Updated on October 22nd, 2020 by Josh Arnold

Utility stocks are often associated with long histories of paying dividends to shareholders. Their relatively predictable earnings and recession resistance combine to make increasing dividends somewhat easier over the long-term than a business that is highly cyclical. However, not all utility stocks are created equal in this sense.

There are four utility stocks on the prestigious list of Dividend Kings, a group of stocks with at least 50 consecutive years of dividend increases. You can see all 30 Dividend Kings here.

You can also download an Excel spreadsheet with the full list of Dividend Kings (plus important metrics such as price-to-earnings ratios and dividend yields) by clicking on the link below:

Click here to download my Dividend Kings Excel Spreadsheet now. Keep reading this article to learn more.

Northwest Natural Holdings (NWN) is one of those four utility stocks in the list of Dividend Kings, and it recently increased its dividend for the 65th consecutive year, giving it one of the longest streaks anywhere in the market.

Below, we’ll assess Northwest’s business, its growth prospects, and whether to buy, sell, or hold.

Business Overview

Northwest was founded more than 160 years ago as a natural gas utility in Portland, Oregon. It has grown from a very small, local utility that provided gas service to a handful of customers to a very successful regional utility with interests that now include water and wastewater, which were purchased in recent acquisitions.

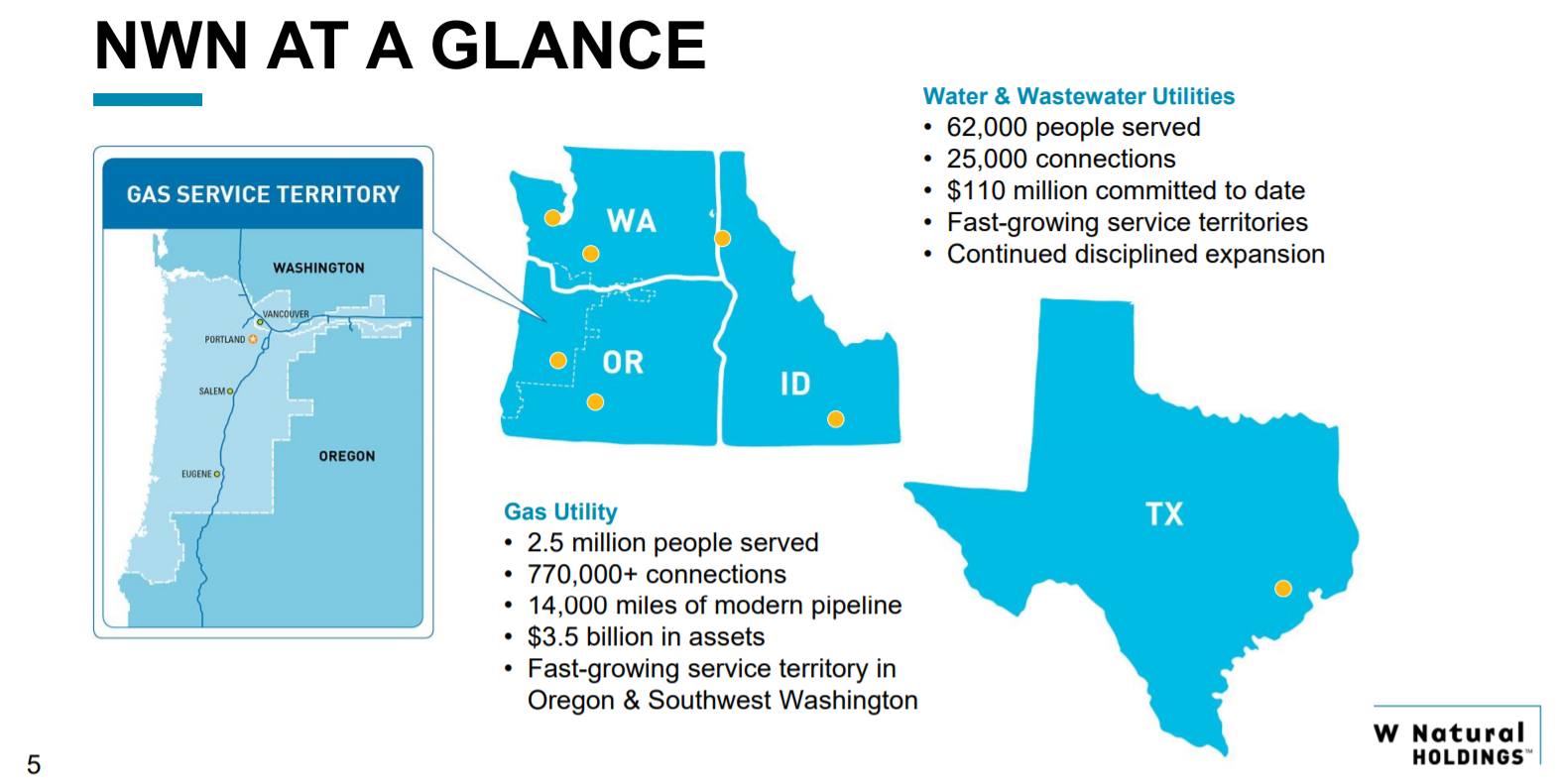

Source: Investor presentation, page 5

Northwest provides gas service to 2.5 million customers in 140 communities in Oregon and Washington, serving 770,000 meters through its network of pipelines. It also owns and operates 35 billion cubic feet of underground gas storage capacity. Finally, its fairly recent move into water has grown to 25,000 connections serving more than 60,000 people.

Northwest produces nearly $800 million in annual revenue and trades with a market capitalization of $1.4 billion after a sizable decline thus far in 2020.

Next, we’ll assess Northwest’s growth prospects.

Growth Prospects

Northwest has had a difficult time growing earnings-per-share in the past decade, despite the fact that the company has managed to acquire customers fairly steadily during that time frame. The company has struggled with rate cases in some of its localities, although it has experienced more recent success in Oregon with raising prices. Since Northwest is a regulated utility, it must ask for pricing increases from local authorities.

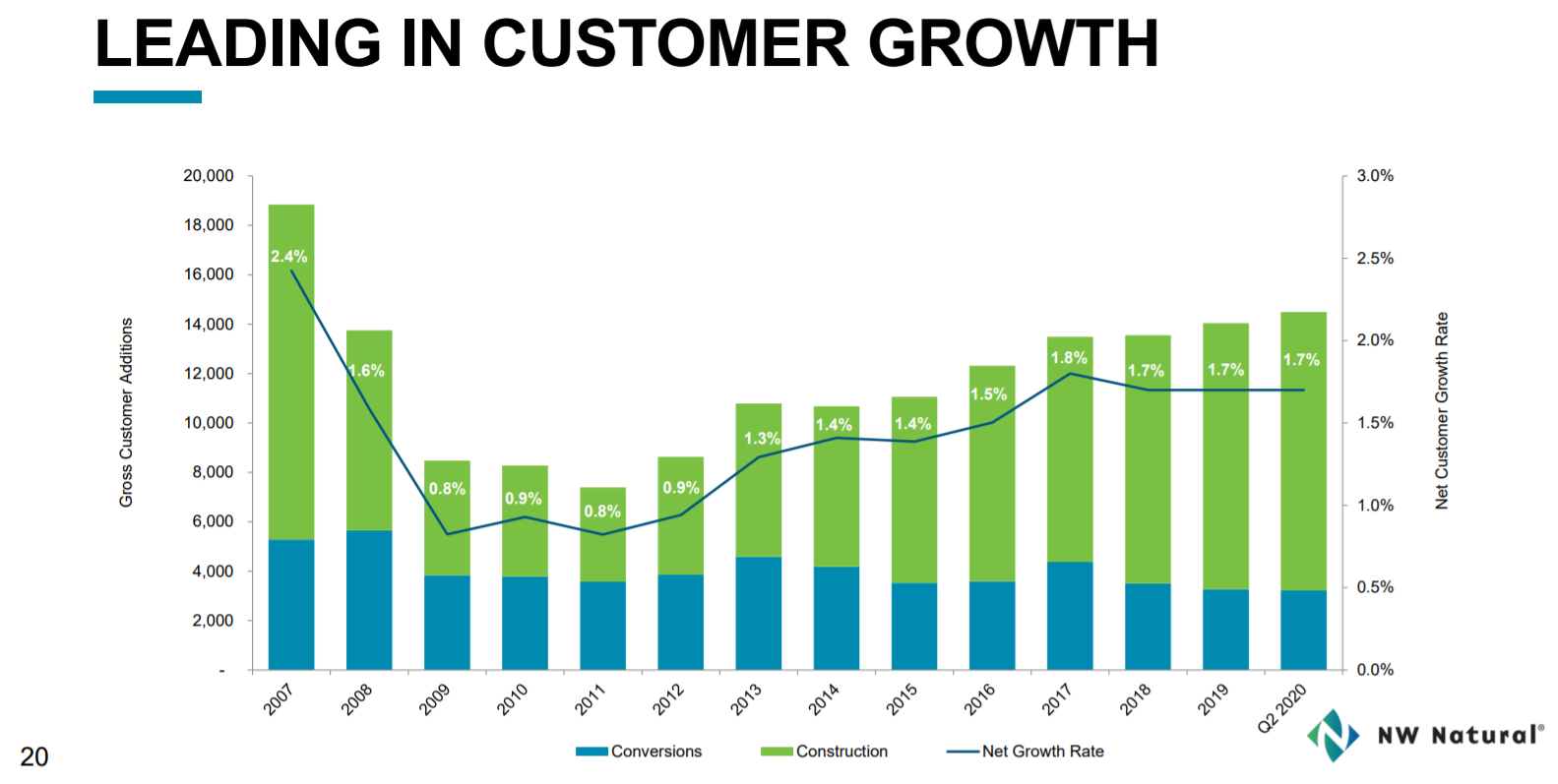

Source: Investor presentation, page 20

Northwest’s customer growth, as we can see above, has been quite strong over the past decade. It has a combination of conversions and new construction, both of which have helped move the needle over time by low-single digits. We believe the demographics of Northwest’s served communities support indefinite customer growth, so this should continue to be a tailwind.

The pandemic has caused Northwest to incur significant costs, although we believe these costs will largely be a 2020 story, and gradually unwind into next year.

Source: Investor presentation, page 14

Northwest has done things like invest in employee safety, voluntarily suspended fees for customers, strengthened liquidity, and applied for deferrals with its regulators. These items have seen Northwest incur costs above and beyond what was forecast for this year, but moving into 2021, we should see these normalize.

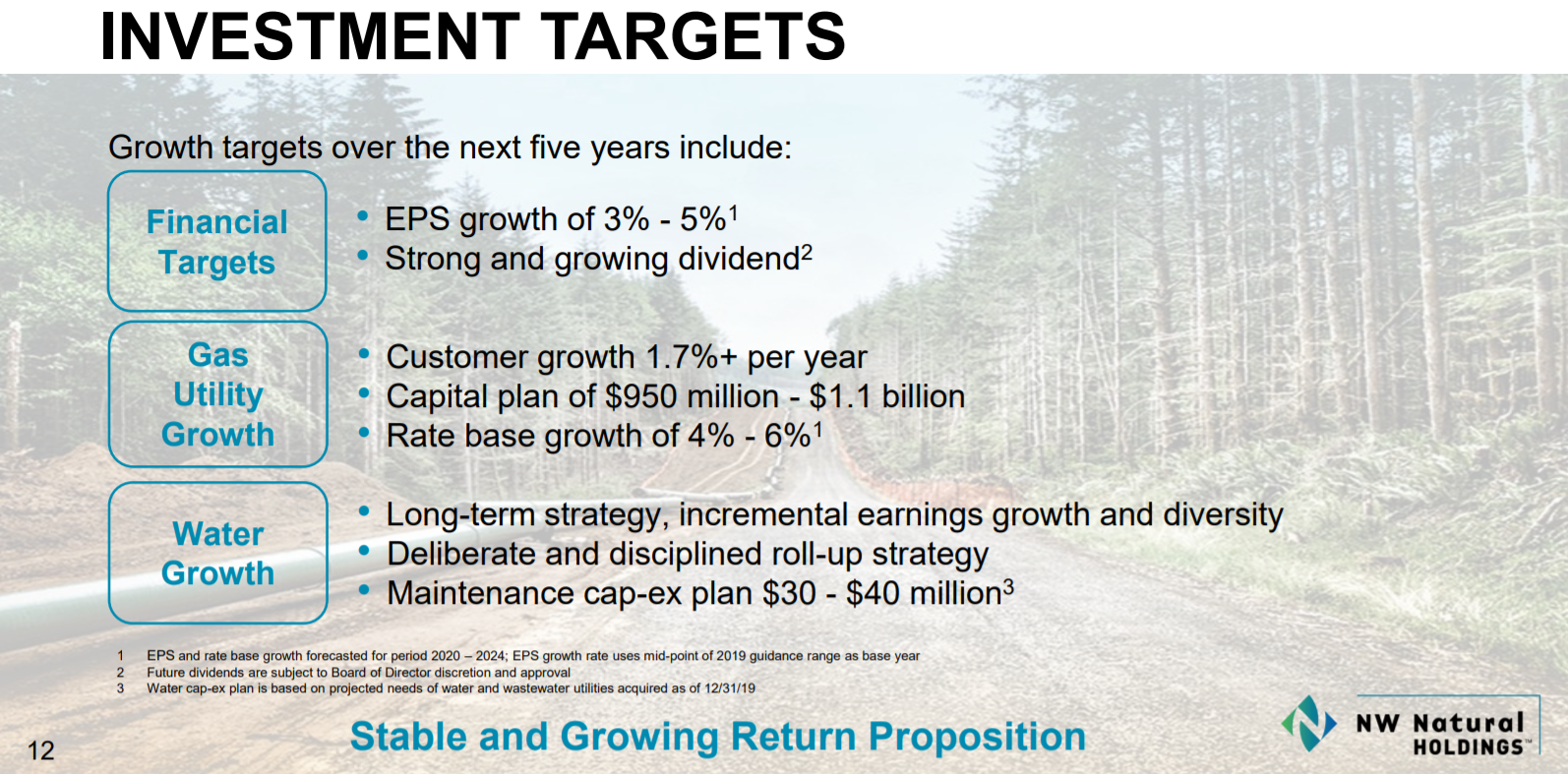

Below, Northwest has laid out what it sees as growth targets for the next five years.

Source: Investor presentation, page 12

The company believes it can grow earnings-per-share at 3% to 5% annually while increasing its dividend. It plans to get there by growing its customer count by at least 1.7% annually – which is consistent with historical performance – as well as rate base growth of 4% to 6%. We believe customer growth will be steady, but Northwest’s history on rate cases has us a bit more cautious on rate growth.

Still, we assess long-term growth potential at 2.9% annually for Northwest in the coming years.

Competitive Advantages & Recession Performance

Northwest’s competitive advantage is much like any other utility; it has a virtual monopoly in its service area. The utility business model is vastly different from just about any other type of business as it requires regulatory approval for things like capex and pricing increases, but in return, the company gets a captive audience to sell products and services to.

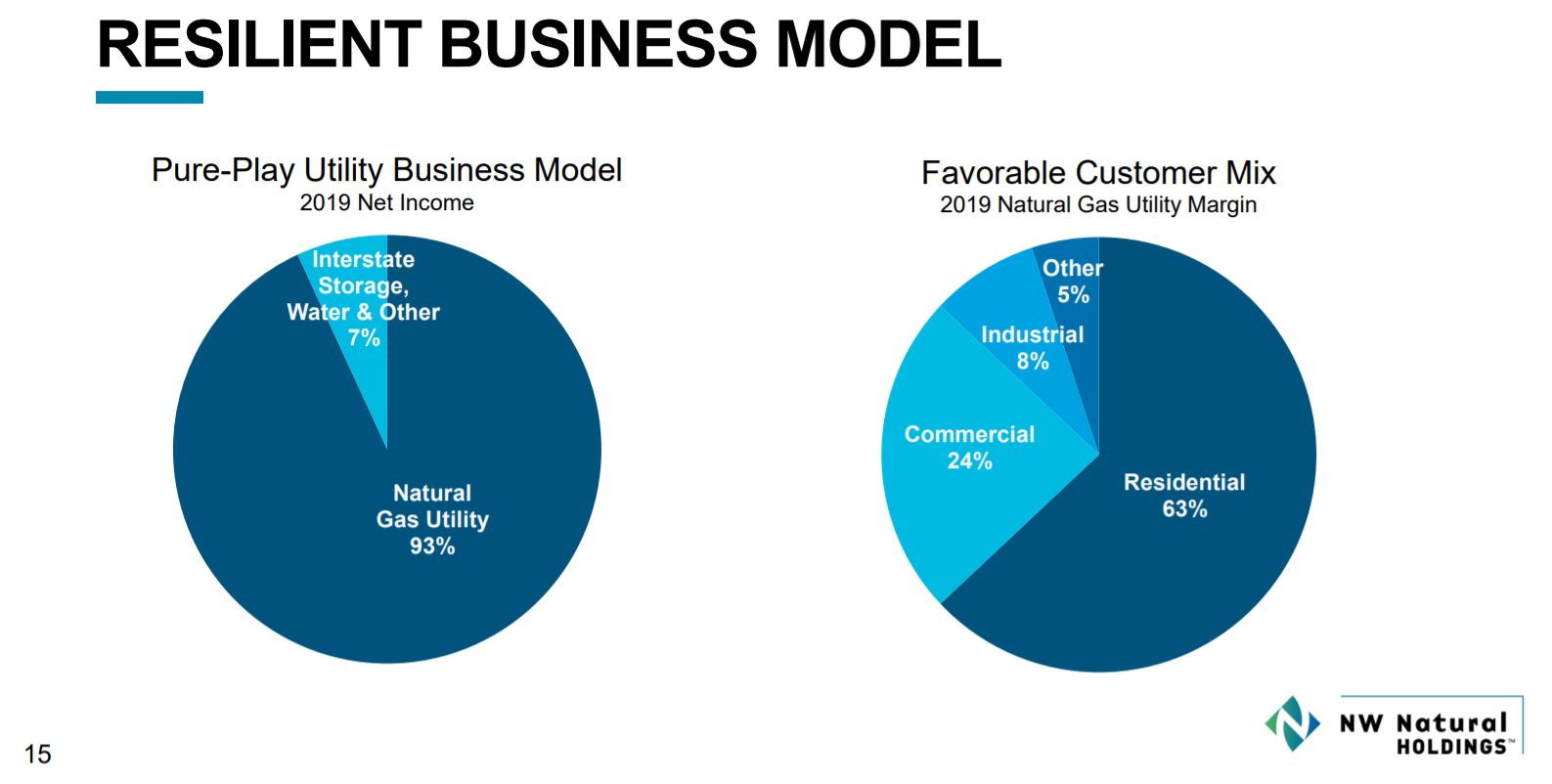

Source: Investor presentation, page 15

Northwest’s model is almost entirely natural gas-based, but its burgeoning water business should take revenue share over time. We believe that Northwest’s fairly heavy concentration on residential customers will continue to serve it well through the pandemic.

Stay-at-home orders, as well as a move by employers to allow people to work from home, have created a situation where residential customers consume more water and natural gas at home. We believe a residential-heavy revenue mix is the path forward for utilities, and Northwest is well-positioned for that.

Below, we have Northwest’s earning-per-share before, during, and after the Great Recession:

- 2007 earnings-per-share: $1.44

- 2008 earnings-per-share: $1.52 (5.6% increase)

- 2009 earnings-per-share: $1.60 (5.3% decrease)

- 2010 earnings-per-share: $1.68 (5.0% increase)

Northwest was able to not only maintain its earnings during a deep and long recession, but it produced at least 5% earnings-per-share growth each year before, during, and following the Great Recession. That’s an extremely impressive track record and for a dividend stock, nothing could be more attractive. Performance like this is why Northwest has been able to produce dividend increases for 65 consecutive years.

The one note of caution on the dividend is that years of lackluster earnings-per-share growth has led to a situation where the constantly-rising dividend is catching up. Indeed, the payout ratio is now in excess of 80% of earnings, and while that’s okay given Northwest’s predictable earnings base, investors should note that increases are likely to be quite small until earnings growth picks up. The most recent increase was just 0.5%, illustrating this point. We believe the current dividend is safe for the foreseeable future, but we note that payout growth will likely be difficult to come by.

Valuation & Expected Returns

Northwest began the year trading at a very elevated valuation, so the massive selloff we’ve seen has simply unwound that and put the stock right near our fair value estimate. At today’s price, Northwest trades for 19.5 times this year’s earnings, which is nearly identical to our estimate of fair value of 20 times earnings. We therefore expect a diminutive tailwind to total returns from the valuation.

The current yield is 4.2%, which is very high by Northwest’s own historical standards, so combining it with the valuation and expected growth, we forecast total annual returns of 7% moving forward. That’s a big improvement over forecasted returns of less than 3% earlier this year, so we see Northwest as much more attractively priced than it has been since the early-2010s.

Final Thoughts

While Northwest has some challenges to face, we believe its strategic direction of focusing on building out its residential business while purchasing growth through the water utility will serve it well in the years to come. Rate cases remain a wildcard, but steady customer growth is attractive and should help at least buoy earnings at current levels, if not produce a bit of growth.

With the share price down a whopping 38% so far this year, Northwest offers a much better value proposition than it has in the past few years. With total returns projected at 7% annually, we see Northwest as a hold, but note that its exceptional dividend history and 4%+ yield are likely quite attractive to income-focused investors.

{kind=link}

{kind=link}

{kind=link}