Published on August 1st, 2022, by Felix Martinez

There is no exact definition for blue chip stocks. We define it as a stock with at least ten consecutive years of dividend increases. We believe an established track record of annual dividend increases going back at least a decade shows a company’s ability to generate steady growth and raise its dividend, even in a recession.

As a result, we feel that blue chip stocks are among the safest dividend stocks investors can buy.

With all this in mind, we created a list of 350+ blue-chip stocks, which you can download by clicking below:

In addition to the Excel spreadsheet above, we will individually review the top 50 blue chip stocks today as ranked using expected total returns from the Sure Analysis Research Database.

In this article, we will analyze Walgreens Boots Alliance (WBA) as part of the 2022 Blue Chip Stocks In Focus series.

Business Overview

Walgreens Boots Alliance is the largest retail pharmacy in the United States and Europe. Through its flagship Walgreens business and other business ventures, the $34.24 billion market cap company has a presence in more than nine countries, employs more than 315,000 people, and has more than 13,000 stores in the U.S., Europe, and Latin America.

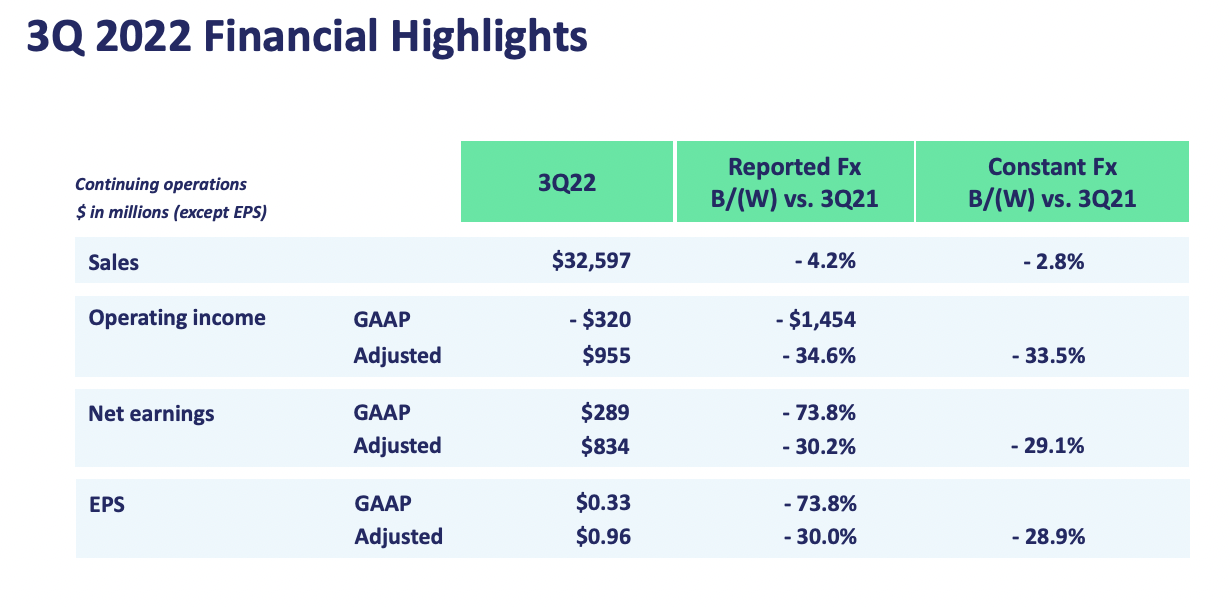

On June 30th, 2022, the company reported the third quarter and first nine months’ results for the fiscal year 2022. The company ends its fiscal year at the end of August of every year. In the quarter, operating loss from continuing operations decreased 4.2% from the same quarter a year ago to $32.6 million.

Net earnings decreased 73.8% to $289 million compared to $1.1 billion in the year-ago quarter. The decline reflects the opioid settlement with the State of Florida, a decrease in U.S. pharmacy operating results as it lapped prior-year peak COVID-19 vaccinations.

Earnings were also down by 73.% to $0.33 compared to EPS of $1.27 in the year-ago quarter. Adjusted EPS from continuing operations was $0.96, a decrease of 30.0% on a reported basis and 28.9% on a constant currency basis.

For the nine months of the fiscal year, sales are up 2% compared to the first nine months of 2021. Net earnings saw a significant increase of 148% versus 2021 net earnings for the nine months. Overall, earnings per share are up from $2.21 per share in 2021 nine months to $5.49 per share for the nine months of 2022.

Source: Investor Presentation

Growth Prospects

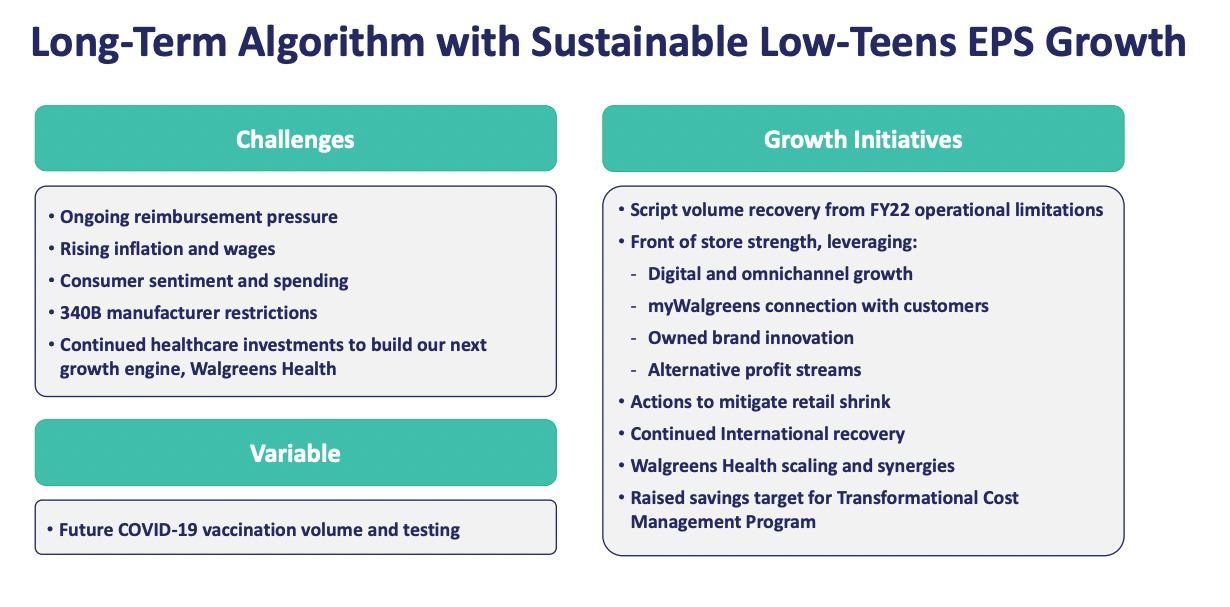

From 2011 through 2021, Walgreens grew earnings-per-share by 7.2% per annum. This was driven by a combination of factors, including solid top-line growth ($72 billion to $132 billion), a steady net profit margin, and a reduction in the number of shares outstanding. In 2020, earnings-per-share fell off dramatically, with the company posting a -21% decline, primarily due to the COVID-19 pandemic. The three factors of success in the past – revenue growth, steady margins, and a lower share count – were simultaneously challenged in the short term.

We expect the company revenue to grow 2% over the coming years. This will be driven by increased prescriptions in the pharmacy segment, the company’s omnichannel efforts, and targeted consumer advertisements contributing to front-end store growth.

We think the company will grow earnings at a modest rate of 3% annually for the next five years. This will give us estimated earnings of $6.20 per share for 2027.

Source: Investor Presentation

Competitive Advantages & Recession Performance

Walgreens’ competitive advantage lies in its vast scale and network in a significant and growing industry. The company also takes advantage of its partners with suppliers on preferred terms. For example, in 2013, Walgreens and prescription drug wholesaler AmerisourceBergen entered into a 10-year primary distribution agreement for branded and generic drugs, which has subsequently been extended through 2029.

Walgreens also did well well during the Great recession. As you see below, earnings did not fall significantly in 2008 or 2009. However, dining the COVID-19 pandemic, the company’s earnings dropped 21% year-over-year (YoY).

You can see a rundown of Walgreen’s earnings-per-share from 2007 to 2011 below:

- 2007 earnings-per-share of $2.03

- 2008 earnings-per-share of $2.12 (Increase 4% YoY)

- 2009 earnings-per-share of $2.02 (Decrease 5% YoY)

- 2010 earnings-per-share of $2.12 (Increase 5% YoY)

- 2011 earnings-per-share of $2.64 (Increase 25% YoY)

While earnings-per-share fell slightly in 2009, the company quickly recovered. By 2011, earnings-per-share were well above the 2007 level.

In addition, Walgreens has a solid balance sheet with ample cash, sufficient liquidity, and manageable debt levels.

Source: Investor Presentation

Valuation & Expected Returns

Over the past ten years, the company has traded with a PE average of 13.7x earnings. Over the past five years, the company’s average PE has been 11.6x earnings.

Currently, the company has a PE of 7.9x earnings. This gives the company a significant upside potential. For example, if the company were to revert back to its five year PE average, we can possibly see multiple expansions of 46.7%

Thus, we think the company is undervalued at today’s price. Overall, we expect that the company can return about 12.8% annually. Most of this return will come from the high dividend yield and multiple expansions.

Final Thoughts

Walgreens has proven to be an impressive company over the years. The dividend track history is ideal, and earnings growth has been stable. We anticipate the stock to offer a 12.8% average annual return over the next five years thanks to 3% earnings growth, a 4.8% starting yield, and a 6.0% valuation tailwind. We rate the stock as a buy, but we note that patience will be required due to the stock price pressure in the ongoing bear market.

The Blue Chips list is not the only way to quickly screen for stocks that regularly pay rising dividends.

- The Dividend Aristocrats: S&P 500 stocks with 25+ years of consecutive dividend increases.

- The High Yield Dividend Aristocrats List is comprised of the Dividend Aristocrats with the highest current yields.

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 44 stocks with 50+ years of consecutive dividend increases.

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The 20 Highest Yielding Monthly Dividend Stocks: Monthly dividend stocks with the highest current yields.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Complete List of Russell 2000 Stocks: arguably the world’s best-known benchmark for small-cap U.S. stocks.

- The Best DRIP Stocks: The top 15 Dividend Aristocrats with no-fee dividend reinvestment plans.

- The 2022 High ROIC Stocks List: The top 10 stocks with high returns on invested capital.

- The 2022 High Beta Stocks List: The 100 stocks in the S&P 500 Index with the highest beta.

- The 2022 Low Beta Stocks List: The 100 stocks in the S&P 500 Index with the lowest beta.

{kind=link}

{kind=link}

{kind=link}