Published on January 28th, 2020 by Josh Arnold

Expeditors International of Washington Inc. (EXPD) may not be the best known stock to most investors given that it services a logistics and transportation niche in global commerce. However, the company has a terrific track record creating value for shareholders, both via appreciation in the share price, and by increasing its dividend payment.

In fact, 2019 marked the 25th consecutive year Expeditors increased its payout, making it a new member of the prestigious Dividend Aristocrats, a group of S&P 500 stocks with at least 25 consecutive years of dividend increases.

Including Expeditors, there are now 64 Dividend Aristocrats.

You can download an Excel spreadsheet of all 64, including important metrics such as P/E ratios, by clicking the link below:

Expeditors has proven over time to be a business with strong growth prospects, although that growth hasn’t been linear by any means. The cyclical nature of the shipping business creates inherent volatility, but over time, Expeditors has delivered growth.

Expeditors stock looks fairly valued today. The stock pays a low-single-digit dividend, and should produce mid-single-digit revenue growth annually for the foreseeable future. Overall, in light of the stock’s very long dividend increase history and steady growth, we see the stock as attractive for dividend growth investors.

Business Overview

Expeditors is a global logistics company that offers services including consolidation and forwarding of air and ocean freight, customs brokerage, vendor consolidation, cargo insurance, time-sensitive delivery options, order management, warehousing and distribution, and other customized logistics solutions. In short, Expeditors offers companies global commerce logistics solutions in all shapes and sizes.

Expeditors was founded in 1979 in Seattle and since that time, it has grown from a single office into more than 300 locations across six continents, spanning more than 100 countries and employing more than 17,000 people. Expeditors generates in excess of $8 billion of gross annual revenue, with air freight revenue being the largest single source. The company is fairly well diversified with its revenue streams, as we can see below:

Source: 2018 Annual Report, page 14

Expeditors has seen its shares move steadily higher in recent years and while the stock is somewhat off of its recent and all-time high, the company’s market capitalization is still near $13 billion.

Expeditors’ most recent earnings report was delivered in November of 2019 for the fiscal third quarter. The company reported some signs of weakness, including deviations from the trends of the first half of the year. Revenue was up just 1% during the quarter year-over-year as ocean volumes fell 2%, but airfreight volumes declined 9%. Volumes worsened in the latter half of the quarter as tariff and general global trade fears have caused some customers to pull back shipments.

Expenses rose about as quickly as revenue in Q3, so earnings-per-share came in flat year-over-year. Much stronger results in Q1 and Q2 have earnings-per-share up 6% through the first nine months, but it is obvious Expeditors is dealing with challenges that are outside of its control.

In a continuation of these trends, Expeditors issued updated Q4 guidance in the middle of January, that stated earnings would miss prior estimates due to continued unfavorable conditions in global shipping markets.

Growth Prospects

We see Expeditors producing annual earnings-per-share growth in the area of 4% to 6% thanks mostly to higher revenues. Top line growth has been far from linear in the past, but since 2010, has averaged about 4% per year.

Expeditors remains well-positioned to continue to see revenue growth over time through its diverse network of revenue streams, but note that recessions, global trade fears, and other exogenous shocks pose a risk to growth.

Source: 2018 Annual Report, page 30

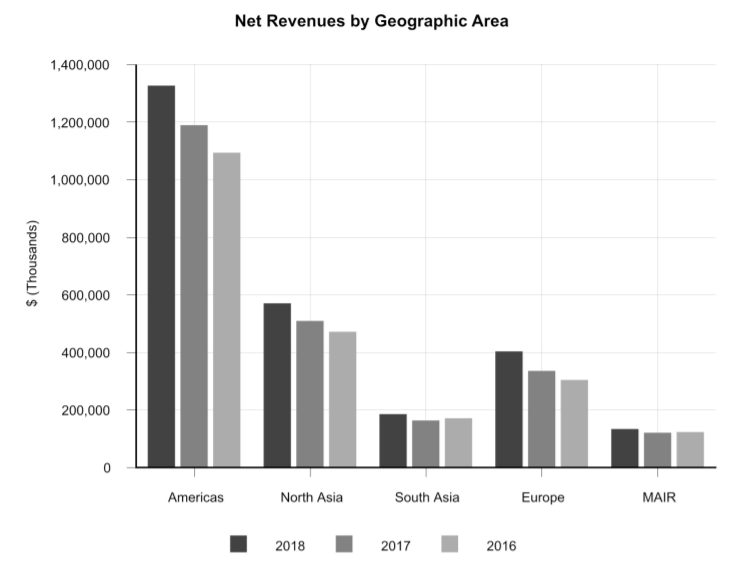

While Expeditors’ revenue base is well-diversified by service type, it is decidedly less so when it comes to geography. Expeditors still derives the vast majority of its revenue from the Americas, meaning it is particularly beholden to the ongoing trade war between China and the US. We think this headwind will pass at some point, but highlight that this geographical concentration may lead to volatility in revenue over time, as we’re seeing now.

From 2014-2018, the company grew airfreight tonnage, ocean containers, and gross revenue every year. Airfreight tonnage increased 3% in 2018. Tonnage is the preferred volume method Expeditors uses to assess performance, and while growth rates have been volatile, the general direction has been higher in recent years.

Were it not for the trade war, we believe Expeditors would be producing similar growth characteristics for the current fiscal year, and given this, we believe the long-term trend is higher for volumes. This will help drive revenues higher over time, as it has for many years.

Source: 2018 Annual Report, page 3

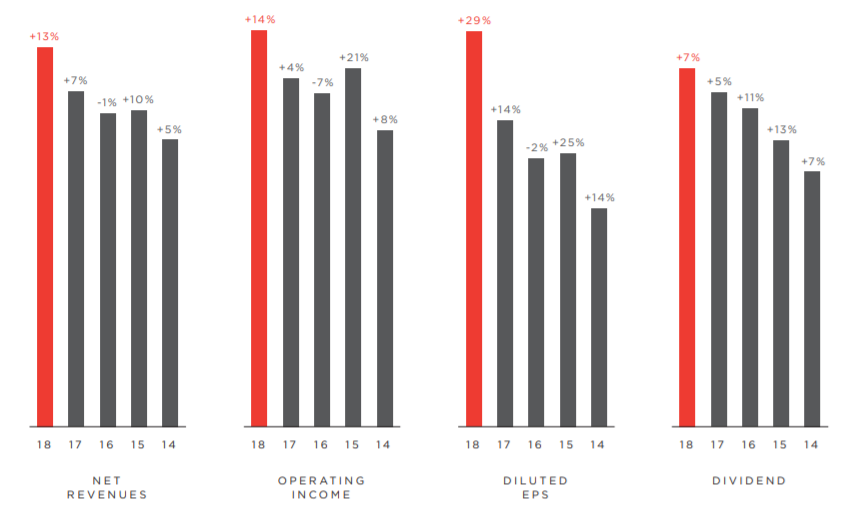

As we can see, revenue, operating income, and earnings-per-share have moved significantly higher over time, but there have been periods for all that showed negative year-over-year growth. Given the inherently volatile nature of the shipping business, we don’t see this as changing, but still expect to see mid-single-digit earnings-per-share growth annually over full economic cycles.

We think revenue will produce the bulk of these gains, while margins will remain generally flat, with a small tailwind from share repurchases. In total, we forecast 6% annual earnings-per-share growth annually.

Competitive Advantages & Recession Performance

Expeditors’ competitive advantage is its size and scale in a niche of global transportation of goods. Expeditors offers customers the scale of a global shipping company with a diverse network of ports and airports, but with the local and customized options of a smaller firm. This sets Expeditors apart from others in the logistics industry, but note that this is an industry where advantages are difficult to come by.

Expeditors’ earnings-per-share during the Great Recession are below:

- 2007 earnings-per-share: $1.21

- 2008 earnings-per-share: $1.37

- 2009 earnings-per-share: $1.12

- 2010 earnings-per-share: $1.59

Expeditors saw its earnings decline during the Great Recession, but only slightly. In fact, Expeditors held up much better than one would perhaps think given its leverage to the global economy. The next recession will likely crimp earnings growth temporarily, but will be far from disastrous for Expeditors given its strong track record during the Great Recession, one of the worst economic periods in recent history.

Valuation & Expected Returns

We see total returns in the high-single-digits for Expeditors over the next five years, driven mostly by earnings-per-share growth, but the dividend yield as well. We expect to see $3.40 in earnings-per-share for this fiscal year after Q4 guidance came in weaker than expected. With the share price at $74, Expeditors is trading for about 22 times earnings.

While that sounds a bit high, that is actually slightly lower than the stock’s ten-year average price-to-earnings ratio of 24. Expeditors has been valued highly by the market for a long time, and while we don’t think 24 times earnings is necessarily the right price, we see 22 times earnings as fairly valued.

We therefore see fair value for the stock at $75 or so – right where it trades as of this update – and forecast essentially no impact on total returns from the valuation.

Combining the forecast for 6% earnings-per-share growth, no impact from the valuation, and the current 1.4% dividend yield, we see total returns in the area of 7% to 8% over time.

We think Expeditors will also continue to grow its dividend at very strong rates over time, as it has boosted its payout by an average compound annual growth rate of 17% since 2003. That is a track record that is difficult to match for any company.

Although that level of growth is likely to fall short of its recent history, mid-single digit to high single-digit growth in the payout annually seems quite reasonable. Expeditors’ current yield is below the S&P 500 average and therefore is unattractive for income investors, but it remains a strong dividend growth stock.

Final Thoughts

Expeditors has been a strong player in the logistics industry for many years. The company has a diverse network of global ports and airports it services, as well as offering customized, valuable services to its global network of customers. Growth will likely continue to be volatile and vulnerable to interruptions, particularly during recessions, but we see Expeditors as attractive for the long-term.

The valuation today is fair, but not cheap, and the yield is quite low at just 1.4%. However, dividend growth should continue for many years to come given the payout ratio is around 30%, and upside to earnings should drive a higher share price over time.

Expeditors is appropriate for dividend growth investors, but not those seeking a high current yield, or earnings safety and consistency. Overall, the stock is somewhat attractive today given its valuation against historical norms, as well as earnings growth projections.

{kind=link}

{kind=link}

{kind=link}