Updated on February 18th, 2022 by Felix Martinez

The Dividend Aristocrats are some of the best dividend growth stocks an investor will find. These are companies are in the S&P 500 Index, with 25+ consecutive years of dividend increases.

We believe the Dividend Aristocrats are among the highest-quality dividend growth stocks around. For this reason, we created a downloadable spreadsheet of all 66 Dividend Aristocrats, along with important metrics such as price-to-earnings ratios and dividend yields.

You can download the Excel sheet of all 66 Dividend Aristocrats by clicking the link below:

Each year, we review all of the Dividend Aristocrats. The next stock in the series is a consumer staple giant Church & Dwight Co., Inc. (CHD). Church & Dwight might not be as familiar as some of its consumer staple competitors as Procter & Gamble (PG), Clorox (CLX), or Colgate-Palmolive (CL); however, it has undoubtedly earned its place on the Dividend Aristocrats list.

Church & Dwight has now increased its dividend for an astounding 26 consecutive years. The Company’s dividend is also very safe, with a dividend payout ratio of 33%.

At the same time, Church & Dwight’s stock has experienced a multi-year rally in share price. As a consumer staple stock, it has benefited from the steady economic growth since the Great Recession ended. However, the stock appears to be overvalued at today’s price, which is why right now might not be the best time to buy Church & Dwight Co. stock.

Business Overview

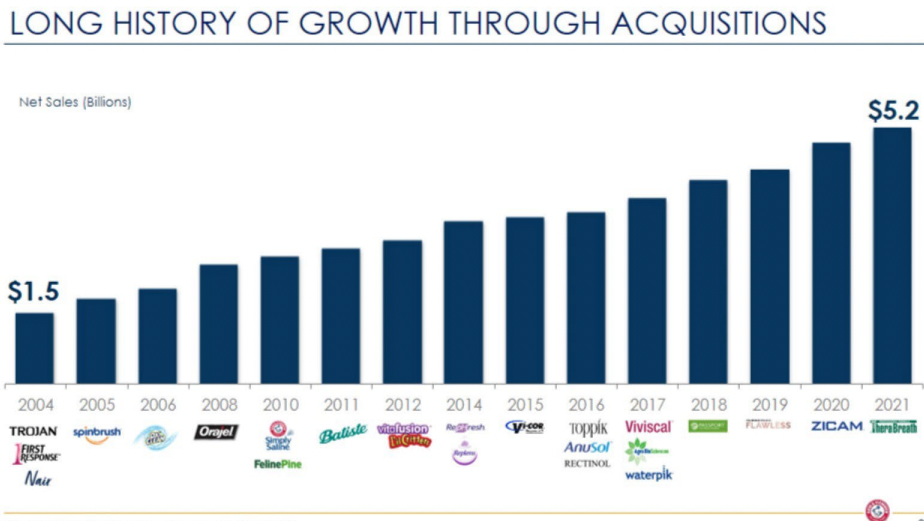

Church & Dwight is a diversified consumer staples company that manufactures and distributes products under several well-known names like Arm & Hammer, Trojan, OxiClean, Spinbrush, First Response, Waterpik, Nair, Orajel, and XTRA. The Company was founded in 1846, has increased its dividend for 26 consecutive years, and trades with a market capitalization of $23.4 billion on about $5.2 billion in annual revenue. For more than 100 years, Church & Dwight was a baking soda company operating with only the Arm & Hammer brand. However, since 2001, the Company has acquired 13 of its 14 “power brands.” Church & Dwight’s acquisitions of leading brands have diversified its reach across the household and personal care space. Also, Church & Dwight has paid quarterly dividends to shareholders for 121 consecutive years.

Source: Investor Presentation

On January 28th, 2022, the Company reported fourth-quarter earnings and full-year results for 2021. Results were slightly higher than consensus expectations on the top and bottom lines. Total revenue for the quarter came to $1.37 billion, up 5.4% year over year, and was $20 million ahead of expectations. This exceeded the Company’s outlook of 3% growth. The Company saw organic sales growth of 4.3%, which exceeded the Company’s outlook of 2%, driven by a favorable price and product mix. Net income grew by $8 million to $158.1 million, an increase of 5.3% compared to the fourth quarter of 2021. Earnings per share (EPS) in Q42021 was $0.64 per share, an 8.5% increase compared to the $0.59 reported EPS in Q4 2020.

For the full year, revenue grew from $4.9 billion in FY2020 to $5.2 billion last year. This is an increase of 6.1% year-over-year. Net income rose 5.4% to $ 827 million for the year from $785 million in FY2020. These growths were driven by a significant increase in consumer demand for many of its products throughout the year.

The Company also announced an increase in its dividend. The Company’s Board of Directors declared a 4% increase in the quarterly dividend from $0.2525 to $0.2625 per share, equivalent to an annual dividend of $1.05 per share. This raises the annual dividend payout from $248 million to approximately $255 million.

We expect CHD to earn $3.20 per share for 2022, an increase of 4%-8% compared to prior year-adjusted EPS, driven by operating income growth 10%+. Also, we expect a 6% annual EPS growth over the next five years, comprised mainly of revenue growth and share buybacks.

Growth Prospects

While 2020 was a challenging year for the global economy, due to the coronavirus pandemic, which weighed heavily on economic growth, Church & Dwight continued to generate steady profits. In 2021, the Company continued to grow its earnings, and the stock price continued to run higher, with a total return of 17.5% for the entire year of 2021.

The biggest growth driver for Church & Dwight will be continued organic sales growth and acquiring solid brands in the future. The 14 “power brands” made up 80% of sales and profits in 2021.

Source: Investor Presentation

Another growth driver for the Company is online. For example, 15% of net sales came from online shopping last year. This is a 2% increase in online sales compared to 2020.

Source: Investor Presentation

Competitive Advantages & Recession Performance

Church & Dwight’s competitive advantage comes from its willingness to execute acquisitions and growth in organic sales. This growth-by-acquisition strategy gives the Company an enduring opportunity to continue growing its business for the foreseeable future. CHD is also modestly recession-resistant. For example, Church & Dwight’s competitive advantages allow it to maintain consistent profitability each year, even during recessions.

Church & Dwight’s earnings-per-share during the Great Recession are below:

- 2007 earnings-per-share of $0.63

- 2008 earnings-per-share of $0.72 (13% increase)

- 2009 earnings-per-share of $0.87 22% increase)

- 2010 earnings-per-share of $0.99 (14% increase)

Durning the COVID-19 pandemic, earnings grew from $2.47 per share in 2019 to $2.83 per share in 2020. This represents an increase of 15% year-over-year.

Valuation & Expected Returns

Based on expected EPS of $3.20 for 2022, Church & Dwight’s stock trades for a price-to-earnings ratio of 30.3, using today’s stock price of ~$97. CHD held an average price-to-earnings ratio of 26.9 over the past ten years. Thus, we think that a fair earning multiple is 27.0. Consequently, based on its average valuation multiples, Church & Dwight’s stock appears to be overvalued.

If the company stock experiences a decline in the valuation multiple to our fair P/E of 27.0, it will reduce annual shareholder returns by 3.0% annually over the next five years.

Earnings growth and dividends will positively impact future returns. First, we expect the Company to grow earnings-per-share by 6% per year through 2027.

Lastly, CHD stock has a dividend yield of 1.1%. Putting it all together, a breakdown of our expected future returns is as follows:

- 6.0% expected earnings-per-share growth

- 1.1% dividend yield

- -3.0% negative return from valuation contraction

In this projection, total shareholder returns could reach 4.1% annualized through 2027. This is a modest expected rate of return for this Company.

Final Thoughts

Church & Dwight has many of the characteristics of a high-quality dividend investment. Most notably, the Company’s portfolio of brands allows it to grow its earnings through each stage of the economic cycle. Also, Church & Dwight shares its growth with its shareholders through consistent dividend increases. The Company’s growth-through-acquisition strategy is time-tested, and its management team has developed considerable expertise in scaling smaller brands through its existing infrastructure. Still, the Company’s valuation is unattractive. We forecast total returns accruing at just 4.1% annually, consisting of 6% earnings growth, the 1.1% dividend yield, and a sizable headwind from the valuation. Shares earn a hold rating.

{kind=link}

{kind=link}

{kind=link}