, the trust is trading at 118% of end of Q1 tangible book value, so the stock is slightly overvalued as well. Given these factors, we do not see Broadmark as a safe dividend stock, and would recommend investors pass on it until the prospects for its portfolio improve.

With wide-scale shutdowns across the country due to COVID-19, the construction loans made by Broadmark are at greater risk than those financed by cash flows. Broadmark’s inherent risk is much higher than other REITs.

{kind=link}

{kind=link}

{kind=link}