The consumer staples category is littered with great dividend stocks. After all, staples are products that consumers need, and therefore, don’t tend to see the ebbs and flows in demand that more discretionary products do. That’s great from a dividend investor’s perspective, because that stability leads to highly predictable earnings, cash flow, and ability to pay a rising dividend.

It is little wonder, then, that many of the 350+ stocks in the list of Blue Chips are in the consumer staples category. Blue Chips are stocks that have at least 10 consecutive years of dividend increases.

The subject of this article, Tyson Foods (TSN), boasts an 11-year streak of consecutive dividend increases. While there are certainly consumer staples stocks with longer streaks, we find Tyson’s dividend ratings to be quite high, and it has an above-market current yield.

We’ve compiled a list of more than 350 similar stocks, which you can download by clicking below:

In addition to the list of Blue Chips, we are individually reviewing the top 50 Blue Chip stocks today as ranked using expected total returns from the Sure Analysis Research Database.

This installment of the 2022 Blue Chip Stocks In Focus series will take a look at Tyson.

Business Overview

Tyson is a food provider that operates worldwide. The company has four segments: Beef, Pork, Chicken, and Prepared Foods. Its primary business is processing live cattle, hogs, and chicken. Through this process it creates various cuts of meat, fully cooked meat, frozen meat, value-added chicken products, hides and more. In additions, it prepares various ready-to-eat products such as sandwiches, hamburgers, pepperoni, bacon, sausage, and more.

Tyson was founded in 1935, produces about $53 billion in annual revenue, and trades with a market cap of $31 billion.

Tyson’s second quarter earnings were released on May 9th, 2022, and easily beat expectations on both the top and bottom lines.

Total revenue was $13.1 billion, a 16% gain over the year-ago period. Beef led the way with a 24% revenue increase, but all four segments produced double-digit gains. Higher sales volumes drove increased revenue for beef and chicken, while pricing actions undertaken to combat cost inflation helped drive further revenue gains.

Source: Investor presentation, page 4

Adjusted operating income was $1.16 billion, up more than half year-over-year, while adjusted earnings-per-share was $2.29. That was up from $1.34 in the same period a year ago.

The company said the USDA forecasts flat demand for protein production this year, but Tyson is outperforming that and raised guidance. It now expects ~$53 billion in sales, up from ~$50 billion previously. Based upon this, we now expect to see $9.00 in adjusted earnings-per-share for the fiscal year.

Now, let’s take a look at the company’s prospects for future growth.

Growth Prospects

Tyson has done a tremendous job of growing earnings in the past decade. The company has averaged almost 17% earnings-per-share expansion annually in the past decade, with much of that growth coming since COVID hit.

We don’t see anything like that sort of rate of growth as sustainable, so we instead forecast 3% for the coming years. Tyson has lapped the pandemic-driven boom in sales and margins, so growth from this much higher base of earnings will be more difficult.

Source: Investor presentation, page 17

Guidance was raised with Q2 earnings, including a sizable increase to the sales forecast, and higher margins. That translates to profit growth, and we believe this record year of earnings will be challenging to grow from.

The company is grappling with flat-to-down volumes in much of its universe, so pricing action is creating the bulk of revenue gains. In addition, the company has undertaken some productivity initiatives that should help drive margins in the coming years.

Source: Investor presentation, page 7

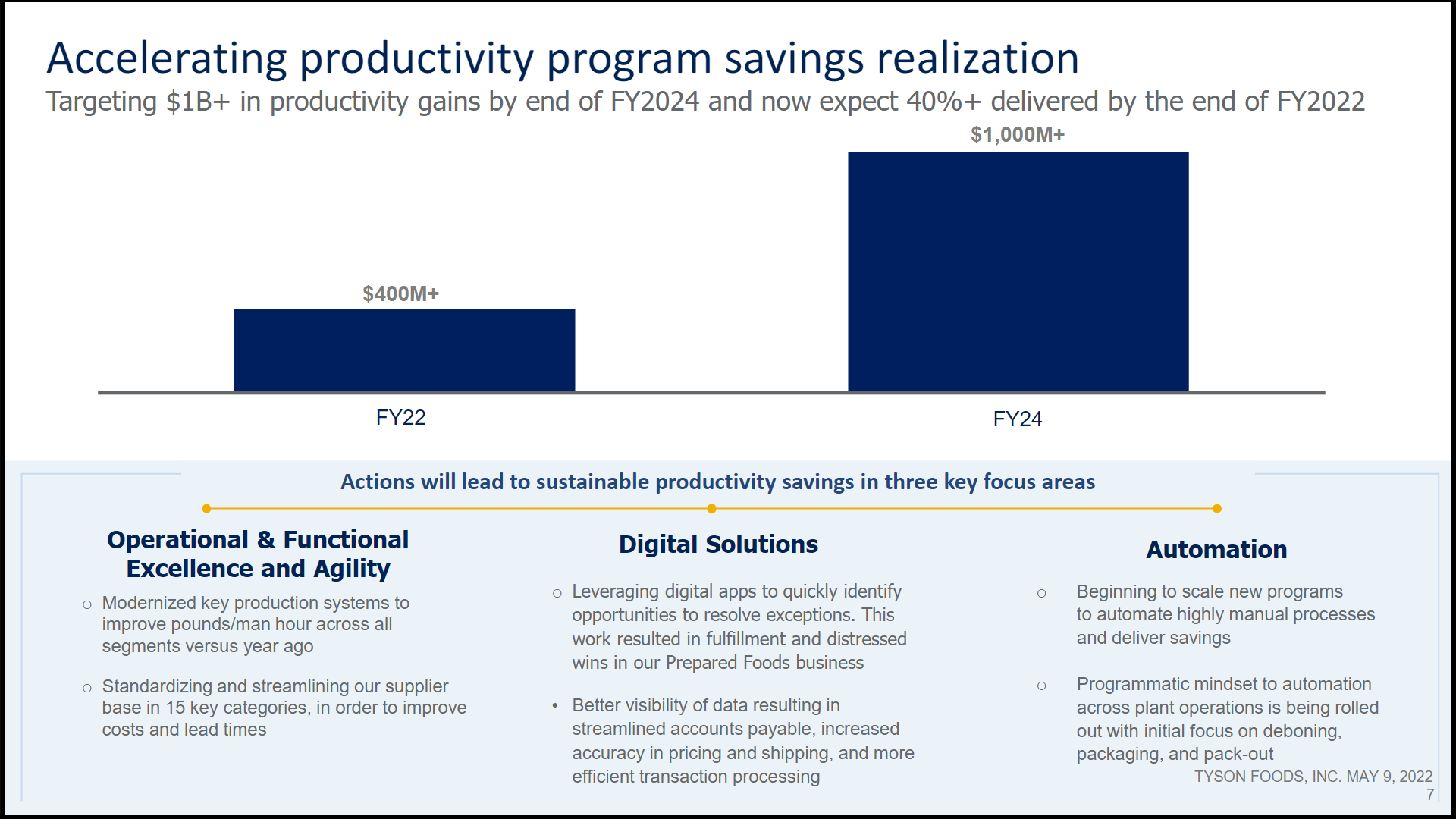

Tyson is targeting at least a billion dollars of productivity gains by the end of fiscal 2024, more than double the current level. Should this be achieved, it will aid in profitability, and therefore, EPS growth.

The company also buys back a modest amount of its own shares, with the second quarter seeing 6.2 million shares repurchased for $523 million. We see repurchases as incremental in terms of EPS growth.

Tyson’s dividend growth in the past decade has averaged more than 26% annually, so it’s been a terrific dividend growth story as well. We see 6% growth going forward, which puts the stock firmly into the dividend growth category.

Competitive Advantages & Recession Performance

Tyson’s competitive advantage stems primarily from its scale and brand recognition. As one of the oldest and largest players in what is a heavily commoditized industry, scale and brand recognition help it stand out from the crowd. We note that despite this, it is still a commodities producer, essentially, so advantages are difficult to come by.

Tyson struggled with earnings during the Great Recession, nearly posting a loss in one of those years. The company needs volume and revenue to leverage down fixed costs, so it’s possible Tyson will see lower earnings during a prolonged recession.

Even if that occurs, however, the dividend should be quite safe. The payout ratio for this year is projected to be just one-fifth of earnings, so there’s substantial room for future increases, as well as absorbing temporary declines in earnings.

Valuation & Expected Returns

The stock has generally traded around 11 to 12 times earnings in the past decade, with lower valuations during times of recession. Given the company is fighting cost inflation, as well as flat or lower volumes, we assess fair value at 10 times earnings today.

Shares trade for just under that value, meaning we would expect a fractional tailwind to total returns from a rising valuation in the years to come.

The current dividend yield is 2.1%, so combining the valuation tailwind and 3% earnings growth, we see ~6% total annual returns for Tyson shareholders over the next five years.

Final Thoughts

While Tyson does face some cyclicality in its earnings, it also has a double-digit streak of impressive dividend increases, very strong dividend safety, and respectable total returns. It also possesses scale and brand recognition in its field, and the combination of these factors makes it a Blue Chip stock to watch.

The list of Blue Chips is just one way to screen for high-quality dividend stocks.

- The Dividend Aristocrats: S&P 500 stocks with 25+ years of consecutive dividend increases.

- The High Yield Dividend Aristocrats List is comprised of the Dividend Aristocrats with the highest current yields.

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 44 stocks with 50+ years of consecutive dividend increases.

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The 20 Highest Yielding Monthly Dividend Stocks: Monthly dividend stocks with the highest current yields.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Complete List of Russell 2000 Stocks: arguably the world’s best-known benchmark for small-cap U.S. stocks.

- The Best DRIP Stocks: The top 15 Dividend Aristocrats with no-fee dividend reinvestment plans.

- The 2022 High ROIC Stocks List: The top 10 stocks with high returns on invested capital.

- The 2022 High Beta Stocks List: The 100 stocks in the S&P 500 Index with the highest beta.

- The 2022 Low Beta Stocks List: The 100 stocks in the S&P 500 Index with the lowest beta.

{kind=link}

{kind=link}

{kind=link}