Updated on May 20th, 2020 by Josh Arnold

Real Estate Investment Trusts have a lot to offer investors who desire higher levels of investment income, such as retirees. For instance, Gladstone Commercial Corporation (GOOD) is a REIT with a current dividend yield of 7.8%.

That makes it one of about 200 stocks in our coverage universe with a 5%+ dividend yield. You can see the full list of 5%+ yielding stocks by clicking here.

Gladstone Commercial appears to be an attractive dividend stock, especially considering the available alternatives. The S&P 500 Index, on average, has about a ~2% dividend yield. Plus, Gladstone Commercial is one of only 57 stocks that pays its dividend each month.

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter like dividend yield and payout ratio) by clicking on the link below:

However, Gladstone Commercial’s dividend is far from guaranteed. Its payout ratio is nearly 100%, leaving little room for error when it comes to maintaining the dividend.

This article will discuss the trust’s business model and financial performance, and why its dividend may be riskier than meets the eye.

Business Overview

Gladstone Commercial invests primarily in single-tenant, and anchored multi-tenant net leased assets. It owns 15.1 million square feet of office and industrial real estate in the U.S.

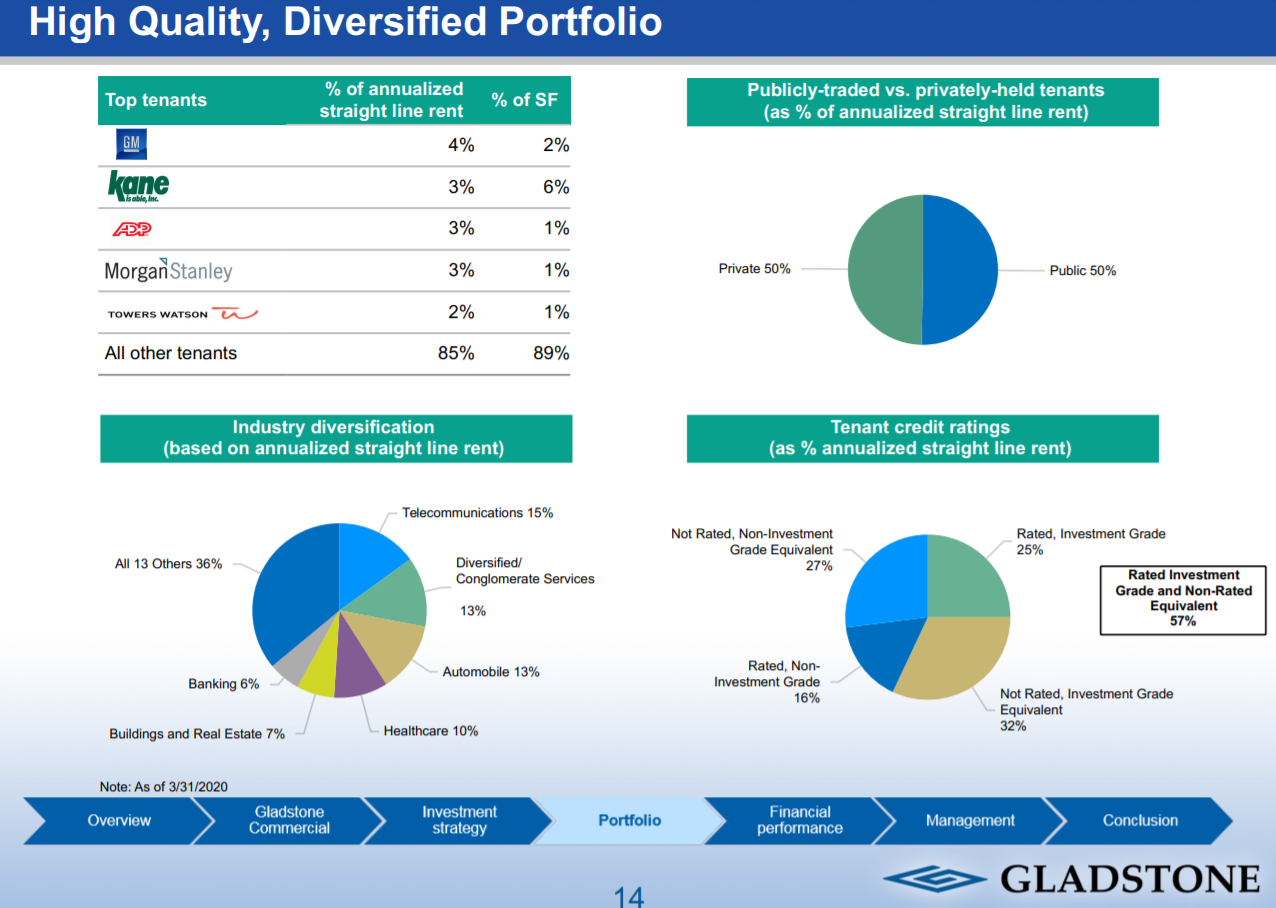

Gladstone Commercial has a very diversified portfolio. As of the end of March, the trust’s portfolio consisted of 101 properties in 24 states, leased to a highly diversified tenant group, as seen below.

{kind=link}

Source: Q1 investor presentation, page 14

The trust’s portfolio is typically geared toward long-term agreements. Gladstone Commercial’s average remaining lease term is 7.5 years.

In addition, Gladstone Commercial enjoys high occupancy rates, including a current rate of 96.6%. Impressively, occupancy has never fallen below 96% since the trust’s IPO in 2003.

Approximately 57% of Gladstone Commercial’s tenants are rated investment grade or are the non-rated investment grade equivalent. This contributes to a high-quality portfolio of tenants that should weather minor economic downturns quite well, and preserve Gladstone Commercial’s rent streams.

The trust has generated impressive revenue growth in the past, but growth of the bottom line has leveled off lately. This creates some level of uncertainty with the distribution’s safety.

Growth Prospects

Gladstone Commercial’s first quarter results showed funds from operation, or FFO, of $0.40 per share, which is in line with the prior year’s Q1, as well as most of the trust’s quarters for the past couple of years.

The trust has had a difficult time growing in recent years, owed to an ever-expanding share count and rising operating costs.

{kind=link}

Source: Q1 investor presentation, page 16

This isn’t a new problem by any means, as the trust has struggled to produce any sort of meaningful FFO-per-share expansion in the past handful of years. After peaking at $1.80 in 2014, FFO-per-share fell to $1.54 in 2015 and last year, rose only to $1.55. We expect a similar level of FFO-per-share for this year after Q1’s showing of $0.40.

Declines occurred despite total assets rising by nearly half, and revenue that rose similarly. The trust’s higher share count over time, which has tripled in the past decade, along with higher operating expenses, have collectively derailed earnings growth.

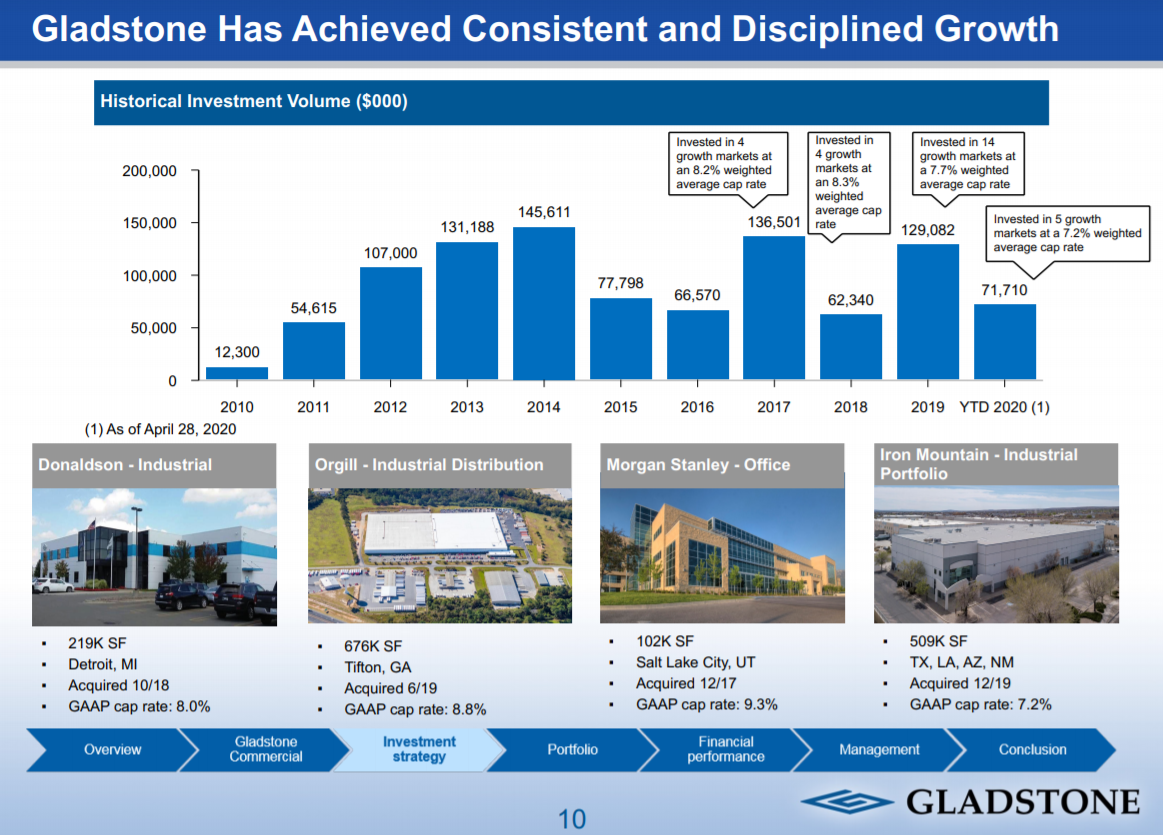

Gladstone Commercial continues to invest heavily in new properties, as seen in the image below.

{kind=link}

Source: Q1 investor presentation, page 10

The trust has invested an average of nearly $100 million annually in new properties since 2011. Compared to the trust’s current market capitalization of $540 million, that is a significant level of investment on an annual basis.

Gladstone Commercial divests non-core properties to fund part of these investments, but it also issues shares on a regular basis, as mentioned above. That has crimped FFO-per-share growth, and given that the trust doesn’t appear to be changing its strategy any time soon, we expect that to continue.

In total, while we expect Gladstone Commercial can at least maintain ~$1.50 in FFO-per-share annually – with potential growth rates in the low-single-digits – we think it will struggle to produce much more than that.

Given where the distribution is today, that could present a problem as the trust’s payout ratio is very close to 100%. However, despite the favorable fundamentals of the trust’s portfolio, its headwinds to earnings growth (dilution and operating expenses) are still very much present.

Dividend Analysis

Gladstone Commercial has a current monthly dividend payment of $0.12515 per share. On an annualized basis, the dividend payment is $1.5018 per share, good for a 7.8% dividend yield.

The distribution had been stagnant at $0.125 per share monthly since January of 2008, reflecting the struggles the trust has had with respect to growth. However, the distribution received a fractional raise earlier in 2020 to the new level of $0.12515 cents per share monthly.

To its credit, Gladstone Commercial has paid monthly dividends for more than 15 consecutive years, an impressive track record of consistent payouts, although the distribution has been basically flat for more than a decade.

Since Gladstone Commercial’s 2003 initial public offering, the trust has not missed a distribution, nor has it reduced the distribution at any time, which is very impressive for a REIT given the wide array of economic conditions that have existed in this time frame.

While we note that a downturn could put Gladstone’s dividend at risk – such as the present downturn – we also note that earnings are holding up very nicely thus far.

Another important consideration when buying dividend stocks is balance sheet strength.

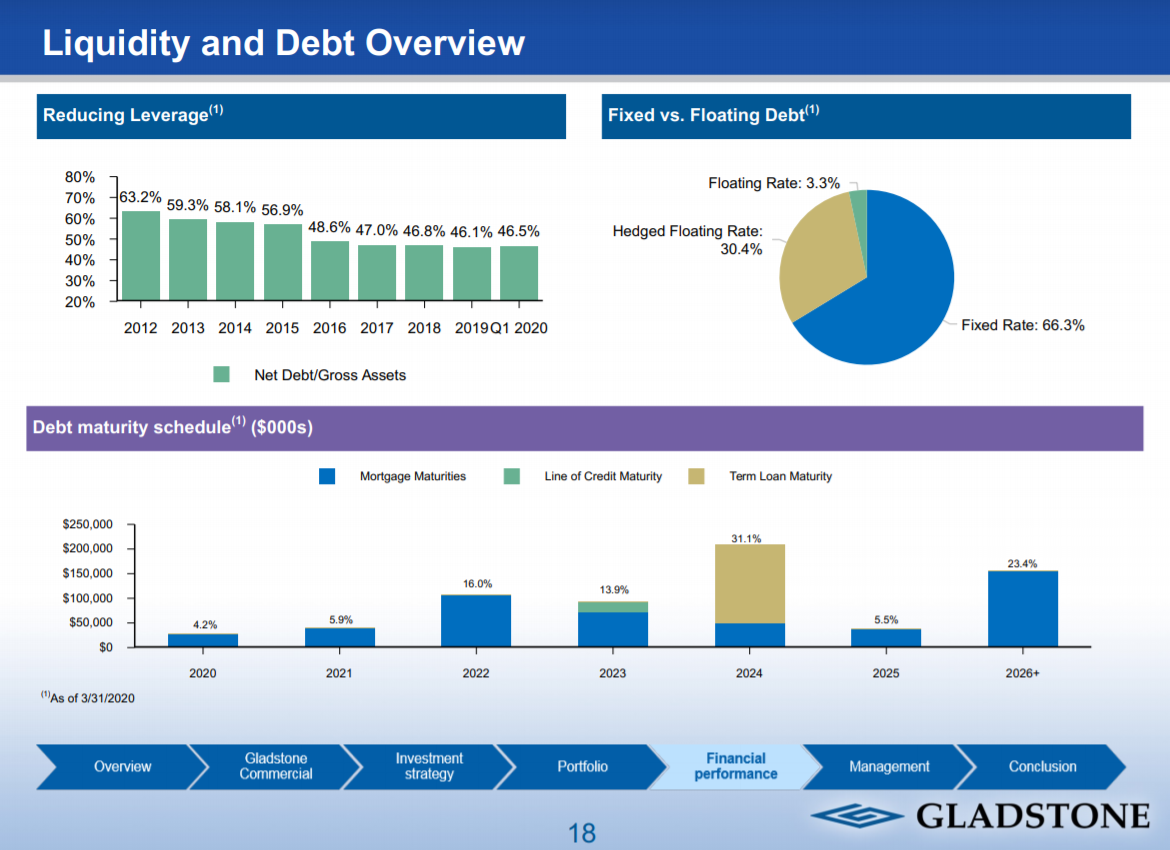

Too much debt can jeopardize a trust’s dividends. On a positive note, Gladstone Commercial has worked to significantly reduce its leverage over the past several years, and now has a balanced maturity schedule.

{kind=link}

Source: Q1 investor presentation, page 18

Approximately two-thirds of Gladstone Commercial’s debt is fixed-rate, which could help mitigate the impact of volatile interest rates.

In addition, large maturities are a few years away, meaning the trust has time to generate cash to pay them off, or find better ways to refinance them.

Still, there is not much room for error because the trust maintains a high payout ratio. Last year’s FFO-per-share of $1.44 didn’t quite cover the $1.50 payout. We see FFO coming very close to the payout this year, with either a small surplus or deficit possible.

This means there is very little wiggle room for Gladstone Commercial’s FFO when it comes to covering the distribution.

If the trust’s fundamentals deteriorate over the next few years, there is a chance it may not be able to sustain its dividend at the current level. We see this as the principal risk of owning Gladstone Commercial today, but also note that the trust has proven willing and able to issue new shares to pay the distribution in the past when there was an FFO deficit.

Final Thoughts

Gladstone Commercial’s very high dividend yield is attractive and appears to be sustainable, at least in the near-term, given the trust’s current FFO generation. The trust enjoys exceedingly high occupancy and strong rental rates as well. But given the ~100% payout ratio, we still have concerns about the dividend’s safety.

As a result, investors will need to monitor the trust’s results closely to make sure FFO does not decline much from present levels. Indeed, even a modest decline could jeopardize the dividend.

Investors should carefully weigh the trust’s risks before investing, as the very high yield is due in part to the risk of a cut thanks to current economic conditions. Gladstone’s yield is attractive, but it carries an elevated risk of a cut in the coming years, particularly if the current recession is worse than expected or drags on for a prolonged period.