Published on October 15th, 2020 by Aristofanis Papadatos

Cincinnati Financial (CINF) has a dividend track record that few companies can rival. The company has increased its cash dividend for 59 consecutive years, making it one of just 8 such entities in the entire market with a dividend increase streak of at least 59 years.

That puts Cincinnati Financial among the elite of Dividend Kings, a small group of stocks that have increased their payouts for at least 50 consecutive years. You can see the full list of all 30 Dividend Kings here.

You can also download an Excel spreadsheet with the full list of Dividend Kings (plus metrics that matter such as price-to-earnings ratios and dividend yields) by clicking on the link below:

Click here to download my Dividend Kings Excel Spreadsheet now. Keep reading this article to learn more.

Dividend Kings have the longest track records when it comes to rewarding shareholders with cash, and Cincinnati Financial is no different. Cincinnati Financial has a relatively boring business and thus it passes under the radar of most investors. However, the company certainly has a successful history of raising its dividend.

Cincinnati Financial is offering a 3.0% dividend yield, which is double the yield of the S&P 500 (1.5%). It has also grown its dividend at a consistent 4% average annual rate over the last decade. Thanks to its healthy payout ratio of 75% and its strong balance sheet, the insurer has ample room to keep raising its dividend for many more years.

On the other hand, income-oriented investors should not expect high dividend growth due to the volatile nature of the property-and-casualty insurance business and hence they should wait patiently to find this stock at a more attractive valuation level.

Business Overview

Cincinnati Financial is a property-and-casualty (P/C) insurance company founded in 1950. It offers business, home, auto insurance, and financial products, including life insurance, annuities, property, and casualty insurance. It is headquartered in Ohio and is trading with a market capitalization of $12.7 billion.

As an insurance company, Cincinnati Financial makes money in two ways. It earns income from the insurance premiums of the policies it sells to its customers and also earns investment income by investing its float, i.e., the money it receives from its customers minus the amounts it pays for the claims of its customers.

The latter is actually the reason behind the great interest of Warren Buffett in the insurance business from the very beginning of his investing career. He noticed that this business generates a great amount of float, which can be invested with a high rate of return and thus generate excessive compounded returns.

On the other hand, the P/C insurance business can be especially tricky for investors. Some insurers are often tempted to reduce the premiums they charge in order to entice more customers and thus enhance their market share. During favorable years, in which catastrophic losses are low, these insurers will post high levels of profits.

However, a year with high catastrophic losses will inevitably show up at some point and will erase the profits of all the previous years if the insurers have not followed a prudent underwriting policy. This means that investors should evaluate P/C insurers based only on their long-term performance.

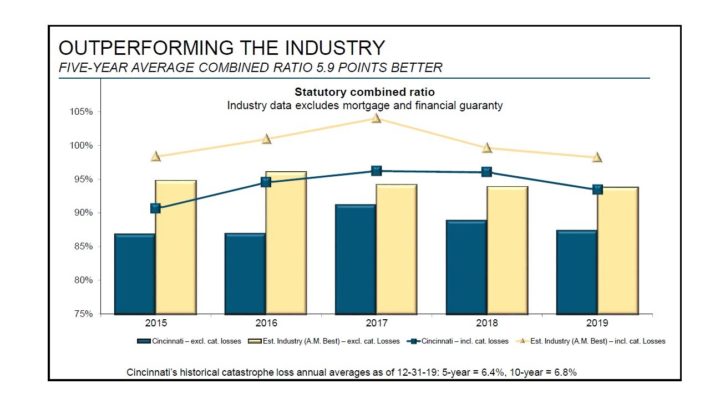

Cincinnati Financial is better than average in this respect when compared to its peers. In the last five years, the company has posted a combined ratio 5.9 percent points better (lower) than that of its peers.

Source: Investor Presentation

The combined ratio is the primary index of performance of P/C insurers, as it is the ratio of the amount of claims paid to the amount of premiums received. As is evident from this definition, the lower the combined ratio the better.

Cincinnati Financial has managed to maintain a superior combined ratio thanks to the predictive modeling tools and analytics it uses as well as data management in order to determine the probability of each catastrophic event and thus set the appropriate price for each customer.

The superior underwriting policy of Cincinnati Financial is evident, not only from its superior combined ratio, but also from its exceptional dividend growth record. As catastrophic losses are very volatile in nature, they are extremely high in a few adverse years.

Consequently, it is nearly impossible for most insurers to grow their dividends during these few rough years. Cincinnati Financial is a bright exception to this rule, as it has raised its dividend for 59 consecutive years. This is a testament to its prudent underwriting policy and the long-term perspective of its management.

Another factor behind the exceptional dividend record of Cincinnati Financial is the healthy payout ratio that the company has always targeted in order to create a wide margin of safety for its dividend.

Source: Investor Presentation

A low payout ratio sometimes results in a low dividend yield but this is not the case for Cincinnati Financial. The stock is offering a 3.0% dividend yield, which is double the 1.5% yield of the S&P 500. Thanks to its healthy payout ratio and its financial strength, the insurer can keep raising its dividend for many more years.

Cincinnati Financial is currently facing strong headwinds due to the pandemic and high catastrophic losses in this year. In the second quarter, which was marked by unprecedented lockdowns, the company incurred $65 million of losses due to the pandemic, as it offered stay-at-home credit in its auto insurance policies and waived vacancy clauses for buildings temporarily closed due to the pandemic.

As if the pandemic were not enough, Cincinnati Financial incurred $231 million of catastrophic losses in the second quarter and thus its adjusted earnings per share plunged 48% over the prior year’s quarter, from $0.85 to $0.44. Due to the strong headwinds facing the insurer this year, the company is poised to report an approximate 24% decrease in its adjusted earnings per share this year, from $4.20 to $3.19.

Growth Prospects

As mentioned above, this year is exceptionally adverse for P/C insurers due to the high catastrophic losses related to adverse weather and the material losses related to the pandemic. However, a rough year every few years should be expected in this business. Investors should focus on the long-term prospects of P/C insurers and we believe that the future growth prospects of Cincinnati Financial are intact.

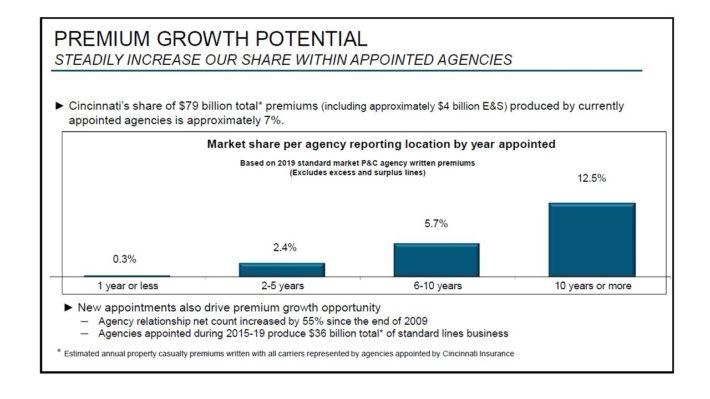

Management targets a 10%-13% average annual growth rate over the next five years. As per its definition, the growth rate is equal to the growth rate of the book value per share plus the dividends paid to the shareholders. Cincinnati Financial has achieved a 14.2% average annual growth rate over the last five years.

It aims to achieve a 10%-13% growth rate over the next five years primarily via new agency appointments and premium growth in the already appointed agencies. 187 new agencies were appointed last year and 72 new agencies have been appointed in the first half of this year.

As shown in the chart below, Cincinnati Financial has consistently increased its market share in its agencies over time.

Source: Investor Presentation

Its market share remains low in the first five years from the appointment of each agency but then it rises significantly and thus contributes to significant premium growth.

On the other hand, the company generates a great portion of its earnings from its investment gains and thus it is highly sensitive to the prevailing interest rates and the stock market performance. Notably, Cincinnati Financial is a somewhat aggressive investor, with 37% of its investment portfolio being invested in stocks. It is remarkable that 28% of the stock portfolio of Cincinnati Financial is invested in the technology sector. Given the impressive rally of NASDAQ this year, the merits of this strategy are evident.

However, this strategy renders the company vulnerable to a potential bear market. Moreover, interest rates are around all-time lows due to the pandemic and thus they exert pressure on the yield of the bond portfolio of the insurer. Due to all the above factors, we prefer to be conservative and thus we expect Cincinnati Financial to grow its earnings per share by only 1.0% per year on average over the next five years.

Competitive Advantages & Recession Performance

Cincinnati Financial boasts of the great relationships it has with most of its agents, which help the insurer earn access to the best accounts of its agents. In addition, it has a good reputation for its financial strength and its efficient procedures in claim payments. These features provide some sort of competitive advantage.

On the other hand, this competitive advantage is narrow. The P/C insurance is characterized by intense competition, which has heated more than ever in recent years. Warren Buffett has repeatedly stated that the best days for insurers belong to the past due to the intense competition prevailing right now.

Moreover, Cincinnati Financial is vulnerable to recessions due to its high exposure to the stock market and its sensitivity to interest rates. During recessions, interest rates remain depressed and thus take their toll on the yield of the bond portfolio of the insurer.

In fact, interest rates have remained suppressed for more than a decade. As a result, the new bonds offer lower yields than the mature bonds of the portfolio. The pre-tax yield of Cincinnati Financial’s bond portfolio has steadily declined, from 4.7% in 2015 to 4.1% now. The interest rate cuts implemented by the Fed due to the pandemic this year will continue to exert a drag on the yield of the bond portfolio of Cincinnati Financial.

Valuation & Expected Returns

We expect Cincinnati Financial to generate earnings-per-share of $3.19 this year. As a result, the stock is trading at a forward price-to-earnings ratio of 24.7. This is much higher than the average price-to-earnings ratio of 20.0 of the stock over the last decade.

A rich valuation is somewhat justified this year, as the results of this year are lower than the long-term potential of the company due to exceptionally high catastrophic losses and the losses caused by the pandemic. On the other hand, the stock is richly valued right now, which raises a red flag for its expected future returns.

If the stock reaches our fair valuation level over the next five years, it will incur a 4.1% annualized drag in its returns due to the contraction of its earnings multiple. We also expect 1% annual EPS growth over the next five years while the stock is also offering a 3.0% dividend yield. Both of these items will add positively to shareholder returns.

However, they are not sufficient to offset the overvaluation of the stock. Overall, the stock is likely to offer just a 0.5% average annual return over the next five years. As a result, such a low expected rate of return gets the stock a sell recommendation at this time.

Final Thoughts

Cincinnati Financial is a high-quality P/C insurer. The exceptional dividend record of the company, with 59 consecutive years of dividend raises, is a testament to its disciplined underwriting policy and the long-term perspective of management.

However, the stock is somewhat overvalued right now. This is a common occurrence these days, with the S&P 500 Index sitting near a record high. It is becoming much harder to find reasonably-valued dividend stocks with high yields and growth potential.

Cincinnati Financial is offering an attractive 3.0% dividend yield and mid-single-digit dividend growth but its valuation is rich. As a result, investors should wait for a significant decline of the stock price of this Dividend King before buying its shares.

{kind=link}

{kind=link}

{kind=link}