Updated on March 11th, 2021, by Nikolaos Sismanis

Appaloosa Management was founded in 1993 by David Tepper and Jack Walton.

The firm used to operate as a junk bond investment company in the 1990s but evolved through the 2000s to become a more diversified hedge fund.

It has been one of the most successful hedge funds by specializing in public equity and fixed income markets around the world, delivering jaw-dropping returns to its institutional investors during times of distress.

As of its last 13F filing, the fund had ~$6.6 billion in managed 13F securities under management, a 17.8% increase from its previous quarter amid higher capital allocation in its public-equity holdings, possibly due to acquiring more clients.

Investors following the company’s 13F filings over the last 3 years (from mid-February 2018 through mid-February 2021) would have generated annualized total returns of 11.9%. For comparison, the S&P 500 ETF (SPY) generated annualized total returns of 12.5% over the same time period.

Note: 13F filing performance is different than fund performance. See how we calculate 13F filing performance here.

Click the link below to download an Excel spreadsheet with metrics that matter of Appaloosa Management’s current 13F equity holdings:

Keep reading this article to learn more about Appaloosa Management.

Table Of Contents

- Introduction & 13F Spreadsheet Download

- David Tepper

- Appaloosa Management’s New Buys & Sells

- Appaloosa Management’s Current Major Investments

- Final Thoughts

David Tepper

Little can be said about Appaloosa Management without mentioning its legendary manager David Tepper. Mr. Tepper has been one of Wall Street’s highest-paid hedge fund managers of the past decade, delivering market-beating returns during recessionary times. His net worth is currently around $12.7 billion. His fortune was made through Appaloosa, having the majority of his assets attached to the fund. Mr. Tepper has created most of his and Appaloosa’s value by navigating the fund’s allocations during times of distress.

In 2001, for example, when the market was suffering massive losses amid the dot com bubble, Mr. Tepper generated a 61% return by focusing on distressed bonds. During the Great Financial Crisis, he embraced the “buy when there is blood in the streets” mentality by purchasing distressed financial stocks. While everybody else was dumping their shares, Tepper was scooping up shares, including his famous play of buying Bank of America (BAC) shares for $3 each as well as AIG’s debt.

His bold bets paid off massively. From 2009 to 2010, the fund’s assets under management grew from $5 billion to $12 billion. Around $4 billion of these gains were added to Mr. Tepper’s net worth, making him the highest earner of the recession and forming the majority of his wealth.

Last year, Mr. Tepper announced his retirement to pursue owning the Carolina Panthers football team, which he bought in 2018 for a record $2.3 billion. A portion of Appaloosa’s assets left the fund; hence its current reduced AUM of $6.6 billion.

Appaloosa Management’s New Buys & Sells

During its latest 13F filing, Appaloosa Management executed the following notable portfolio adjustments:

New Buys:

Occidental Petroleum (OXY): Occidental’s new stake just became a ~3% portfolio position as of this quarter, with the fund purchasing shares at prices between ~$8.90 and ~$21.30. Occidental currently trades above $30/share.

Qualcomm (QCOM): Qualcomm’s new stake implies a ~1.3% portfolio position as of this quarter, with the fund buying shares between ~$116 and ~$159. Qualcomm currently trades at ~$125.

Fun fact: Qualcomm is back in the portfolio after a quarter’s gap. It is a frequently traded stock in Appaloosa’s portfolio.

Appaloosa also initiated stakes in the following securities, though in small amounts:Macy’s Inc. (M), CarMax Inc. (KMX), Kohl’s Corp (KSS), Enterprise Products Partners (EPD), Alliance Data Systems (ADS), EQT Corp (EQT), Freeport-McMoRan (FCX), MPLX LP (MPLX), Magellan Midstream (MMP), and Kinder Morgan (KMI)

While these investments were not very significant in size, we can clearly tell that Appaloosa favors retailers and midstream companies, which were those most affected by the COVID-19 pandemic. The investment management likely sees these securities still quite undervalued, despite many of them significantly rebounding since their initial nosedive around this time a year ago.

New Sells:

AT&T Inc. (T): AT&T was a ~2% position initiated in Q2-2020 at prices between $28 and $33. The fund sold ~50% of the position last quarter at prices between ~$28 and ~$31. The disposal this quarter was at prices between $26.50 and $31.50. The Dividend Aristocrat did not increase its DPS, as usual, this year, though it still has several quarters to do so before losing its Dividend Aristocrat status.

Additionally, Altria Group (MO) and Boston Scientific (BSX) were also eliminated during the quarter. They were quite meager stakes.

Appaloosa Management’s Current Major Investments

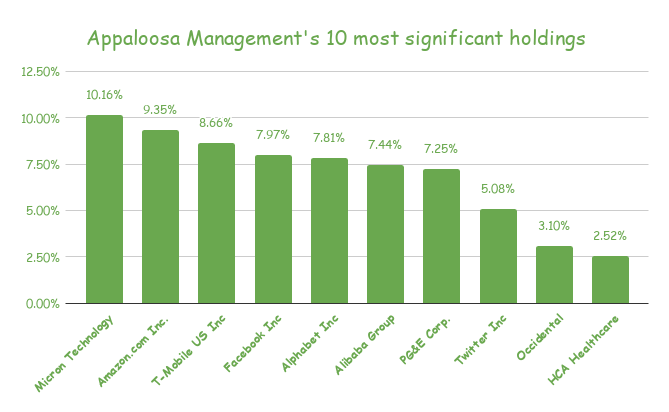

Appaloosa Management’s long-term strategy has focused on concentrated investment positions with multi-bagger potential. This investment philosophy seems to be the case well after Mr. Tapper’s departure, as the fund’s nearly $6.6 billion-worth public equity portfolio consists of only 35 stocks, with the top 5 accounting for around 44% of its total holdings.

Source: 13F Filings, Author

The fund’s 10 largest investments are the following:

Micron Technology (MU)

Despite Appaloosa trimming its Micron Technology stake by 34%, the company is currently the fund’s biggest holding, accounting for around 10.2% of its public equity investments. This is mainly due to the stock’s non-stop rally, which continued in Q4 as well. The stock has experienced a spectacular rally over the past 4 years, as the demand for its semiconductors has been explosive. Analysts expect the company’s earnings to snowball in the medium-term. While the stock is considered speculative, its robust profitability over the last several years has proven bears and short-sellers wrong. Many had predicted that the company’s top & bottom line would suffer due to the pandemic. However, Micron posted a robust FY2020 net income of $2.69 billion. The company is expected to produce FY2021 EPS of $4.66, implying a forward P/E of ~20, which indeed implies a relatively expensive multiple for a company in the semiconductor industry.

Amazon (AMZN)

Jeff Bezos’s e-commerce behemoth used to take up nearly ⅓ of Appaloosa’s at a couple of quarters earlier. With the fund’s traditional strategy of concentration, management’s faith placement in Amazon has been typical amongst multiple funds as of late. The company is taking over the world and seems unstoppable both in terms of its physical and digital infrastructure capabilities.

Mr. Jeff Bezos plans to have the company undergo another investment cycle and avoid maximizing profitability once again in the medium term, which is just another testament to Amazon’s long-term perspective. The e-commerce giant now accounts for around 9.4% of Appaloosa’s holdings. The fund seems to remain quite confident in Amazon, increasing its equity stake by 39% during the most recent quarter.

T-Mobile (TMUS)

Appaloosa trimmed its TMUS stake by 5% and while also ditching its AT&T stake completely, as mentioned earlier, clearly moving away from the telecom giants.

With T-Mobile recently acquiring Sprint, the company should be able to actively compete with AT&T and Verizon. As a result of the synergies to be unlocked, the company should undergo a growth phase over the next few quarters. The company reported record Q4 revenues of $20.34 billion and net income of $750 million. While the stock’s current P/E of around 48 may seem like a hefty one, analysts expect the company to leverage its economies of scale amid its recent merger to grow its profitability massively in the medium term.

The stock currently occupies around 8.7% of Appaloosa’s portfolio.

Facebook (FB) & Alphabet (GOOGL)

Appaloosa increased its Facebook stake by around 13%, placing the stock in its fourth-largest position. Shares account for around 8% of the fund’s holdings. With growing financials, one of Wall St.’s healthiest balance sheets, and the best platform for advertisers to utilize, Facebook remains an attractive pick at a reasonable valuation.

The company reported an all-time high bottom line of $11.22 billion and is only trading at 22 times its underlying earnings, despite its rapid growth. With its ARPU (average revenue per user) proliferating, we are confident that Facebook’s financials will continue expanding rapidly, and the stock will have to eventually reflect the company’s underlying qualities.

Appaloosa also trimmed its position in Alphabet by around 1% as well, likely in efforts to diversify its portfolio against tech’s never-ending rally. The company is another example of showcasing world-class financials and robust growth. Further, the stock trades at an attractive valuation of around 30 times the company’s forward earnings, which makes it one of the more reasonably-priced technology picks as of lately. Alphabet’s growth seems to be re-accelerating as well, with its latest results posting revenue growth of 23.5%.

It is currently Appaloosa’s fifth-largest holding or around 7.8% of its public-equity holdings.

Alibaba Group (BABA)

Alibaba was Appaloosa’s largest equity holding 2 quarters ago after management had increased the fund’s stake by a massive 49%. In this quarter, Alibaba’s stake was slashed by 14%. Shares have declined significantly over the past quarter, despite the company posting record revenues and profits.

With an average estimated buying price below $200, Appaloosa has profited nicely off of its consistent $BABA stake increases (and sales). Shares are currently trading around $228, despite trading near all-time highs, at around $275/shares in the previous quarter. This is most likely due to the risks involved with Chinese equities, including the potential for a NASDAQ delisting.

PG&E Corporation (PGE)

PG&E was Appaloosa’s largest holding in its previous filings. The hedge fund slashed its position by 47%during this quarter, most likely due to shares surging during Q4, netting Appaloosa decent profits in a short period of time. With the rest of its stake in PCG, Appaloosa likely aims to benefit from the company’s currently depressed situation, facing a potential bankruptcy amid California’s wildfires. The fund’s average buying point seems to be around $10.82, which indicates considerable short-term gains at the stock’s current price of $11.32. Should the company survive its current headwinds, Appaloosa is likely to have made one of its most successful distressed equity investments, buying shares near their 50-year lows. Still, the company remains very risky, has suspended dividends as per its current situation, and it is unlikely that shareholders will see any kind of tangible returns in the medium term. Hence retail investors should be very aware of the underlying concerns before allocating capital to the company.

Twitter Inc (TWTR)

Jack Dorsey’s social media company occupies the eighth-largest position of Appaloosa’s portfolio with a nearly $350 million stake. The company has struggled to deliver consistent, investors-friendly financial results over the years, despite its success as a social media platform.

However, with its recent plans to develop a subscription service, investor interest has been reignited over the potential of recurring revenues flowing into the social media firm.

Appaloosa trimmed increased its stake by 1% during the quarter, remaining confident in Twitter’s long-term prospects. Despite its inconsistencies, the company delivered a substantial net income of around $222 million in Q4.

It’s worth noting that Twitter’s monetization issues may continue to persist, leaving current investors to future potential valuation risks. For those looking to get exposure to the social media space, Facebook still remains the best option, in our view.

Occidental Petroleum Corporation (OXY) & HCA Healthcare, Inc. (HCA)

Last but not least, Appaloosa’s ninth and tenth largest holdings are both new entries in this list, accounting for around 3.1% and 2.5% of its portfolio, respectively. Occidental, along with the various other new stakes that the fund initiated during the quarter, indicated that the Appaloosa is likely becoming bullish on the energy sector. The company has essentially suspended its dividend at this point as it recovers from the adverse effects of the ongoing pandemic. It’s unlikely that investors will see any significant capital returns back at this point, with all 4 of its previous quarters resulting in net losses.

Finally, the fund increased its position in HCA by 6% to a $174 million stake. Appaloosa owns only three stocks operating in the healthcare sector, with HCA being the largest one. The medical care facilities provider posted resilient results during FY2020, and while it did cut its dividend during the year to remain prudent, it reinstated as of the past couple of quarters. The stock currently trades at just over 14.5 times its forward earnings, being quite fairly priced considering its long-term growth prospects and recession-proof business model.

Final Thoughts

Appaloosa Management has had a prosperous past, with multiple achievements under Mr. Tepper’s leadership. The firm has spoiled its investors with jaw-dropping returns during adverse economic times. Mr. Tepper’s departure marks a new era for the fund.

While the firm’s public holdings have slightly lagged the market over the past three years, it’s still early to judge, as the firm could once again shine during a potential future recession.

{kind=link}

{kind=link}

{kind=link}