Published on March 27, 2022, by Felix Martinez

Durning the COVID-19 pandemic, many businesses, and industries were hit hard because of closures. One industry that was hit the hardest was the restaurant industry. Since everything is now open, there are companies in the restaurant industry that have been lagging in the stock market.

Cracker Barrel Old Country Store Inc. (CBRL) is one of those businesses. This company sports a high dividend yield with the potential of future dividend increases.

We also cover a lot of other different high-yield stocks in our database.

We have created a spreadsheet of stocks (and closely related REITs and MLPs, etc.) with dividend yields of 5% or more…

You can download your free full list of all securities with 5%+ yields (along with important financial metrics such as dividend yield and payout ratio) by clicking on the link below:

Thus, for the following high-yield stocks in this series, we will review Cracker Barrel Old Country Store Inc. (CBRL), with a dividend yield of 4.3%.

Business Overview

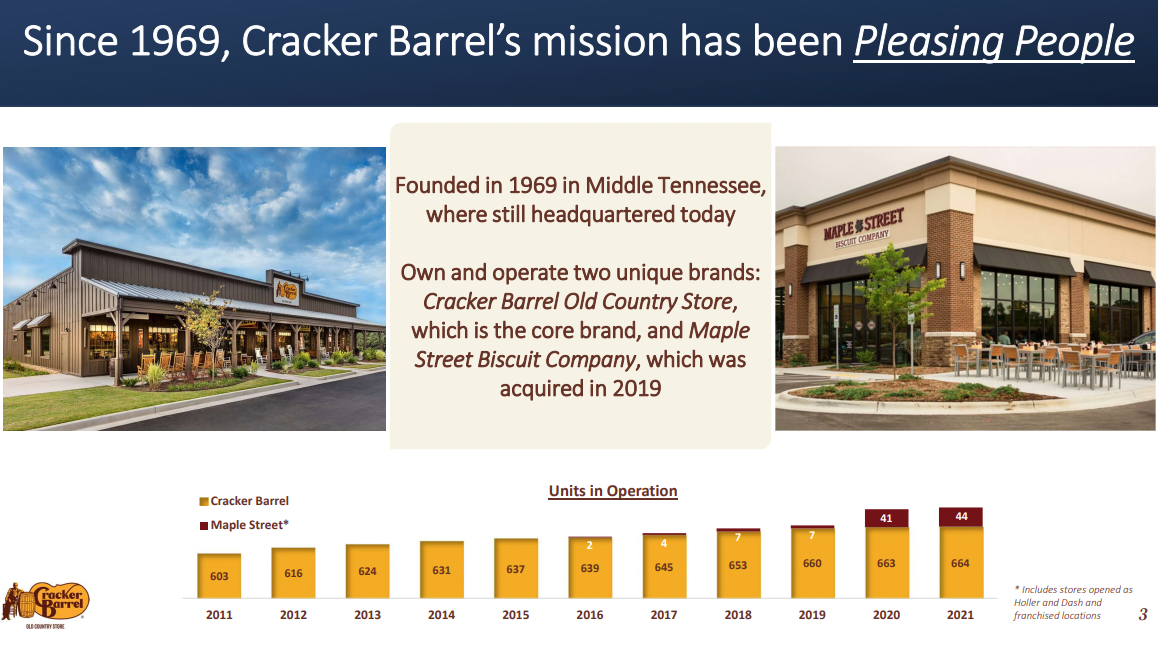

Cracker Barrel Old Country Store was established in 1969 as a restaurant concept that embraces America’s heritage. It sells home-style food at modest prices. It differentiates itself from competitors within the casual dining industry with unique menu offerings. For example, some of Cracker Barrel’s most popular menu items are its meatloaf and signature biscuits.

It also operates a gift shop. Cracker Barrel generates annual sales of approximately $3.3 billion and the stock trades with a market capitalization of $2.74 billion. The bulk of company sales comes from its restaurant operations, while the company also derives revenue from its in-store retail business.

The company owns and operates two unique brands. The primary and core brand is Cracker Barrel Old Country Store. The other Brand is Maple Stree Biscuit Company, which was acquired in 2019. The company has 664 stores that welcome approximately 225 million guests in a typical year with travelers making up about 35%-40% of those visits. Restaurant sales contribute 80% of revenue, while the retail shop, which is integral to the Cracker Barrel brand, makes up 20% of revenue.

Source: Investor Presentation

On February 22, 2022, the company reported second-quarter and first six months results for Fiscal Year (FY)2022. The company fiscal year ends at the end of July of each year. For the second quarter, the company’s total revenue increased by 6.2% compared to 2Q2019, which was pre-COVID-19. Total revenue increased 27% from $677 million in 2Q2021 to $862 million. Comparable store restaurant sales increased by 1.9% compared to pre-COVID-19 levels, and similar store retail sales increased by 13.7%. Also, the company added seven additional Cracker Barrel and 31 Maple Street net units.

GAAP operating income for the second quarter was $46.7 million, or a 224% increase compared to prior-year quarter GAAP operating income of $14.4 million. Net income for the quarter was $37.6 million, which increased 169% compared to 2Q2021. The company earned $1.60 per share on an earning per share basis. This saw a significant increase of 171% compared to the $0.59 per share the company made in 2Q2021.

For the six months, revenue is up over 24%, but operating income is down 64%. Operating expenses have seen notable increases for the six months thus far. For example, costs of goods sold increase by 24%. Labor expenses also increased by 23%. Because of the higher costs, this affected the company’s net income for the six months so far. The reported net income for the six months of the fiscal year was $71 million. This compares unfavorably to the first six months of FY2021, where the company reported a net income of $184.6 million. Overall, net income was down 62% compared to the last fiscal year’s first six months.

Overall, the company reported EPS was $3.02 compared to $7.77 in FY2021. This represents a decrease of 61%.

Growth Prospects

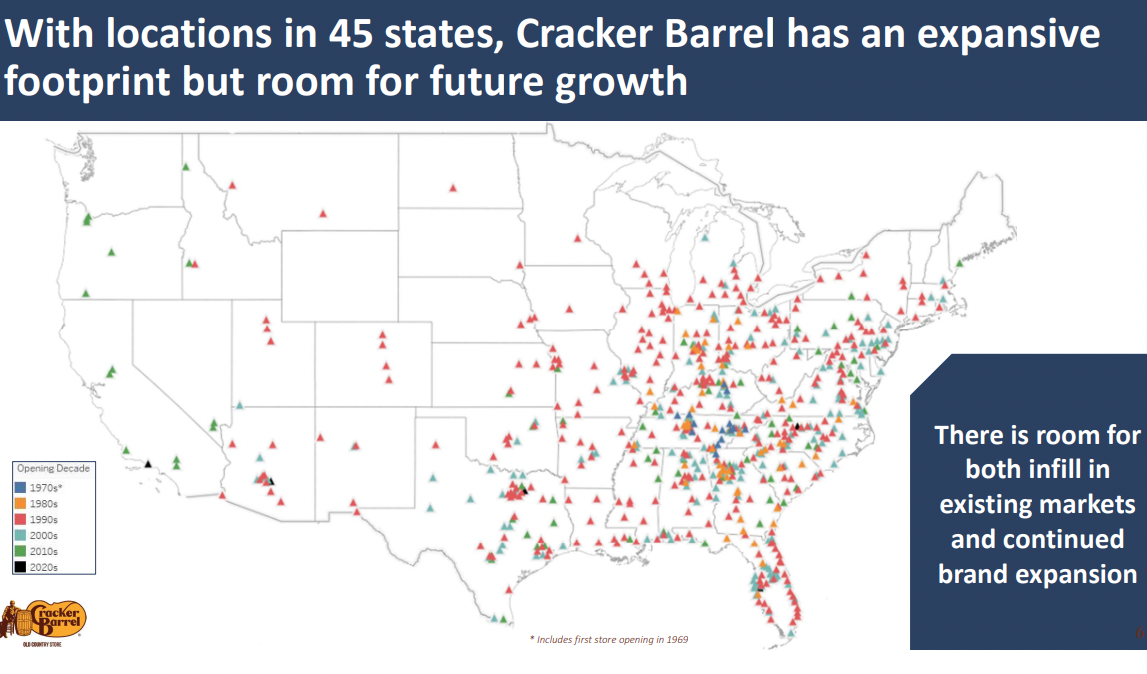

The company is currently in 45 states with the most footprint on the mid to east coast. This leaves the company with plenty of growth prospects to expand west. For example, the company expects the opening of 2 new Cracker Barrel locations and between 9 and 11 new Maple Street Biscuit Company locations and the one Maple Street Biscuit Company location that opened in the second quarter. The company can also grow traffic with a frequency strategy of earning one more visit from current guests per year as well as, attract new customers via new occasions and revenue sources.

Source: Investor Presentation

Another growth driver would be making the restaurants more appealing to the Gen z and Millennials without losing their core uniqueness. For example, Gen z and Millennials make up 11% and 21% of the company’s core guests, respectively. The Boomers and Matures make up 49% of the company’s core guests. This is concerning to investors as this age group gets older and older. This has the potential to hurt the company in the long run.

Acquiring others like restaurants would also help the company continue to grow. For example, the acquisition of Maple Street in 2019 complements the Cracker Barrel brand.

Competitive Advantages & Recession Performance

Cracker Barrel competitive is the authentic experiential brand. The company has a unique culture of caring hospitality, which people of all ages love when they visit one of its restaurants. The company earnings performed very well during the Great Recession. However, the share price performance was very poor during this time. For example, in 2007, the share price was as high as $50.37 per share and as low as $11.64 per share in 2008. This was about a 56% decrease in share price in a little over a year and a half.

CRBL’s earnings-per-share throughout the Great Recession:

- 2007 earnings-per-share of $2.52

- 2008 earnings-per-share of $2.79 (11% increase)

- 2009 earnings-per-share of $2.89 (4% increase)

- 2010 earnings-per-share of $3.62(25% increase)

As you see, the company did very well during the 2008-2009 Great Recession. Almost like the recession was not even there. But as we mentioned above, the share price performance miserably at the time.

On the bright side, those investors who held through the Great Recession did very well and were paid a growing dividend while waiting for a recovery.

Dividend Analysis

Before the COVID-19 pandemic, the company has a strong dividend growth history of nine consecutive years of dividend growth. The company had a nine-year dividend growth rate of 22.7%, which is outstanding. However, because of the COVID-19 pandemic, the company had to freeze its dividend. On May 25, 2021, CBRL announced a 23.1% dividend cut compared to its prior dividend.

The following quarter, the company increased its dividend by 30% and back to the levels before the COIVD-19 pandemic. This is very promising. This shows that the management team believes that the company will make it through this and continue its growth as before.

The dividend looks very safe going forward. We expect the company will make $7.08 per share in earnings in FY2022. This will give us a dividend payout ratio of 73.4%. We also expect the company to continue to grow earnings by 9.2% for the next five years. Thus, in 2027, we anticipate that Cracker Barrel will make $11.00 per share, bringing down the dividend payout ratio to a much better and safer level of 55%.

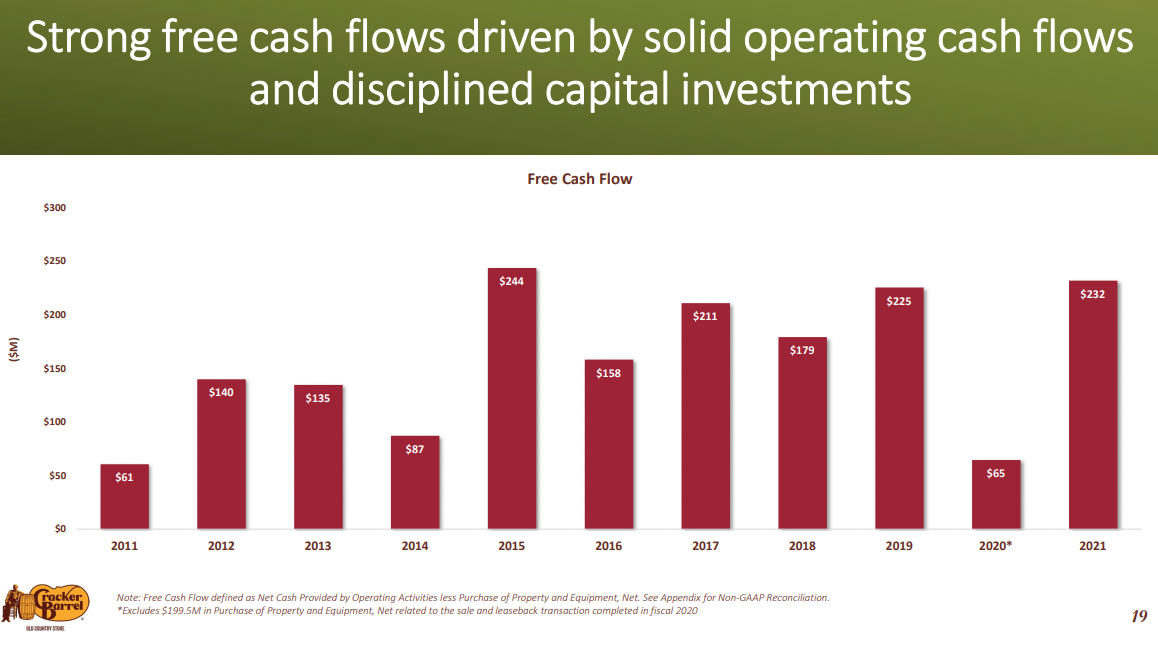

Another confidence boost to the dividend safety is that the company has seen strong free cash flow growth following the COVID-19 pandemic.

Source: Investor Presentation

The company also has an outstanding balance sheet. The company has an interest coverage ratio of 5.2, which is very good. As well as a 1.8 debt-to-equity ratio. Thus, the balance sheet is satisfactory to very good.

Thus, we think the dividend is very safe.

Final Thoughts

Cracker Barrel is well on its way towards recovering fully from the COVID-19 outbreak and related impacts. The recent full reinstatement of its quarterly dividend to pre-COVID-19 levels was a strong signal of management’s bullish outlook on the business. Because we think that the company will continue to recover from the COVID-19 headwinds, we believe that the high dividend is safe. We can start to see future dividend growth coming soon. Thus, Cracker Barrel is worth the research for an income and dividend growth investor.

{kind=link}

{kind=link}

{kind=link}