Published on October 13th, 2020 by Josh Arnold

The Dividend Kings are the best-of-the-best when it comes to returning cash to shareholders. These are stocks that have 50+ year histories of increasing their dividends to shareholders. These stocks are generally ones that long-term income investors seek out due to their earnings stability, and impressive dividend track records.

Just 30 companies qualify as Dividend Kings. You can see all 30 Dividend Kings here.

You can also download an Excel spreadsheet with the full list of Dividend Kings (plus metrics that matter such as price-to-earnings ratios and dividend yields) by clicking on the link below:

Click here to download my Dividend Kings Excel Spreadsheet now. Keep reading this article to learn more.

Colgate-Palmolive is a consumer staples conglomerate that has increased its dividend for 57 consecutive years, one of the longest streaks in the entire market. Perhaps more impressively, Colgate-Palmolive has paid dividends on its common stock continuously since 1895.

Colgate-Palmolive has been working on improving growth in recent years, and the pandemic has only served to accelerate this effort. Below, we’ll discuss the company’s growth prospects, its valuation, and its ever-important dividend.

Business Overview

Colgate-Palmolive was founded in 1806, and has built an impressive and extensive portfolio of consumer brands. It operates globally, selling in most countries around the world. About one-sixth of its revenue comes from its Hill’s pet food division, which has shown very strong growth in recent years.

The other five-sixths of revenue come from a mix of cleaning and personal care products, with the company’s most recognizable brands being Colgate (tooth care) and Palmolive (soap). However, Colgate-Palmolive has built a diverse slate of brands well outside of just its two namesake brands.

Colgate-Palmolive trades currently for a $67 billion valuation, and the company produces about $16 billion in annual revenue.

Source: Investor presentation, page 8

Colgate-Palmolive has structured itself into four units: Oral Care, Personal Care, Home Care, and Pet Nutrition. The company has created and acquired numerous brands over time, and more recently, has worked to innovate with its best brands through line extensions.

Below, we’ll look at the company’s growth prospects.

Growth Prospects

We expect Colgate-Palmolive to post 6% average earnings-per-share growth in the coming years, as it has a few levers it can pull to power the bottom line higher. The company has been exposed to forex translation since it sells globally, meaning it is beholden to many different currencies and their relative value against the dollar.

In addition, commodity volatility has taken its toll at times on margins, although the company has undertaken cost saving measures to combat this.

Source: Investor presentation, page 49

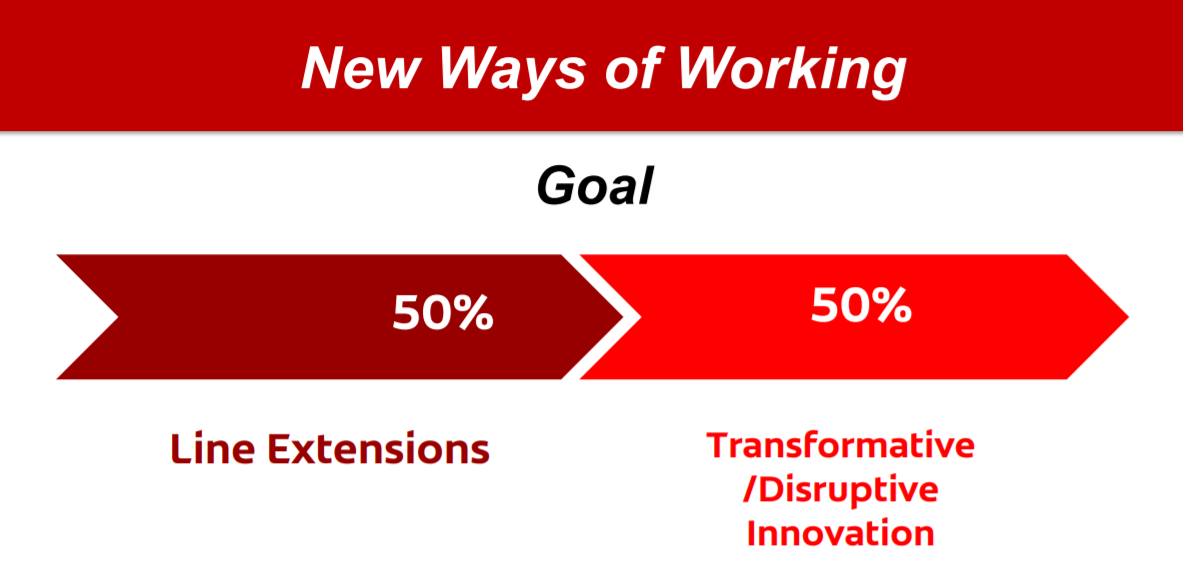

Another way Colgate-Palmolive has worked to improve growth is to work true innovation into its portfolio, rather than just creating a slightly different version of an existing product. That has worked well for the company too, but the idea is to take its enormous R&D budget and create new products. Over time, this can lead to incremental revenue growth.

Line extensions, however, still work quite well for Colgate-Palmolive because it can leverage its highly recognizable, global brands.

Source: Investor presentation, page 33

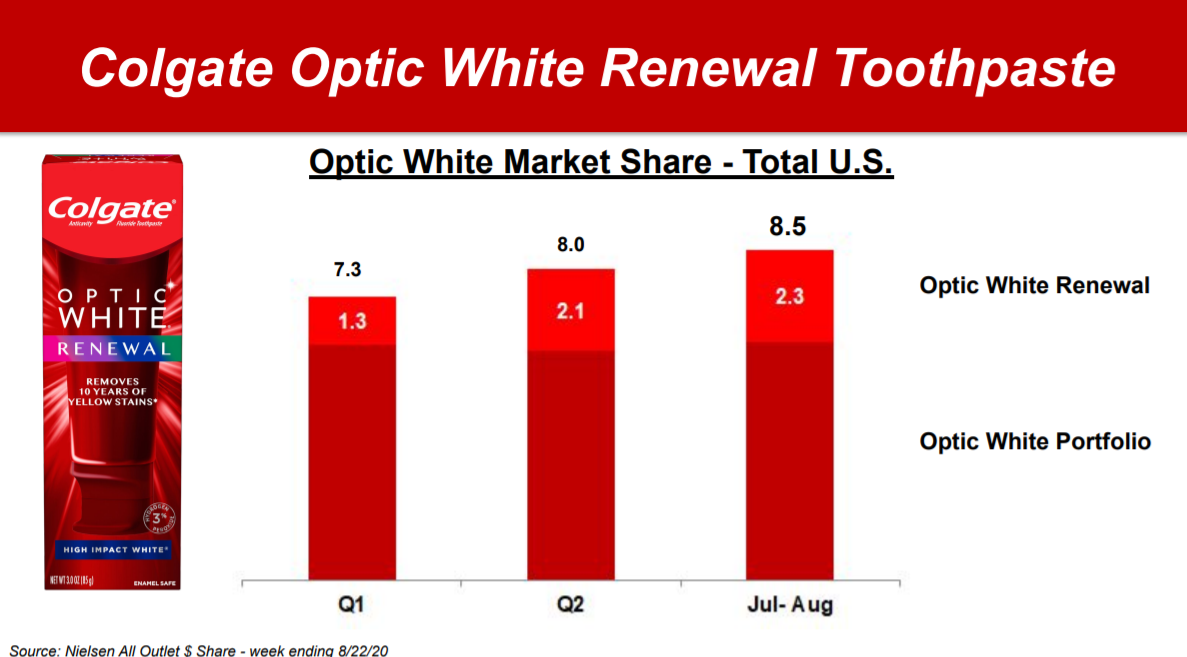

An example of this is above, where the company took its flagship Colgate brand and extended it up market, which has subsequently taken large chunks of a very large market. Colgate-Palmolive has done this with numerous products, with its Optic White Renewal being a particularly successful example.

Source: Investor presentation, page 43

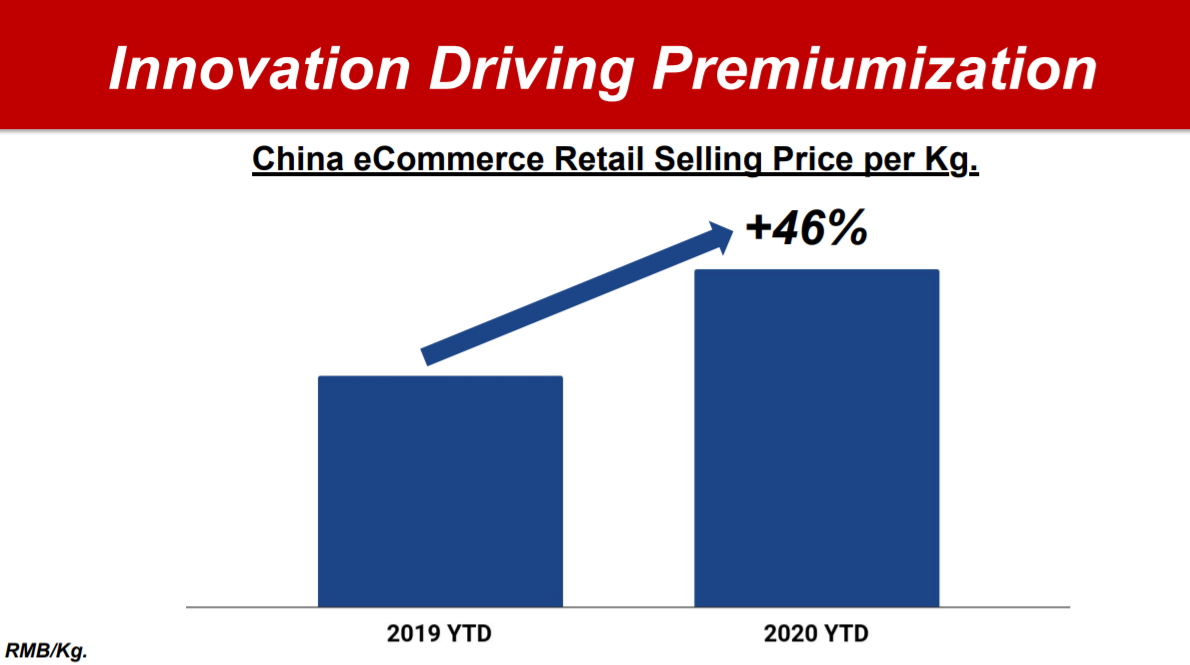

Finally, Colgate-Palmolive has concentrated its R&D dollars on what it calls “premiumization”, which is moving up-market with its products, as it did with Optic White. The above image is an example of success of this strategy in China, but the concept applies everywhere, to generate more revenue through the same volume of products.

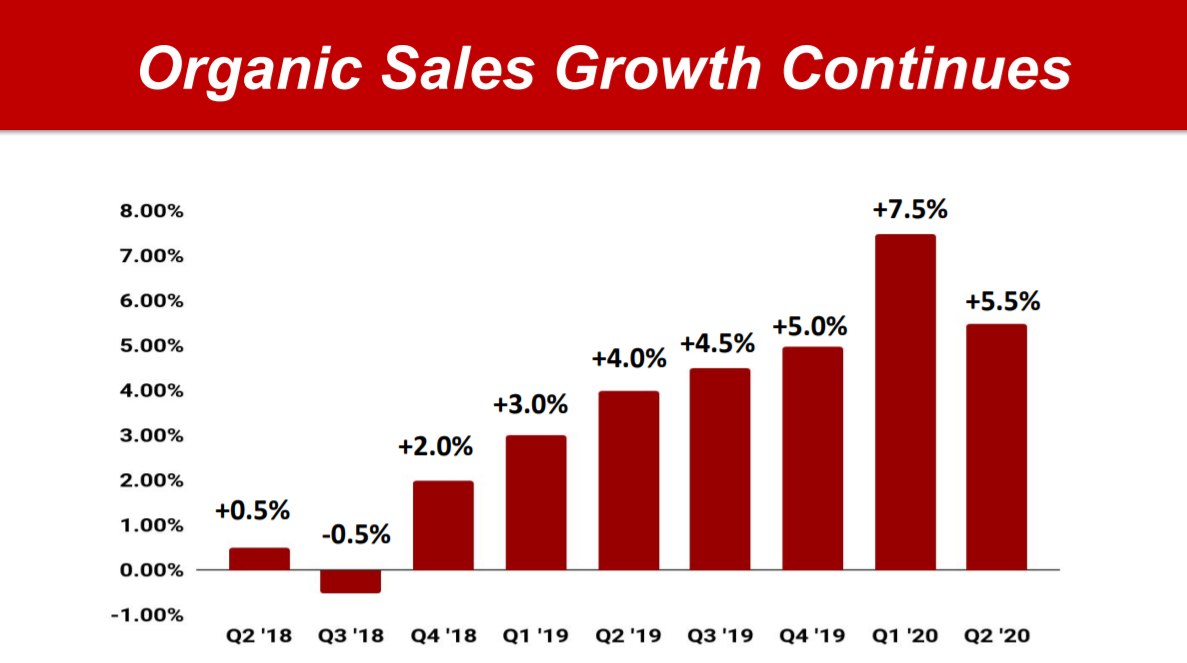

All of this has resulted in what we see below; very strong organic sales growth in recent years.

Source: Investor presentation, page 7

Colgate-Palmolive has had one quarter in the past nine where organic sales growth was below zero. That growth has accelerated in recent quarters, even prior to the pandemic. We see this driving much of the company’s growth in the coming years.

Colgate-Palmolive reported second quarter earnings on July 31st, and the company managed to beat very high expectations on both the top and bottom lines. Total revenue was up 0.5% from the prior year period, but organic sales impressed once again with a 5.5% gain year-over-year. Colgate-Palmolive saw higher volumes and higher pricing.

North American sales were strong due to stay-at-home conditions, but the company noted pantry-stocking appeared to be waning, indicating some measure of weakness in the back half of the year. Hill’s led the way with growth once more, as it has for some time.

Forex hurt the top line, but earnings-per-share rose two cents year-over-year to $0.74, handily beating consensus of $0.69. Management didn’t reinstate guidance due to uncertainty from COVID-19, but we expect $2.95 in earnings-per-share for this year.

Competitive Advantages & Recession Performance

Colgate-Palmolive’s competitive advantage is its extensive product catalog, as well as its extremely well-known brands. This has afforded the company size and scale globally that allows it to bring products to market quickly, and at favorable pricing.

Colgate-Palmolive’s recession record is extraordinary, having posted strong earnings gains during the Great Recession:

- 2007 earnings-per-share of $1.69

- 2008 earnings-per-share of $1.83 (8.3% increase)

- 2009 earnings-per-share of $2.19 (19.7% increase)

- 2010 earnings-per-share of $2.16 (-1.4% decline)

While earnings dipped very slightly in 2010, it is clear Colgate-Palmolive performs quite well during times of economic duress. Indeed, we expect a robust earnings increase this year, which contains a very sharp recession from COVID-19.

Colgate-Palmolive has managed to build a portfolio that not only holds up to recessions, but thrives during such periods.

Valuation & Expected Returns

We see Colgate-Palmolive posting fairly weak returns in the coming years, not due to fundamental weakness, but rather, because the stock has already priced much of that growth in.

We expect 6% earnings-per-share growth in the coming years, and the dividend is worth 2.2% annually at the current price and payout. However, shares trade today at 26.7 times this year’s expected earnings, which is well in excess of our fair value estimate of 21 times earnings. We therefore expect a nearly-5% headwind to total returns in the coming years from the valuation.

With this somewhat offsetting expected earnings growth and the dividend yield, total returns are expected to be just 3.4% for the next five years. Investors have bid up the stock as a response to pantry-stocking and the company’s very strong recession resilience, but that has made it unattractive.

The dividend is just 60% of earnings for this year, and we expect the payout ratio to remain around 60% for the foreseeable future. We expect the dividend to rise at about the same rate as earnings, and that investors will enjoy decades of further increases thanks to the very safe payout.

Final Thoughts

Colgate-Palmolive has a very impressive history of growing its portfolio over time, and with its recent focus on innovation, it has renewed its growth. We expect the company to build upon a strong 2020 performance in the coming years, and we see many years of dividend increases coming as well.

However, the stock is pricing in a lot of growth today, and with total projected annual returns under 4%, we rate Colgate-Palmolive a sell. The stock would once again be a buy, if and when it trades below fair value.

{kind=link}

{kind=link}

{kind=link}