Updated on September 25th, 2020 by Nate Parsh

The Dividend Kings are an exclusive group of dividend stocks that satisfy our most stringent criteria for dividend history.

More specifically, each Dividend King has increased its dividend for a remarkable 50 consecutive years. You can see the full list of all 30Dividend Kings here.

We have created a full downloadable list of all Dividend Kings, along with important financial metrics such as price-to-earnings ratios and dividend yields. You can download your copy of the Dividend Kings list by clicking on the link below:

Click here to download my Dividend Kings Excel Spreadsheet now. Keep reading this article to learn more.

Commerce Bancshares (CBSH) is one example of a slow-and-steady Dividend King. With that said, the company flies under the radar of many dividend growth investors because it has a low market capitalization of just $6 billion.

In this article, we will examine Commerce Banchshares investment appeal by considering its business model, growth prospects, and current valuation in detail.

Business Overview

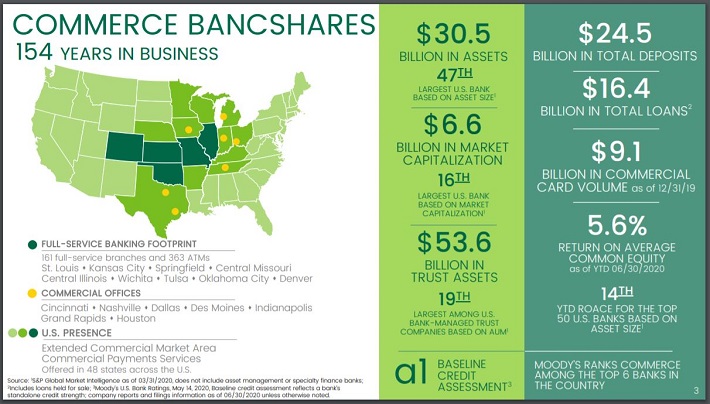

Commerce Bancshares has an easy-to-understand business model. The company is a bank holding company whose principal subsidiary is Commerce Bank.

Source: Commerce Bancshares’ Second Quarter Earnings Presentation, slide 3

Commerce Bank offers general baking services to both retail and business customers, with offers ranging from retail and corporate banking to asset management and investment banking. Commerce Bank was founded in 1865 and operates branches in the following states:

- Colorado

- Missouri

- Kansas

- Illinois

- Oklahoma

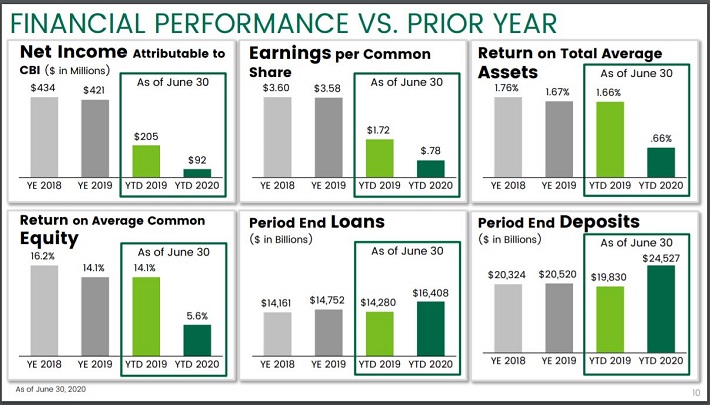

The company is currently headquartered in Kansas City, Missouri. Commerce Bancshares had a difficult second quarter. A summary of the bank’s performance can be seen below.

Source: Commerce Bancshares’ Second Quarter Earnings Presentation, slide 10

Revenue fell 5.5% to $324 million while earnings-per-share declined 59%, to $0.37. Much of the year-over-year declines for both the top and bottom-lines was due to additional provisions for loan losses, of $78 million.

Net income would have increased slightly from the first quarter of the year had the additional loan losses not been included. This shows how much the coronavirus has impacted the company’s business. On the bright side, Commerce Bancshares’ loan portfolio grew 15% to $16.4 billion while quarter-end deposits rose 24%.

For financial companies, an important metric is book value per common share. On this measure, Commerce Bancshares performed admirably. The company’s book value per common share increased almost 10% from the same period a year ago and 3.4% from the first quarter of 2020.

Growth Prospects

Commerce Bancshares has a solid if unspectacular growth track record. Through the ten-year period ending last fiscal year (2019), the bank managed to increase its earnings-per-share by 7.2% per year.

Looking ahead, Commerce Bancshares’ growth prospects have not changed by much over the last decade. The bank’s growth continues to be dependent on the following factors:

- Net Interest Margin: the company’s financial results are very sensitive to the spread between the interest rates it pays on its deposits and the interest rates it earns on its loans.

- Loan Growth: The company’s revenue is very dependent on the continued expansion of its loan portfolio.

- The Yield Curve: The Federal Reserve members have stated that they expect interest rates to be at or near zero for the foreseeable future. This will likely have a negative impact near term results.

- Share Repurchases: Commerce Bancshares has reduced its share count by 6.6% over the last 10 years, which has boosted its shareholder yield during this time period.

Overall, we believe the company is likely to nearly replicate its historical growth moving forward, and are forecasting 6% growth in earnings-per-share through the next half-decade.

Competitive Advantages & Recession Performance

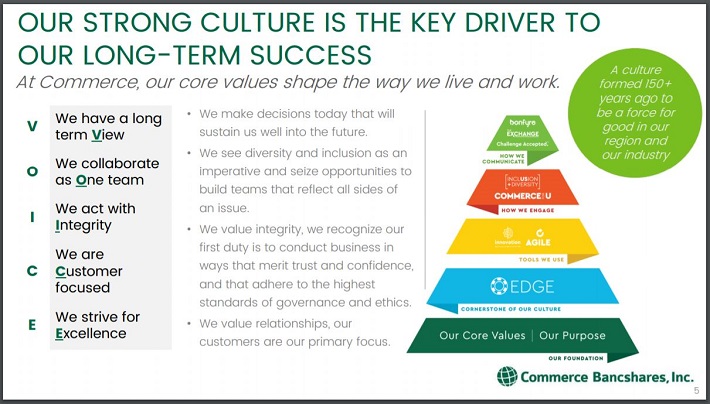

As the following image indicates, Commerce Bancshares believes that its culture is a source of competitive advantage for the firm.

Source: Commerce Bancshares’ Second Quarter Earnings Presentation, slide 5

Commerce Bancshares performed exceptionally well during the last recession compared to its peers in the lending industry. The company’s earnings trajectory during the 2007-2009 financial crisis is shown below:

- 2006 adjusted earnings-per-share: $1.72

- 2007 adjusted earnings-per-share: $1.65

- 2008 adjusted earnings-per-share: $1.52

- 2009 adjusted earnings-per-share: $1.33

- 2010 adjusted earnings-per-share: $1.71

- 2011 adjusted earnings-per-share: $2.00

Commerce Bancshares’ adjusted earnings-per-share declined by 19.4% peak-to-trough during the worst of the Great Recession during a time period when many larger lenders executed recapitalization programs that were devastating to continuing shareholders.

Perhaps more importantly, Commerce Bancshares continued its multi-decade streak of consecutive dividend increases. Because of this, we believe the company will perform very well during any future economic downturns.

Valuation & Expected Returns

As with all common equities, Commerce Bancshares future returns can be estimated by looking at each of the three contributors to returns: dividend payments, earnings growth, and valuation changes.

Dividend payments are the most predictable contributor to total returns. Commerce Bancshares currently pays a quarterly dividend of $0.27 per share, which yields 2.0% on the company’s current stock price of ~$54. Commerce Bancshares has raised its dividend for 52 consecutive years.

The second most predictable source of returns is earnings-per-share growth. As we outlined earlier in this article, Commerce Bancshares’ current growth prospects are very similar to its historical growth prospects, so we believe the company will be capable of matching its historical growth rate moving forward. We expect 6% annual earnings growth over full economic cycles.

Lastly, let’s discuss the bank’s current valuation. Commerce Bancshares is expected to earn $2.35 of earnings-per-share in 2020. This is a decline of 34% from 2019 and means that the stock is trading at a current price-to-earnings ratio of 22.9.

However, this decline is due almost entirely to loan losses attributed to the coronavirus pandemic. Eventually, the pandemic will subside and likely mean a reversal of fortunes for the bank. We have believe that Commerce Bancshares’ underlying earnings power of $3.60 is more accurate measure to use to calculate fair value. Using this number, the current price-to-earnings ratio is 14.9.

The company’s 10-year average price-to-earnings ratio is 16.5, but we believe that fair value for Commerce Bancshares lies somewhere closer to 12 times earnings given comparable valuations in the lending sector. If the company’s valuation were to contract to 12 times earnings over the next 5 years, this would reduce the company’s returns by 4.2% annually.

Therefore, total returns would consist of the following:

- 6% earnings growth

- 2% dividend yield

- -4.2% multiple reversion

Commerce Bancshares are expected to provide a total return of just 3.8% annually through 20205. Because of this high valuation, the bank earns a sell recommendation from Sure Dividend at current prices.

Final Thoughts

Commerce Bancshares has a dividend history that few companies in the financial services industry can match. Unfortunately, the company’s valuation is even richer than its dividend history. We suspect that valuation contraction will be a negative contributor to Commerce Bancshares’ future returns.

Because of this, the company earns a hold recommendation today. Prospective investors would do well to monitor its stock price and perhaps accumulate shares on any meaningful dips.

{kind=link}

{kind=link}

{kind=link}