Updated on January 13th, 2020 by Samuel Smith

Rising dividend income over time is a goal for most dividend growth investors. We believe the best way to do this is to focus on high-quality dividend growth stocks.

For the best-in-class dividend growth stocks, consider investing in the Dividend Aristocrats, a select group of 57 companies in the S&P 500 Index with 25+ consecutive years of dividend increases.

You can see a full downloadable spreadsheet of all 57 Dividend Aristocrats, along with several important financial metrics such as price-to-earnings ratios, by clicking on the link below:

We review all 57 Dividend Aristocrats each year, and the next stock in the 2020 edition is Cintas (CTAS). Cintas is a high-growth dividend stock. It has raised its dividend 36 years in a row, including a 24.4% increase for 2019.

Cintas raises its dividend each year, but it has a low current yield of just 0.9%. This is less than half the average dividend yield of the broader S&P 500 Index.

In addition, Cintas stock has an extremely high valuation. As a result, prospective investors should wait for a better price before buying Cintas.

Business Overview

Cintas Corporation started out in 1929, under the name Acme Industrial Laundry Company. It was founded by Richard “Doc” Farmer, who got his start collecting chemical-soaked rags from factories and cleaning them for a fee.

Doc Farmer’s grandson, Richard T. Farmer, joined the company in 1956 after graduating from college. After gaining enough experience, he left the family business to start Cintas in 1968.

Today, it is the largest company in its industry, generating annual revenue in excess of $7 billion.

Source: Investor Relations

It designs and manufactures corporate uniforms, entrance mats, restroom supplies, fire protection, and first aid products. The company has a large and diversified customer base, which includes more than 1 million businesses in North America, Latin America, Europe, and Asia.

Cintas is split up into two main businesses. The Uniform Rental segment is the largest business, representing more than 80% of annual revenue. It provides products and services to customers through the company’s local delivery routes. Cintas also has a first aid and safety services business, which provides products through its distribution network and local delivery routes.

Cintas is certainly a growth company, and has been for a long time. In the company’s fiscal 2020 second quarter, adjusted earnings-per-share rose by an impressive 29% over the comparable period last year. The company also enjoyed a 7% increase in total revenue thanks to broad-based growth, as well as continued margin expansion.

Going forward, we estimate that Cintas will be able to produce 8% earnings-per-share growth annually, continuing a long tradition of high rates of earnings growth.

Growth Prospects

Cintas has enjoyed strong growth for the past several years. It saw particularly high growth rates in the years following the Great Recession, when hiring picked up and the labor market recovered. This has led to the huge rally in Cintas stock since the market lows of 2009. As unemployment rates remain very low, Cintas is performing extremely well.

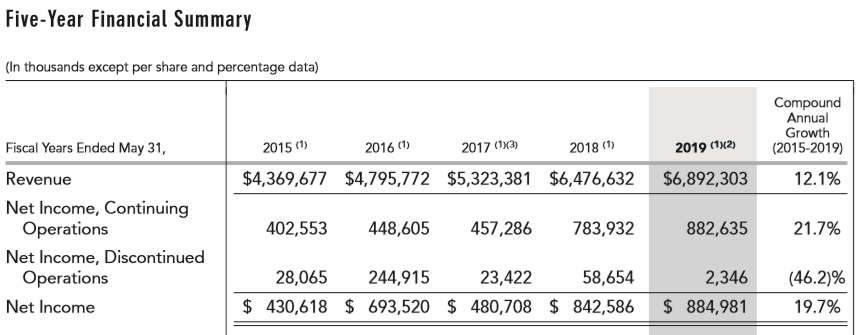

Cintas has generated excellent growth of revenue and net income over the past five years:

Source: 2019 Annual Report

The company continued to perform well to start fiscal 2020. After the Q2 earnings report, management boosted guidance to a midpoint of $8.7 in earnings-per-share for this year. Cintas also said revenue would be up ~6% this year to $7.3 billion, and margins would continue to expand. With the job market continuing to perform well and with a bright outlook, management is justifiably confident.

Cintas has a positive growth outlook moving forward. Catalysts for future growth include the very strong job market in the US as well as Cintas’ willingness and ability to purchase growth, as it did with G&K Services in 2017.

Cintas benefits from global economic growth. As companies grow and hire new employees, demand for service uniforms and related equipment rises. This is how Cintas has been able to produce such high growth rates over time and given the strong state of the U.S. labor market, Cintas’ near-term growth is all but assured.

Another growth catalyst for Cintas is its portfolio restructuring. The company has divested under-performing segments and has acquired companies in new areas, as management is willing to reshape its portfolio toward the best future opportunities.

For example, Cintas sold its interest in Shred-it International, for $578 million. This business was not meeting management’s expectations, and was not deemed critical to the future growth strategy of the company.

On the other hand, the G&K acquisition added nearly a billion dollars of annual revenue without shareholder dilution. In addition, the company is saving more than $100 million annually from synergies between the two companies and is providing Cintas with another strong growth catalyst.

The G&K purchase was a sizable one for Cintas so it may be some time before investors see another big acquisition, but Cintas certainly isn’t afraid to make bold moves to fuel the next leg of growth.

In total, we see 8% average annual earnings-per-share growth in the coming years for Cintas. Cintas doesn’t buy back enough stock to impact earnings-per-share growth, but revenue growth and margin expansion have been outstanding in recent years.

Competitive Advantages & Recession Performance

Cintas has a distinct operating advantage, which is its vast distribution network. Cintas has more than 11,000 local delivery routes, hundreds of operational facilities, and 11 distribution centers.

It is the largest company in its industry, which gives it market control. It would be very difficult for a new competitor to enter the market and try to disrupt Cintas’ business model, even more so after the G&K purchase. This helps keep competition at bay as Cintas has a highly entrenched customer base.

Its distribution capabilities and reputation for quality provide Cintas with high margins. So far this year, gross margins are in excess of 46% of revenue and operating margins are over 18% of revenue.

While Cintas is a high-growth business, it is also reliant on a healthy global economy. When the economy goes into recession, companies hire less and often reduce headcount. This results in reduced demand for the products Cintas manufactures. Cintas had a difficult time growing earnings-per-share, despite the fact that the recession officially ended in 2010.

The company’s earnings-per-share for 2008-2010 are shown below:

- 2007 earnings-per-share of $2.09

- 2008 earnings-per-share of $2.15 (2.9% increase)

- 2009 earnings-per-share of $1.83 (15% decline)

- 2010 earnings-per-share of $1.49 (19% decline)

As you can see, Cintas struggled during 2009 and 2010, with two consecutive years of double-digit earnings declines. This reflects how closely the profits of the business are tied to the condition of the economy. At the same time, Cintas remained profitable, which allowed it to continue increasing dividends each year. The company’s dividend also appears to be quite safe at current levels.

And, Cintas quickly emerged from the recession. The company grew earnings-per-share by 13% and 35% in 2011 and 2012, respectively. To be clear, the risk of recession in the near term is low, but shareholders should note that economic downturns are very unfriendly to Cintas’ earnings capabilities.

Valuation & Expected Returns

Based on forecasted earnings-per-share of $8.70 for fiscal 2020, Cintas stock trades for a price-to-earnings ratio of 27.8. This is a very high valuation against the broader market, as well as Cintas’ own historical valuations.

Cintas has had an average price-to-earnings ratio of 32, which means the stock is currently trading ~83% above its fair value. The stock has traded for such high valuations in the past, but these periods often preceded significant multiple contraction, which hurt shareholder returns.

If the stock were to return to our fair value estimate price-to-earnings ratio over the next five years, shares would decline by about 11% annually from multiple contraction. As a result, Cintas is extremely overvalued, and remains overvalued for us at any price above $152 per share. This would represent a price-to-earnings ratio of 17.5, on par with the company’s normalized valuation.

Given this extensive overvaluation, we expect negative total shareholder returns for the next half decade. Essentially, Cintas’ significant runway for growth has already been priced into the stock at the current price, as the sub-1% dividend yield and ~8% expected earnings-per-share growth will likely be entirely offset by the substantial annual expected headwind from multiple contraction.

Cintas’ valuation today, in other words, has priced in five years’ worth of growth, and we believe investors should avoid the stock as a result.

Final Thoughts

Cintas is a very strong company, with a high growth rate of earnings and dividends. However, due to the recent impressive rally in the stock price, Cintas now has a dangerously elevated valuation.

Another consequence of the huge share price increase in recent years is that the stock has a low dividend yield of under 1%.

While the company has a secure dividend payout with room for future dividend increases, the stock is simply overvalued. We rate it a sell despite its superior fundamentals simply because the valuation is so high.

If Cintas returns to a normalized valuation at or below our fair value estimate, it could once again earn a buy recommendation because of its strong growth and high-quality business.

{kind=link}

{kind=link}

{kind=link}