Meta Platforms Earnings: Watch These Key Metrics

It’s an action-packed week concerning earnings, with the reporting docket dominated by several Mag 7 members.

Among the bunch is beloved Meta Platforms META, whose shares have outperformed nicely in 2025, gaining 26% compared to the S&P 500’s 18% gain. The stock also sports a favorable Zacks Rank #2 (Buy), with near-term EPS expectations remaining bullish.

Image Source: Zacks Investment Research

But what should investors be watching for? Let’s take a closer look at key metrics and expectations.

Ad Revenue Remains Key

Advertising results are generally the major metric investors watch heavily, accounting for the bulk of the tech titan’s revenue. AI implementations have enabled the company to deliver more relevant ads to consumers, boosting performance significantly over recent periods. Ad impressions grew 11% year-over-year throughout its latest quarter.

We expect Meta Platforms to post $48.5 billion in ad revenue, reflecting a sizable +21% jump year-over-year. The company has regularly blown away our consensus expectations on the metric, with the beats growing in size.

Below is a chart illustrating META’s ad results relative to our consensus expectations, expressed as a percentage.

Image Source: Zacks Investment Research

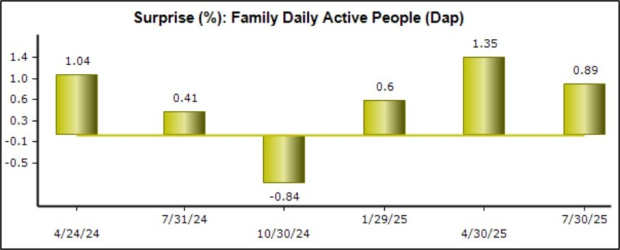

In the same vein, its family daily active people (DAP), which represents all of the users across its family of apps (Instagram, WhatsApp, Facebook, etc), will also be key in telling us if its overall user base is growing or shrinking.

As revealed in its latest results, DAP averaged 3.48 billion in June 2025, an increase of 6% year-over-year. The company’s user base growth has continued to be outstanding, providing many clear benefits.

Our consensus estimate for DAP for the upcoming period stands at 3.49 billion, representing a 6.1% increase from the 3.29 billion mark in the same period last year. The growth rate is largely in line with other recent periods, not raising any red flags.

Image Source: Zacks Investment Research

The valuation picture is also fair heading into the print, with the current 24.9X forward 12-month earnings multiple reflecting a modest 5% premium relative to the S&P 500. The company is forecasted to see 18% EPS growth on 19% higher sales in its current fiscal year.

Image Source: Zacks Investment Research

Bottom Line

Beloved Meta Platforms META is on the docket this week, reflecting one of the several Mag 7 reports we’ll receive this week.

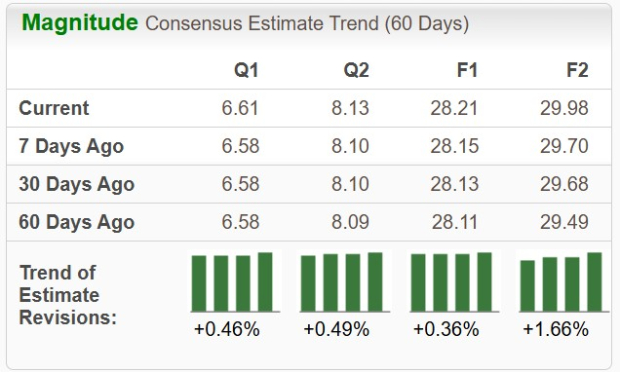

Quarterly sales and EPS expectations are largely unchanged from where they stood at the beginning of August, with the titan expected to see 10% adjusted EPS growth on 22% higher sales. Below is a chart illustrating the EPS revisions.

Image Source: Zacks Investment Research

Advertising results will again be the key focus, having shown great momentum over recent periods thanks to AI implementations that are providing more relevant results to users.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power, you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Meta Platforms, Inc. (META): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Source Zacks-com

{kind=link}

{kind=link}

{kind=link}