Hardgoods Momentum Drives Chewy's Expansion Beyond Consumables

Chewy, Inc.’s CHWY Hardgoods segment showed exceptional strength in the second quarter of fiscal 2025, highlighting its expanding role in diversifying sales beyond consumables. Hardgoods revenues grew more than 15% year over year, outpacing total sales growth of 8.6%. The rebound was driven mainly by structural volume growth, reflecting strong underlying demand and improved customer engagement in discretionary categories.

Over the past two quarters, Chewy has onboarded more than 1,500 new brands and enhanced inventory freshness, allowing pet parents to access a wider and more diverse selection. Improved fulfillment execution and higher in-stock levels supported seamless service during peak periods. These operational upgrades enable faster market response and higher customer satisfaction.

Management emphasized that Hardgoods gains were broad-based across subcategories, driven by better merchandising, personalization and on-site visibility. To maintain availability and protect pricing power amid tariff concerns, Chewy invested $3-$5 million in additional inbound processing during the fiscal second quarter. Although this temporarily lifted SG&A expenses, it positioned Chewy to sustain pricing competitiveness as peers face inflationary pressures.

The resurgence of Hardgoods also supported margin expansion, contributing to Chewy’s gross margin improvement of 90 basis points year over year to 30.4%. Alongside premium consumables and health, Hardgoods strengthened the overall product mix and demonstrated leverage from Chewy’s scaling fulfillment infrastructure.

Reflecting this momentum, Chewy raised fiscal 2025 net sales guidance to $12.5-$12.6 billion, representing 7-8% growth when adjusted for the prior year’s extra week. With double-digit volume gains and improving product economics, the Hardgoods segment is emerging as a pivotal growth engine.

How Do CENT & WOOF Stack Up Against CHWY’s Sales Growth?

Chewy's net sales have outperformed those of its key competitors, including Central Garden & Pet Company CENT and Petco Health and Wellness Company, Inc. WOOF.

Central Garden & Pet reported third-quarter fiscal 2025 net sales of $961 million, down 4% year over year, primarily reflecting the exit of two product lines in its Garden distribution business, extended periods of cool and rainy weather and continued softness in pet durables. Growth in Wild Bird, Fertilizer and Packet Seeds categories, along with double-digit e-commerce gains, helped offset Central Garden & Pet’s broader sales declines.

Petco Health and Wellness reported second-quarter fiscal 2025 net sales of $1.49 billion, down 2.3% year over year, mainly reflecting store closures and the strategic exit from unprofitable sales. Comparable sales declined 1.4%, while adjusted EBITDA of Petco Health and Wellness increased $30 million to $114 million, expanding nearly 220 basis points to 7.6% of sales.

CHWY’s Price Performance, Valuation & Estimates

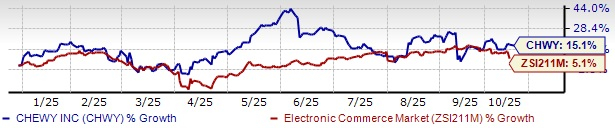

Shares of Chewy have gained 15.1% year to date compared with the industry’s growth of 5.1%.

Image Source: Zacks Investment Research

From a valuation standpoint, CHWY trades at a trailing price-to-sales ratio of 1.34X, below the industry’s average of 2.58X. It has a Value Score of C.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for CHWY’s fiscal 2025 and 2026 earnings implies year-over-year growth of 22.1% and 20.4%, respectively. Estimates for fiscal 2025 and 2026 have been unchanged and revised upward by 1 cent, respectively, over the past 30 days.

Image Source: Zacks Investment Research

CHWY currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Central Garden & Pet Company (CENT): Free Stock Analysis Report

Petco Health and Wellness Company, Inc. (WOOF): Free Stock Analysis Report

Chewy (CHWY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Source Zacks-com

{kind=link}

{kind=link}

{kind=link}