Published on March 23rd, 2022, by Quinn Mohammed

Verizon pays a safe and reliable dividend. Even more, that dividend yields 5.0%, and has increased for the last seventeen years. The company benefits from recession-resistant qualities and competitive advantages that we believe will allow them to continue raising the dividend for years to come.

Not all high-yielding businesses are as safe as we believe Verizon to be, so deep analysis should be completed to verify the safety of high-yield stocks.

We have created a spreadsheet of high dividend stocks with dividend yields of 5% or more…

You can download your free full list of all securities with 5%+ yields (along with important financial metrics such as dividend yield and payout ratio) by clicking on the link below:

In this article, we will analyze the telecom giant Verizon Communications (VZ).

Business Overview

Verizon is a leading provider of technology and communications services. The company as we know it today was formed as the result of a merger between Bell Atlantic Corp and GTE Corp in June 2000. The company reports in two segments: Verizon Consumer Group and Verizon Business Group.

In September 2021, the company sold what once was their third segment, Verizon Media Group. The company deemed Verizon Media to be a non-core asset.

The company’s wireless business makes up about three quarters of total revenues, with broadband accounting for nearly one fourth of sales. And, Verizon is a mega-cap stock, as it has a market capitalization above $200 billion.

Verizon reported Q4 and FY 2021 results on January 25th, 2022. For the quarter, revenue grew 4.8% to $34.1 billion, beating estimates by $120 million. Adjusted earnings-per-share of $1.31 was an 8% increase compared to $1.21 in the prior year. For the year, revenue grew 4.1% to $133.6 billion while adjusted earnings-per-share was 10% higher to $5.39.

The company achieved wireless retail postpaid net adds was 1.058 million. About 53% of these were postpaid phone net adds. Total retail connections were nearly 143 million.

Revenue for the consumer segment grew 7.4% for the quarter, driven by higher rates of 5G-phone adoption and 55K Fios net additions. Average revenue per account (ARPA) also increased companywide. Business revenue was down 3% to $7.8 billion as gains in business wireless services were offset by weakness in the public sector. This segment had 391K wireless retail postpaid net additions, including 222K phone net additions.

Leadership provided a 2022 outlook. The company expects adjusted earnings-per-share of $5.40 to $5.55 for the year. Wireless revenue is projected to grow 9% to 10%, with organic service revenue of close to 3%.

Growth Prospects

While telecommunications’ utility-like services are often trailed by slow growth, Verizon breaks the mold with an earnings-per-share growth rate of nearly 10% per year for the last decade.

However, going forward, Verizon itself anticipates much slower revenue growth, at about 4.0% per year into 2025.

Source: Investor Presentation

The company expects for 5G Mobility to fuel the bulk of growth from 2022 to 2025. In fact, about half of the company’s growth is anticipated to come from 5G. Verizon anticipates 2.0% growth in annual revenue per account (ARPA) through 2025. Additionally, 5G adoption in the Business segment is set to grow to 80% by end of year 2025.

Another strong growth driver will be the company’s nationwide broadband growth. The company’s expanded footprint will cover 50 million households and 14 million businesses by year-end 2025. Fios also expects to reach 8 million internet subscribers by year-end 2025.

The MEC & B2B Solution business will continue growing Internet of Things (IoT) revenue as it anticipates annualized double-digit connections growth through 2025.

And lastly, Value Market, and Network Monetization will make up the rest of the company’s expected growth in the years ahead.

Source: Investor Presentation

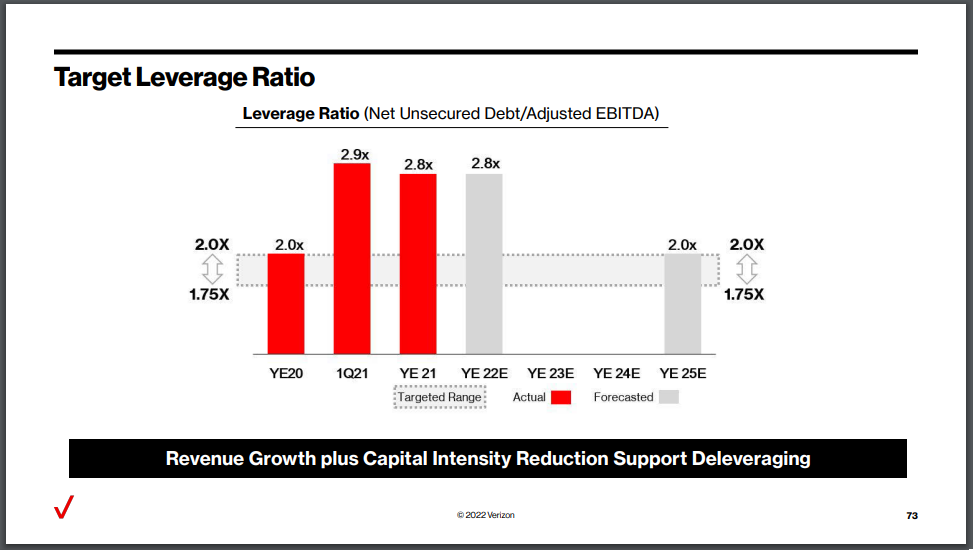

Once the company has deleveraged to 2.25 times net unsecured debt to adjusted EBITDA, they will consider share repurchases, which could also produce a minor tailwind to earnings. The company had a leverage ratio of 2.8x at year-end 2021 and expects to reach 2.0x by the end of 2025.

Competitive Advantages & Recession Performance

A key competitive advantage of Verizon is that it can often be considered the best wireless carrier in the U.S. This is clear when looking at the company’s wireless net additions and very low churn rate. The reliability of their service has led to a satisfied and intact customer base. This same customer base may then move to higher-priced plans.

The company also operates a business with recession-resistant qualities. Verizon customers are very likely to keep their wireless and broadband service, even during recessions.

Additionally, the divestiture of its non-core assets in Verizon Media will allow it to focus on maintaining its advantage in wireless service. And the massive infrastructure behind Verizon’s business would be difficult to replicate today, meaning the company has somewhat of a wide moat.

Dividend Analysis

Verizon is expected to pay a dividend worth $2.56 for 2022. The company last increased its dividend 2.0% and has a seventeen-year dividend increase streak. At the current share price, Verizon is yielding 5.0%. The current yield is about 50 basis points higher than the trailing decade average of 4.5%.

According to Verizon’s 2022 outlook, we anticipate the company will earn $5.48 in adjusted EPS for the year. Therefore, the company is forecasted to pay out 47% of adjusted EPS out in dividends. This is a healthy payout ratio for a telecom company. The security of the payout ratio and the solid expected growth rate of the company should lead to more dividend increases down the line.

In the last decade, Verizon has grown its dividend by 2.4% per year on average. Given a forecasted earnings growth rate of 4.0%, the payout ratio will moderate in the future as earnings growth outpaces dividend growth.

Final Thoughts

In the last year, Verizon divested its non-core media segment as it aims to focus on its core competencies of telecommunications. The company has executed solidly in the last decade, and should continue to do so going forward, albeit at a slower rate.

Verizon has increased its dividend for seventeen consecutive years. Not to mention, the payout ratio as a percent of adjusted earnings is less than 50%. Given the company is still growing, the dividend is secure, and we expect it to continue growing.

The company’s 5.0% yield is attractive for income investors. Value investors may also like the company here as we believe it’s trading below fair value.

{kind=link}

{kind=link}

{kind=link}