Published on November 15th, 2019

This is a guest post from Mike Errecart at Old School Value

Dividend investing and value investing have long gone hand-in-hand.

Value investors often look to the dividends paid by their stocks to help formulate the intrinsic value of a company, as a sign of a company’s quality and long-term viability, and as a source of safety in dividends’ positive contributions to total returns.

Ben Graham, the father of value investing, listed “Continued dividends for at least the past 20 years” as the 3rd criterion in his list of 7 statistical requirements for inclusion in a defensive investor’s portfolio from The Intelligent Investor.

Many income investors probably start by looking at dividends, then assessing the quality of the company and upside potential. Sometimes the “upside potential” is based on valuation metrics, but sometimes it’s based on strategy, growth, technical analysis, or other catalysts.

Most people in the deep value community start with valuation and will check out dividend information if there is any.

But what if we modified that, and tried to find deeply undervalued dividend stocks?

Defining Graham Net-Nets

Probably the most famous type of deep value stock is a Ben Graham “net-net,” where the stock is priced at less than some version of the company’s current assets. Warren Buffett called this “cigar butt” investing.

There are two main ways to find Net-Nets.

Net Current Asset Value (NCAV)

NCAV is just working capital (current assets minus current liabilities) divided by shares outstanding. Graham targeted companies trading at ⅔ NCAV.

Net-Net Working Capital (NNWC)

This is a close cousin to NCAV, but it really represents a fire sale liquidation value of tangible assets. The formula for this is:

NNWC = Cash and short-term investments

+ (0.75 x Accounts Receivable)

+ (0.5 x Total Inventory )

– Total Liabilities

Although true liquidations are rare, it’s more meant to represent a super conservative valuation.

So, are there any decent dividend payers that are trading at these levels? Let’s take a look.

Screening for U.S. Dividend Net-Nets

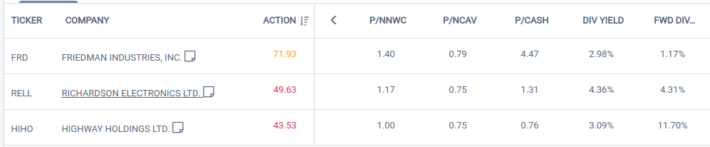

In my company’s fundamental stock analysis platform, we make it easy to screen for this kind of thing. When we put in the Price to NCAV and NNWC filters, along with dividend yield, not surprisingly, we don’t find too many. Companies in this much distress often can’t afford dividends. But, three names showed up:

Each of these is trading below P/NCAV, and just at or above P/NNWC. One is even trading below the amount of cash on its balance sheet. It’s amazing to me that any of them can afford to pay a dividend.

I’ve never heard of any of these companies, of course. They’re all below $100M in market cap.

Investing in Net-Nets means looking at really off-the-radar names. It also means you have to do a ton of research, because when companies become valued at such low levels, you have to worry about Value Traps — companies whose businesses are so bad they will never recover.

We’ve written several pieces on identifying value traps, but here are a few things you’d want to look at:

- Only FRD has positive earnings, with a payout ratio of 76% — definitely on the high side for sustainability. It also has positive Free Cash Flow. The others are likely to have funding issues.

- Insider ownership is very low for FRD and RELL at less than 1%. The managers may not have enough skin in the game. HHO, on the other hand, has such high insider ownership that transparency is a potential concern.

- All 3 companies appear solvent. No debt, with solid current and quick ratios.

There’s obviously a lot more to look at to understand each company’s financials and competitive position. I’ll leave that as an exercise for the reader, as this article is intended to explore new ways of finding interesting ideas rather than to asses the ideas themselves.

Best Valuation Ratios Research

Buffett modified Graham’s approach from finding any company — even terrible ones — priced at a huge discount to its intrinsic value to finding good companies at attractive prices. We don’t have to look through the closeout bins to find good value opportunities.

A recent paper from O’Shaughnessy Asset Management entitled “The Earnings Mirage” did some really interesting research on the effect of inflation on book values and earnings.

That article is well worth a read, and it has informed a lot of my recent thinking. Some of the insights from the article include:

- Inflation distorts both book values and earnings.

- Book values of assets should be inflation-adjusted. Because they’re not, depreciation becomes understated in current price terms. Understated depreciation results in overstated earnings.

- This makes using Free Cash Flow — which incorporates these depreciation-related expenses by subtracting CapEx — a key measure to use in your investing process.

The author looked at 8 different value metrics and back-tested portfolios constructed by ranking stocks on each of them.

- EV/FCF

- P/FCF

- P/OCF

- EV/EBITDA

- P/E

- P/EBITDA

- P/S

- P/B

Not surprisingly, when back-tested, the Free Cash Flow measures (P/FCF and EV/FCF) were the best individual valuation metrics with average excess returns around 5%. The income-based measures that ignore depreciation and CapEx (i.e., EV/EBITDA, P/OCF, P/EBITDA) performed less well and naturally inclined to overweight CapEx-heavy industries like materials and energy. You don’t want your Value factor exposure to really be a bet on certain sectors!

Interestingly, using a composite of all valuation metrics outperformed any single metric.

Undervalued Dividend Payers

Implementing OSAM’s specific methodology is a little bit of a pain, so for simplicity’s sake, we’re going to screen for companies at the lower end of most of these metrics with a primary sort on P/FCF.

We’ll also screen for:

- Dividend yield > 2.5%

- Payout ratio < 85%

- 5 year dividends per share growth > 0

- ROIC > 5%

I’m choosing to screen for ROIC > 5% because ROIC is a great measure of quality, but it’s also a highly mean-reverting metric, so a screen on a high TTM ROIC filters out too much. You can make the case, in fact, that finding companies whose ROICs are depressed and appear likely to revert back to the historical mean is an opportunity an and of itself. (But you would need to then check that the company’s mean ROIC is in fact above its cost of capital.)

When you do this, you end up with some interesting names:

Some financials, some beat-down retailers, some media.

Again, I’m not going to proceed with the deep-dives into any of these, but some of these are definitely worth looking at. If you want a tool to help calculate the intrinsic value of any of these companies with just a few clicks, come give Old School Value a try.

Conclusion

It’s clear that there are some attractively-priced dividend payers available, even in today’s relatively expensive market.

When you can combine strong returns from a solid dividend yield plus the upside potential of a valuation reversion, you have a recipe for strong risk-adjusted returns.

{kind=link}

{kind=link}

{kind=link}