GreenWood Investors 3Q21 Commentary: Defense, Offense & Conviction

GreenWood Investors commentary for the third quarter ended September 2021, titled, “Defense, Offense & Conviction.”

Q3 2021 hedge fund letters, conferences and more

When Defense Misfires

“Offense wins games. Defense wins championships.”

This past quarter, much of my curiosity has been focused on the differences between offense and defense. Given I’ve spent little time watching team sports, it’s been an interesting exploration. As my mind was occupied by defining an offensive playbook for our two coinvestments, we took our eyes off the ball of our protective, defense-oriented portfolio activities. The performance in the quarter was impacted by a 4% headwind generated by one particular short, which was the primary reason our fund underperformed indices in the quarter. While it was a painful lesson, we immediately evolved our short process in order to prevent our defensive measures from ever hurting our performance to such an extent going forward.

Cutting to the chase, the performance in the quarter for the Global Micro Fund was -7.7% net (+30.5% YTD), and this compares to our benchmark MSCI ACWI index returning -1.1% in the quarter (+11.5% YTD). Without any FX headwinds, euro-denominated Luxembourg fund returned -3.3% net (+39.4% YTD). Separate account composites had similar returns, as Global Micro strategy returned -8.1% net (+15.0% YTD) and our longest-running and long-only Traditional accounts returned -6.8% net (16.5% YTD). The Builders Fund I returned -5.2% net in the quarter (+84.5% YTD) driven partially by foreign exchange. Builders Fund II, which was launched in the quarter, returned +3.0% net (+3.0% YTD).

Aside from the one short mentioned, our returns were also impacted by corrections at Superdry PLC (LON:SDRY) and Peloton Interactive Inc (NASDAQ:PTON), each taking away roughly 2% from our performance in the quarter. They are both experiencing very different situations right now in the aftermath of Covid, but both are pressing their offense strategies with increased vigor.

We remain undeterred with Superdry despite popular skepticism on the brand’s turnaround. Such perspectives look mismatched with a reinvigorated influencer strategy targeting a whole new generation, which have just driven same-store-sales to positive territory on a two-year stack. This is ahead of a pivotal autumn-winter season, when its jackets, coats and sweaters have traditionally shined. Having missed last winter due to Covid, we are excited to see the new product resonate with an entirely new base of consumers. We recently followed the Chairman and CEO’s insider buys, and purchased more shares on weakness. We continue to be encouraged by the progress made; and for a slightly longer discussion on where our thoughts are on Superdry, click here to see a tweet thread.

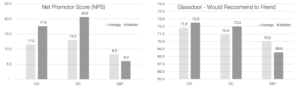

Peloton has experienced a round trip of home workout demand back to pre-covid levels. Thus, while it is launching new products and new geographies, and retains an industry-leading engaged base of 6.2 million exercisers with low monthly subscription churn, this position will have to return to old fashioned marketing to continue on its path towards its incredibly ambitious goal of impacting 100 million users’s fitness routines every month.. With its customer satisfaction, as measured by the Net Promotor Score, remaining one of the highest, if not the highest, in the world, we would not bet against this heavily engaged cult of growing endorphin-filled users. We believe the company still has a very significant market opportunity to both attack and define.

Revisiting The Defense Playbook

“Rule No.1: Never lose money. Rule No.2: Never forget rule No.1.” Warren Buffett

Stretching the offense and defense analogies over to investing, this past year has rewarded risk-taking (offensive) strategies, particularly those that are furthest out on the risk curve. But over the long-term, value-oriented investing wins the championship. That means taking a conservative underwriting approach to investment opportunities and maintaining a defensive posture when everyone else is doing the opposite. In our opinion, that also means running a short book, which allow us to remain opportunistic in periods of greater stress. It is not a good time to be reducing a defensive posture, in our opinion.

Over the first 11 years of GreenWood’s existence, we have almost never been idea-constrained. Rather, we have been only constrained by the capacity we have to analyze the large opportunity set. That has typically meant, aside from the earliest years, we have had minimal cash left over. Given we have gravitated towards misunderstood assets and areas neglected by robotic index funds, not only does this portfolio tend to not carry a large cash balance, but it has exhibited more volatility than an index.

Accordingly, carrying a short book is essential for us to be able to remain opportunistic in periods of stress. And quite frankly, our defense track record could use some improvement. While this defensive posture paid off in 2008, 2011, and 2018, we had few opportunistic shorts going into 2016 and 2020, right when we needed them. I’m personally committed to improving on that 3-2 market defense track record. I’m also committed to lowering any significant portfolio tilt towards specific factors, as our fundamental research capabilities are not able to be matched on a macroeconomic scale. There are too many factors and estimates to know anything on a large scale with any degree of certainty. For us, conviction is the most important function of an asset manager.

It was with that intention we have been carrying a full short book ever since late 2020. And that short book largely paid off over the first half of this year, as the current environment has proved to be fertile in finding over-valued, value-less businesses. In fact, most of these shorts underperformed the market so quickly and so dramatically, that short book turnover caused Chris and I to run on a faster and faster treadmill throughout this year.

When we found the short that ended up causing us so much pain in the quarter, it sounded too good to be true. It was a perfect offset to some of our chunkier portfolio factor exposures, but even more, it became clear this was not only a terrible business model, but it was likely a fraud. As Chris and I dug further into the business, there was a never-ending string of yarn that we kept pulling, and the more we pulled, the more damning the evidence was on the founder, company and target markets.

In that excited process, we failed to appreciate the risk posed by the meme-trading phenomenon, in the assumption that an Italian company was unlikely to get caught up in the retail trading frenzy that has generated so many distortions elsewhere. Bypassing that debate proved to be our mistake, as the less liquid nature of the stock meant that it was more easily manipulated higher for a few months. As it was getting squeezed, I took action to eliminate that portfolio risk, even knowing that the stock would eventually go to zero. And in the wake of that experience, we also exited other shorts that had largely run their course, but that posed some possible retail trading risk.

In our post-mortems, that are published on our investors-only research area, we identified one of the problems we were trying to solve for was the treadmill we found ourselves on. Because each piece of incremental evidence made it more and more compelling, we actually didn’t pause to have a proper bull-bear debate, which is what we have done for every other position. We had put too much pressure on ourselves to maintain a timely short book, and in many ways that papered over the obvious truth that the borrow was hard to obtain and liquidity was not accommodative. We revised our ranking framework to ensure there is a significantly higher bar for less liquid shorts in the future.

Furthermore, we decided that any “gaps” in needed short exposure would more easily be filled immediately with index funds that could directly help offset some of the chunkier factor risks to our portfolio, namely European value stocks. We don’t intend to hold these index hedges forever, but believe it will help take pressure off of us to prematurely add new shorts to the portfolio. We have a lot of candidates in the backlog, but we are determined to ensure that we get the timing right as opposed to just the company thesis and factor exposure. At their core, our defensive moves should first do no harm. This analogy mirrors perhaps the most quoted Buffett lesson about rule number one, noted above.

In that vein, our current short portfolio is comprised of large, liquid index constituents with very low short interests, cheap borrows, and are largely well-loved. Similar to most of our short positions in the past, they also have mounting liabilities as decades of unconscious behaviors or corruption have eroded the core values of the businesses. We recently published our research on two newer positions on our investor-only research site. These shorts have multiple catalysts over the next few quarters, that we believe, will cause both a material impact to their financials while also possibly downgrading the market’s behavioral narrative.

More Conscious Than ESG

“Sustainability is built into our business model. If we are focused on the long term, there is no conflict between profitability and the interests of stakeholders. If you are focused on the short term, there is. It’s that simple!” Sir Martin Sorrell

Most importantly, these two businesses that we are short have some deeply unconscious features. While each case is different, this means that we’ve found evidence of corruption or deliberate sales of defective or toxic products for decades prior to being discontinued. All of these behaviors are only now catching up to these companies and present material downside risks to these businesses that have historically been run for short-term profit maximization as opposed to long-term value creation or innovation.

These are the kinds of companies that are causing the ESG movement to gain major traction around the world. But while we applaud action being taken on protecting the environment, the ESG movement is not solving the root of the problem. The movement is addressing the symptoms rather than the causes.

In a white paper that I can’t wait to publish, we’ll show evidence that the fundamental issue facing business today is one of unaccountable agents seeking immediate gratification. There’s a lack of ownership and accountability in a market that continues to outsource much of the “ratings” to agents. Large funds managed by agents with no skin in the game are relying on ratings agencies, also with no skin in the game, to dictate qualitative criteria that often don’t tie to value creation, but rather liability minimization. And that is important, but not sufficient on its own. It is defense without the offense. Or sometimes, it’s all marketing covering up flimsy foundations.

Owners or founders exhibit more long-term, conscious capitalist behavior. They generally don’t give quarterly profit guidance, and instead prefer to focus on their customer satisfaction and employee morale. They invest more in their own businesses rather than paying that capital out to shareholders or to acquisition targets. Great shareholder returns are the result of a highly conscious business model, not the goal in and of itself.

Exhibit 1: Builders Have Happier Customers & More Engaged Employees

Source: GreenWood Investors, OO = owner operators, DC = dual share class structures, S&P = S&P 1200 Global Index

But what does it mean actually to be conscious? That’s the subject that Anil Seth seeks to answer in his latest work, Being You. In seeking to demystify the mystery of consciousness, he discusses the most robust model that has been put forward for understanding and measuring how conscious an organism is. Integration information theory (IIT) postulates that consciousness is measured by the degree to which information is integrated into a system or action. Seth explains, “This underpins the main claim of the theory, which is that a system is conscious to the extent that its whole generates more information than its parts.”

This concept struck me, as it has many direct parallels to well-worn concepts in investing. Of course it makes sense that the more conscious an organization is, the better it is at integrating information into action. But what really struck me here is that using this IIT framework- an organization is only conscious if the whole is greater than the sum of its parts. To me this infers that if the parts of a business don’t come together to produce something more powerful or valuable than the sum of those individual units, segments or components, the business is not a conscious business.

Seth later explained how conscious perceptions are largely built from best guesses and confidence. A key insight of Bayesian inference is that perception is largely a function of updating beliefs about the world based on the precision and reliability of new information. Our minds seek to eliminate prediction errors everywhere and all the time, and we do so by converging our beliefs to the level of conviction we have in the information.

In this age of ubiquitous and free information, we differentiate ourselves by the level of conviction we have in the quality and reliability of the insights we have. Conviction is the key. And as Seth later demonstrated, such insights are virtually worthless if not paired with action. This echoes the sentiment that Warren Buffett expressed in talking about getting fat pitches in one’s career, and that one must “swing big,” as they don’t happen very often. This is indeed why we are “swinging big” with Coinvestment II, as this is one of the fattest pitches we’ve ever been thrown.

Moving From Defense to Offense

“High expectations are the key to everything.” -Sam Walton

As my mind was more occupied with offensive capital allocation strategies in the quarter, this pairing of action with insight particularly spoke to me, highly conscious offense playbook strategies are rare. Instead the norm is that most offensive actions are typically made from a defensive motive, and are not based on novel insights.

As I wrote in last year’s fourth quarter letter, we endeavor to only get involved in turnaround situations where we either have a board presence, or where a founder or owner operates the business. In our view, these managers have been more resilient in defending their businesses from adversity. Simply put, they cannot just give up and move on.

As Covid ripped through the world and economies, far too many managers decided to give up. In the depths of the Covid crisis, at the Presidential inauguration ceremony, National Youth Poet Laureate Amanda Gorman articulated rather eloquently that, “Your optimism will never be as powerful as it is in that exact moment when you want to give it up.” Founders are inherently optimistic, and they don’t give up.

In exploring the differences between defense and offense, I’ve come to realize that it is even more important to have an owner-oriented management culture when moving from defense to offense. Defense is inherently reactive, reacting to “known knowns” or “known unknowns.” Reactions are easier than proaction. Traditional boards are typically very good at liability minimization. But as important as liability reduction is, these actions do not create value.

New business and invention is inherently venturing into the unknown, seeing what others don’t, and pursuing the path untravelled. It comes naturally to a founder or owner, whose authorship imbues the business with the optimistic, entrepreneurial impulse that often started it in the first place. As my friend Bill Carey has articulated, most managers compensated via stock options act more like stock brokers as opposed to owners. Similar to brokers, their time horizons have shrunk considerably. They are simply rent-seeking for a short period of time. And as my friend Chris Mayer likes to say, “no one washes a rental.”

Our research on the differences in the behaviors of owner operators and these renters, shows these renters are not very good at offense strategies either. They are very good at competitive reactions, cost cutting and margin optimization. These are important, just as any defense strategy is, but they typically fail to create any lasting value. The value that is captured from these tools generally only lasts as long as the brief period in which the manager’s stock options vest. Given 70-90% of mergers and acquisitions fail, and stock repurchases have taken a notably pro-cyclical, buy-high, sell-low, history, these renters have a typically poor track record in value-creating initiatives and capital deployment.

This short-term rental behavior often results in mediocre outcomes. As the late great Sergio Marchionne regularly reminded, “mediocrity is not worth the trip.” Marchionne acted like an owner even before he was one. And he created so much value that his net worth neared $1 billion when he shuffled off this mortal coil. While much of that was indeed generated by options that he exercised, such options were struck at twice and three times the level at which he came in to rescue Fiat in 2004. His package inspired the design of CTT’s options package for top and first level managers.

Sergio was very good at seeing things others didn’t. He and his venerable team of managers, to whom he dedicated so much of his energy, were very good at transforming ignored products and assets into gold. Of particular note, Jeep grew from just over 2%of the market in the US to just under 6% when he passed- and it became a truly global brand. He invented Ferrari’s Icona series, which made the irregular limited edition profits part of the regular P&L of the brand without diluting the exclusivity of such models.

He and parent holding company Exor have continued to provide much of the inspiration behind our activities with both coinvestments. We endeavor to replicate their divide & conquer strategy, which allowed the Fiat Group to become stronger as stand-alone Fiat-Chrysler (now Stellantis), Ferrari, CNH, and soon to be Iveco Group. Just as Sergio advised the few believers throughout his career, investors will be “owning multiple pieces of paper” as the journey unfolds.

In hindsight, we can all agree on the value creation prowess of him and his team. But we easily forget that for most of his career, he was faced mostly by skeptics and doubters. He was not afraid to look dumb. In his own words, “A lot of what I do is challenge assumptions . . . which often looks like you are asking stupid questions.”

Being entrepreneurial, by definition, means taking the path untraveled, and heading into the unknown with daring boldness. Offense playbooks, by design, must take competition by surprise. Coming from a humble place with brands and companies that were ridiculed by competitors, when Sergio put medium-term plans out to the market, they were not timid. He would always aim higher than anyone, especially his competitors, believed he and his team could reach. And while not every target was always achieved, the formidable results speak for themselves.

This past earnings season, as Twitter was the only social media company to deliver on guidance while also confirming the quarter ahead to be at least as good, the stock sold off materially as its monetizable daily active user (MDAU) targets in the medium-term were called into question. While founder Jack Dorsey is clearly unafraid to look foolish to the public, or even in front of congress, he also manages multiple businesses at the same time. Competitors openly make fun of him. But his team is exceptionally loyal to him, and they have set out very ambitious targets for themselves over the next few years. The recent sell-off in Twitter shares was like deja vu all over again, as I reminisced about the Fiat capital markets day in 2014, fittingly on Twitter in this tweet thread.

With its product and revenue servers rebuilt, it can now innovate and launch new ad formats faster than ever before. We look forward to the Twitter team pressing its offense strategy as a major peer loses focus on its core business.

Into The Unknown

“Action is inseparable from perception. Perception and action are so tightly coupled that they determined and define each other. Every action alters perception by changing the incoming sensory data, and every perception is the way it is in order to help guide action. There is simply no point to perception in the absence of action.” Anil Seth, Being You

What does it mean to move into offense?

One thing very clear to us, is that it has to be a dynamic and reflexive approach. It cannot be built into a three or five year plan and remain fixed over that duration. As Anil Seth’s work on consciousness explains, a highly conscious being is constantly ingesting and integrating information, evolving actions based on reliability, precision and conviction.

As capital-markets focused investors, we believe one of the highest values we can provide to our companies is information that can be integrated into their offense and defense playbooks. Thanks to our collaborative approach, we get nearly daily recommendations and thoughts from our investors with new information, new case studies, and new suggestions on how to continue iterating.

One of the biggest differentiations between good and great investments, that is often overlooked, is the value added by good capital allocation- be it with a very well-done merger, opportunistic buyback or even more, venture-style investments that are almost in no one’s “model” or perception. Small acquisitions that bring new tools and managers can often upgrade the business model. As Clayton Christensen suggested in The Big Idea: The New M&A Playbook, these are often the most overlooked investments.

But during the quarter, when posed with the question of how to best allocate capital over the long term, I found myself tongue tied. For it’s a dynamic and reflexive question to ask. It’s easy to see what to do right now, and where to build in the next few years. But sound capital allocation is a function of the opportunities that present themselves. It is also about creating new possibilities, particular ones that competitors don’t see.

At CTT, with defensive, problem-solving actions becoming less of a focus, attention can now turn to offense. What that looks like in the near term, at least to me, should be continued progress and convergence on the strategy to become the Shopify of Iberia. With Portugal e-commerce order frequency at very small fractions of neighboring Spain, we believe it is CTT’s responsibility to make itself the most convenient and most cost effective way of conducting commerce. Through more parcel lockers, better digital tools, while maintaining or improving on best-in-class quality of service, we believe much of the responsibility to make online the most convenient commerce channel in Portugal will fall on CTT’s shoulders. Going further with online shop enabling, more cost effective payments tools, and an integrated fulfillment offer, that continues through to returns and customer service, it has every tool it needs to enable this digital transition. This convergence is happening at the same time EU recovery stimulus dollars will be directed towards digitalizing the economy.

Case studies like Kaspi, which started as a bank, evolved into a payments company, then launched an e-commerce marketplace and then further expanded into logistics, provide more inspiration than any company in the logistics industry. This reminds me of Google’s earliest days, when its managers encouraged their teams to ignore the traditional competitors and instead go where other competitors hadn’t dared to venture- into the unknown.

We believe CTT has greater competitive advantages than some “new economy” companies playing throughout the same e-commerce value chain, often trading at significantly higher valuation multiples. Whether we’re talking about fulfillment services, parcel lockers, or alternative purchase financing, it’s the customer relationship that differentiates and builds competitive advantages. That is why one of the first priorities of the new management was to improve customer satisfaction. And while some analysts that cover the company still use traditional methods to frame the opportunity, the shareholder base has largely transitioned away from income-oriented investors. More like-minded shareholders, aligned with management, can enable the team to build something truly great.

Building Great Companies

“The urgency of doing. Knowing is not enough; we must apply. Being willing is not enough; we must do.” DaVinci

What started for us as an approach to separate the bank from the industrial company, and achieve a sum of parts valuation, has been upgraded to that of building a great compound machine. As Exor articulated in 2019, its purpose to “build great companies,” is an aspirational philosophy for us. While we certainly aren’t doing the building here, perhaps through setting the right strategic priorities, incentives, and providing timely and right information, we can assist in the build underway.

Exor has provided an exemplary model of how to enable its teams to build greater value by dividing, conquering, and then often later combining with more synergistic peers. Just like Anil Seth described, the whole must be greater than the sum of the parts in a highly conscious organization. When a company’s sum of the parts is greater than the total, the organization is not conscious, and therefor not capable of adding material value.

Just as Exor has executed masterfully in its portfolio companies over the past decade, the path forward is one of both dividing and one of conquering. Extending the business and commerce services that CTT provides is a natural offense-oriented positioning that further reinforces the strength of the whole. But there are other parts of this organization that aren’t adding as much to the sum total- those can, and should be separated to pursue their own offense playbooks in a more focused and agile manner.

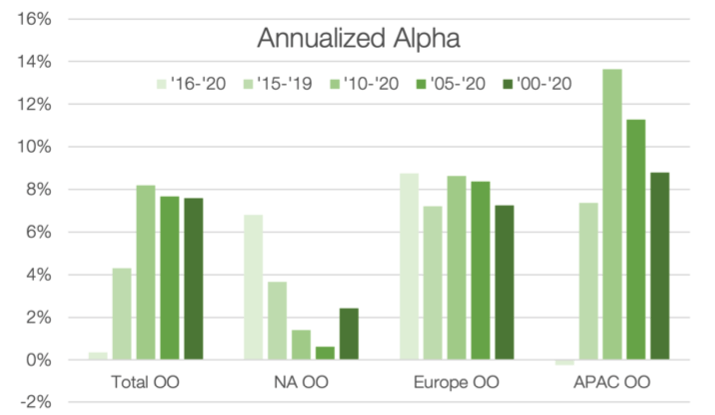

Such an approach goes well beyond ESG, and it goes well beyond most other broker-oriented management teams. It is a highly conscious capitalist approach, aligned with long term value creation and sustainability. And that process should result in considerable returns as an effect, not as a goal. As owner operators’ short, medium, and long term benchmark outperformance demonstrates, this strong alignment between management and ownership is a championship-winning combination.

Exhibit 2: Owner Operators’ Stock Index Outperformance

Source: GreenWood Investors

In the months ahead, we anticipate thoroughly engaging with the management and board of the target at the Builders Fund II. This company is mirroring CTT’s current posture, in that it is in the process of finishing nearly a decade of defense-oriented actions. After years of strategic actions focused on fixing problematic areas, contracts or business dynamics, most of these reactive or defensive actions are increasingly passing into the rearview mirror. It is entering a new phase of life in a position to also divide and conquer, and it has exceptional assets.

With both coinvestments representing a substantial portion of our net exposure, we move forward with conviction. While this quarter was a lesson that we, nor our companies, can lose sight of a strong defense strategy, we are increasingly looking forward to our portfolio pressing offense strategies moving forward.

Committed to deliver,

Steven Wood, CFA

GreenWood Investors

Updated on

Source valuewalk

{kind=link}

{kind=link}

{kind=link}