Published on August 7th, 2022 by Nikolaos Sismanis

There is no exact definition for blue chip stocks. We define it as a stock with at least ten consecutive years of dividend increases. We believe an established track record of annual dividend increases going back at least a decade shows a company’s ability to generate steady growth and raise its dividend, even in a recession. As a result, we feel that blue chip stocks are among the safest dividend stocks investors can buy.

With all this in mind, we created a list of 350+ blue-chip stocks which you can download by clicking below:

In addition to the Excel spreadsheet above, we will individually review the top 50 blue chip stocks today as ranked using expected total returns from the Sure Analysis Research Database.

This installment of the 2022 Blue Chip Stocks In Focus series will analyze Hillenbrand, Inc. (HI).

Business Overview

Hillenbrand is an industrial conglomerate that operates through its three segments: Advanced Process Solutions, Molding Technology Solutions, and Batesville.

Advanced Process Solutions provides a variety of industrial solutions for companies’ manufacturing systems, Molding Technology Solutions is heavily involved in plastic processing and is exposed to the oil industry, and the legacy Batesville segment is a burial care business that provides burial caskets and services.

Hillenbrand has been diversifying away from its legacy Batesville segment (21.8% of 2021 sales) because even though burial care is an industry with high barriers to entry and good returns on capital for legacy businesses, the demand for caskets has been declining with the rise in popularity of lower cost cremation options.

The business has diversified into Advanced Process Solutions (43.5% of 2021 sales) and the Molding Technology Solutions segment (34.8% of sales), which was formed from the company’s acquisition of Milacron in 2019. Molding Technology Solutions is on track to achieve $75 million in cost synergies within 3 years of the acquisition. They have already recorded $58 million in cost synergies by the end of the fiscal year 2021.

Hillenbrand generates around $2.86 billion in annual revenues and is headquartered in Batesville, Indiana.

On August 3rd, 2022, Hillenbrand reported its fiscal Q3 results for the period ending June 30th, 2022. Revenues grew 3.7% year-over-year for the quarter to $720.6 million, driven by healthy industrial demand.

Adjusted earnings-per-share grew 8% year-over-year in the quarter to $0.92, and even though inflation and the impact of foreign currency exchange affected the business, favorable pricing, higher volume in the company’s industrial segments, and lower shares outstanding more than offset these headwinds.

Source: Investor Presentation

Management narrowed their guidance for fiscal 2022, now expecting adjusted earnings-per-share to land between $3.85 and $3.95.

Growth Prospects

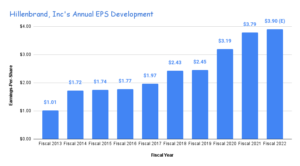

This business has seen steady growth in earnings-per-share, and we expect growth to continue. Over the past 9 years, Hillenbrand has seen earnings-per-share grow at an average annualized rate of 9.5%.

In 2022, we expect Hillenbrand to deliver $3.90 in earnings-per-share (the midpoint of management guidance), and we forecast that earnings-per-share will increase 4% annually over the intermediate term to reach our 2027 estimate of around $4.74 in earnings-per-share.

Source: SEC filings, Author

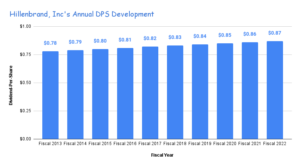

Over the past 9 years, the business has grown dividends per share at a rate of one cent per year. Following this trend, we expect that dividends per share will increase to $0.92 per share in 2027.

This increase of one cent per year works out to about 1% annual dividend growth, which is slow growth. Hillenbrand features a 14-year dividend growth streak, nonetheless.

Source: SEC filings, Author

Source: SEC filings, Author

The pace of divided increases is not particularly attractive, but we like Hillenbrand’s conservative approach. Combined with a resilient business model, we believe that Hillenbrand should continue to comfortably grow the dividend for many years to come.

Competitive Advantages & Recession Performance

Hillenbrand has averaged a payout ratio of 42% over the past 9 years and has averaged a 32% payout ratio over the past 5 years. The business has a low payout ratio, and we expect that dividends will continue to be safe over the intermediate term.

Additionally, we believe the business has a strong balance sheet after deleveraging from the 2019 Milacron acquisition. Further, much of Hillenbrand’s operating cash flows come from recession-proof businesses, such as the burial services segment.

We believe that the company will continue generating rather resilient results even during a recession. Hillenbrand’s ability to generate strong profits even during harsh economic environments was proven during the last prolonged recession.

You can see a rundown of Hillenbrand’s earnings-per-share from 2007 to 2011 below:

- 2007 earnings-per-share of $1.59

- 2008 earnings-per-share of $1.49

- 2009 earnings-per-share of $2.66

- 2010 earnings-per-share of $1.49

- 2011 earnings-per-share of $1.71

It’s also worth noting that Hillenbrand’s businesses feature robust pricing power characteristics, as proven in the company’s latest results. This is a great advantage in a highly inflationary environment like the current one.

Valuation & Expected Returns

Over the past 5 years, Hillenbrand has averaged a P/E ratio of 14.7, and over the past 9 years, the business has averaged a P/E ratio of 16.1. We estimate that a P/E ratio of 14 is about fair for the business under normal conditions, so this guided our 2027 P/E estimate.

Today, the stock offers a low 1.9% dividend yield, and the dividend is only expected to grow at ~1% annually over the intermediate term. Even though this business does have a stable history of dividend payments, the stock’s low yield may make it an unsuitable choice for investors that prioritize dividend income.

If the price-to-earnings multiple expands from 10.7 to 14, future returns would be boosted by 5.5% per year over the next five years. Combined with our EPS & DPS growth rates, as well as the current dividend yield, we project annualized returns could amount to 11.2% through 2027.

Accordingly, we rate Hillenbrand a buy.

Final Thoughts

Hillenbrand has proven itself to be a blue chip stock with a noteworthy track record of annual dividend increases. The company offers investors an opportunity to invest in an industrial conglomerate that is investing its legacy cash flows into growth industries to diversify the company.

We rate this stock a buy because we estimate that the stock offers total return prospects of 11.2% annually over the next five years. Investors might be interested in this stock because of the growth opportunities the business is pursuing and the favorable return prospects that the stock offers. Still, the pace of dividend growth is likely to remain at humble levels.

The Blue Chips list is not the only way to quickly screen for stocks that regularly pay rising dividends.

- The Dividend Aristocrats: S&P 500 stocks with 25+ years of consecutive dividend increases.

- The High Yield Dividend Aristocrats List is comprised of the Dividend Aristocrats with the highest current yields.

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 44 stocks with 50+ years of consecutive dividend increases.

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The 20 Highest Yielding Monthly Dividend Stocks: Monthly dividend stocks with the highest current yields.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Complete List of Russell 2000 Stocks: arguably the world’s best-known benchmark for small-cap U.S. stocks.

- The Best DRIP Stocks: The top 15 Dividend Aristocrats with no-fee dividend reinvestment plans.

- The 2022 High ROIC Stocks List: The top 10 stocks with high returns on invested capital.

- The 2022 High Beta Stocks List: The 100 stocks in the S&P 500 Index with the highest beta.

- The 2022 Low Beta Stocks List: The 100 stocks in the S&P 500 Index with the lowest beta.

{kind=link}

{kind=link}

{kind=link}